EXXITA BE CIRCULAR, S.A.: SaaS Transition Near Seville Facility as Normalized $228,908 Organic EBIT Loss Signals Structurally Unprofitable Core Operations

Date : 2026-07-15

Reading : 176

HDIN Market Intelligence Brief

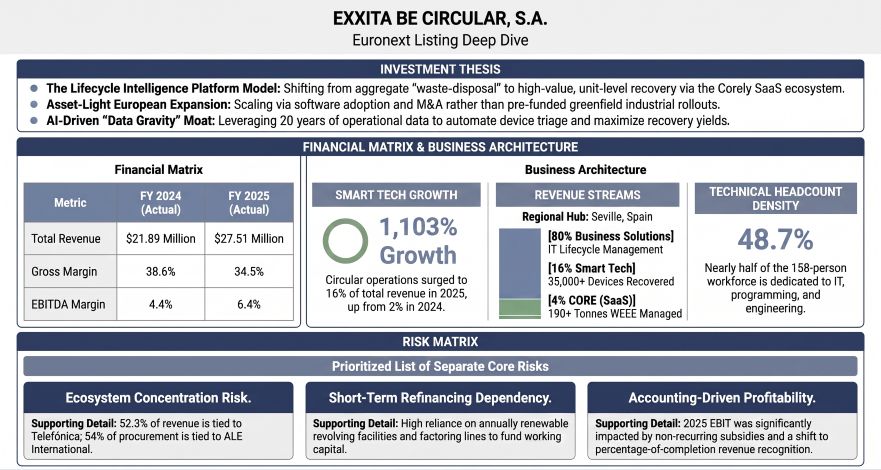

1. EXXITA BE CIRCULAR, S.A. [Euronext Access: EXXITA] reported FY2025 revenues of $27.51M (€24.33M), but generated a normalized organic EBIT loss of $228,908 (€202,466) after adjusting for non-recurring government subsidies and accounting shifts.

2. Physical processing remains highly centralized at a single 10,000 m² Seville hub, creating structural reverse-logistics friction and capital constraints for organic European footprint expansion.

3. Severe operational concentrations persist, with the Telefónica Group generating 52.3% of billing and ALE Internacional S.A.S. commanding 54% of procurement under non-guaranteed, order-by-order terms.

Figure EXXITA BE CIRCULAR: Euronext Listing Deep Dive

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

A granular audit of the FY2025 consolidated income statement for EXXITA BE CIRCULAR, S.A. reveals a structural shift toward digital and circular operations, accompanied by underlying gross margin pressures. The company achieved total revenues of $27,510,815 (€24,332,934) in FY2025, representing a 25.6% year-over-year expansion from the $21,894,624 (€19,365,491) reported in FY24.

However, the consolidated gross margin compressed by 410 basis points, declining from 38.6% in FY2024 to 34.5% in FY2025, highlighting elevated procurement costs and reliance on third-party service providers.

Operational leverage was partially sustained through disciplined fixed-cost absorption. Personnel expenses grew by 10.2%, lagging behind top-line growth and enabling EBITDA to expand by 81.7% to $1,750,000 (€1,550,000 approx.) in FY2025, up from $960,000 (€850,000 approx.) in FY24. This drove EBITDA margins from 4.4% to 6.4%. Reported net income reached $599,500 (€530,249) in FY2025, up from $54,300 (€48,028) in FY2024. Return on Invested Capital (ROIC) was estimated at 11.7% based on a Net Operating Profit After Tax (NOPAT) of ~$880,000 and average Invested Capital of ~$7.57M, outpacing the company's Weighted Average Cost of Capital (WACC) of 10.68%.

Operational throughput metrics for the 2024 cycle included:

* Device Recovery Volume: Exceeded 35,000 physical electronic devices.

* WEEE Managed: Handled over 190 tonnes of Waste Electrical and Electronic Equipment.

* Environmental Impact: Avoided approximately 58,000 kg of CO2 emissions.

* Workforce Integration: Trained over 1,360 individuals in digital/green skills; 753 individuals completed employment integration pathways.

The working capital cycle reflects a Cash Conversion Cycle (CCC) of 33 days, optimized through aggressive bank confirming and factoring lines to offset extended collections:

* Days Sales Outstanding (DSO): Averaged ~82 days. Trade receivables expanded by 15.0% to $6,580,000, with Telefónica Group representing ~60% of outstanding accounts, mitigated through non-recourse bank factoring.

* Days Inventory Outstanding (DIO): Optimized to ~70 days. Inventories decreased by 11.3% to $3,230,000, reflecting inventory impairment adjustments and faster throughput.

* Days Payable Outstanding (DPO): Extended to ~118 days. Accounts payable surged by 50.3% to $7,020,000, with ALE Internacional S.A.S. accounting for 63% of outstanding payables.

Infrastructure Layout and Regional Moats

EXXITA BE CIRCULAR, S.A. centralizes its physical infrastructure in Southern Europe. The primary operational asset is the "Circular Innovation Hub" in Bollullos de la Mitación, Seville, Spain, encompassing more than 10,000 square meters of technical, industrial, and logistical footprint.

The physical asset footprint includes:

* Polígono 6, Parcela 50, Nave B: An owned 2,768 m² warehouse, subject to a real encumbrance linked to a $276,884 (€244,900) incentive grant from the Andalusian Innovation and Development Agency.

* Parcela 73, Avenida de Umbrete: An owned 639.20 m² operational facility.

* Leased Industrial Facility: Expiring in May 2028.

The technical workforce comprises 158 employees, with 77 classified as technology/engineering staff (67 IT staff, 8 programmers, and 2 technical engineers), representing 48.7% of the total corporate headcount. This technical talent supports the "Tandem Algoritmo Verde" training initiative run via its 100%-owned Special Employment Centre subsidiary, Exxita Be Social, S.L.

This subsidiary operates under a formalized framework agreement dated February 3, 2025, featuring a 360-day payment window and a 6% transfer pricing mark-up.

The company possesses no registered patents. Its intellectual property moat is driven by its proprietary "Corely" software platform (comprising Corely Plant, Corely Retail Returns, and Corely Impact modules) and the "Aitana" AI-driven diagnostic engine, trained on data from over 20 years of operational interactions.

R&D capitalization on the balance sheet within Intangible Assets reached $534,153 (€472,451) in FY24 (2.44% of revenue) and $303,358 (€268,316) in FY25 (1.10% of revenue).

HDIN Institutional Verdict

An independent forensic normalization of EXXITA BE CIRCULAR, S.A.’s operating metrics challenges management's profitability narrative. After stripping out non-operating items, the core commercial business operated at a normalized organic EBIT loss of $228,908 (€-202,466) in FY2025.

Table Normalized Sustainable Operating Profit (EBIT) Bridge Analysis

The 2025 accounting policy shift to a percentage-of-completion basis accelerated $961,010 (€850,000) in revenues against $504,248 (€446,000) in costs, delivering a net pre-tax boost of $456,762 (€404,000). Furthermore, "Other operating income" of $980,175 (€866,951) consisted entirely of capitalized non-refundable government grants recognized in proportion to asset depreciation.

Excluding these adjustments, the core business remains unprofitable.

The company's balance sheet exposes public investors to significant operational counterparty concentrations:

[Total FY2025 Billings: $26.2M Verified Base]

│

├── Telefónica Group (52.3% of Billings / ~60.4% of Trade Receivables)

│ ├── Telefónica Soluciones, S.A.U.: $5.77M (€5.10M) [22.0% of billings / 24.8% of receivables]

│ ├── Telefónica de España, S.A.U.: $5.13M (€4.54M) [19.6% of billings / 28.9% of receivables]

│ └── Telefónica Cybersecurity & Cloud Tech, S.L.: $2.79M (€2.47M) [10.7% of billings / 5.6% of receivables]

│

└── Other Key Clients (47.7% of Billings)

└── DXC (ES Field Delivery), Siemens Financial, TCL Europe, Lenovo Spain

Purchasing is equally concentrated with ALE Internacional S.A.S. accounting for $11.52M (€10.19M), representing 54% of total supplier purchases and up to 63% of outstanding supplier liabilities by early 2026. The distributorship agreement lacks volume guarantees and contains change-of-control termination clauses.

The capital structure is highly dependent on short-term bank credit. Total financial debt stands at $3.22M (€2.85M) against equity of $7.47M (Debt-to-Equity: 0.43x). Short-term debt decreased by 30.4% to $2.55M, but the company remains dependent on factoring and confirming limits of $4.55M ($1.56M outstanding) that require annual renewal. Cash of $4.19M includes $2.71M in liquid investment funds.

The corporate governance structure lacks standard public market safeguards. There are zero independent board members across the 5 seats, split between the co-founders (Alejandro Costa, Jose Angel Costa, Ricardo Gonzalez) and private equity sponsor Global Social Impact Fund Spain (GSI), which owns 39.11% in Preferred Shares carrying liquidation preferences. Emprépolis, S.L. holds 60.89% (CEO Alejandro Costa holds 30.59% UBO via Puro Trece, S.L.U.). No Audit, Remuneration, or Nomination committees exist.

Related-party risk is highlighted by transactions with the CEO’s holding company Puro Trece, S.L.U., including a land lease of $11,032 (€9,758) in 2025 and a land purchase of $16,283 sqm in February 2026 for $223,859 (€198,000) cash. Aggregate related-party balances in FY25 include $1,851,199 (€1,637,360) in intercompany sales and current related-party assets of $686,327 (€607,047).

Liquidity is exposed to several contingent risks:

* Pending Litigation: Contentious-administrative proceedings against the Andalusian Agency for Innovation and Development (hearing June 24, 2026) regarding public subsidy clawbacks.

* Receivables Recovery: Ongoing litigation against RB Europa, S.L. to recover an impaired trade receivable of $61,052 (€54,000).

* Phantom Share Plan: 1,620 allocated phantom share units represent 2.32% of fully diluted capital, creating an off-balance-sheet cash liability triggered upon a change of control.

* Covenants: Change-of-control clauses in bank facilities and commercial contracts with Telefónica/ALE mandate minimum liability insurance policies between $2.26M and $5.65M.

With no contractually committed CapEx plans for physical expansion and 2026 cash flows projected to be negative due to working capital expansion, EXXITA’s proposed European expansion remains reliant on software licensing (Corely SaaS) rather than physical infrastructure deployment. The company's Enterprise Value of $28.19M (€24.9M) remains sensitive to execution risk under its 10.68% WACC assumption.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. EXXITA BE CIRCULAR, S.A. [Euronext Access: EXXITA] reported FY2025 revenues of $27.51M (€24.33M), but generated a normalized organic EBIT loss of $228,908 (€202,466) after adjusting for non-recurring government subsidies and accounting shifts.

2. Physical processing remains highly centralized at a single 10,000 m² Seville hub, creating structural reverse-logistics friction and capital constraints for organic European footprint expansion.

3. Severe operational concentrations persist, with the Telefónica Group generating 52.3% of billing and ALE Internacional S.A.S. commanding 54% of procurement under non-guaranteed, order-by-order terms.

Figure EXXITA BE CIRCULAR: Euronext Listing Deep Dive

Segmental Realities and Margin CompressionA granular audit of the FY2025 consolidated income statement for EXXITA BE CIRCULAR, S.A. reveals a structural shift toward digital and circular operations, accompanied by underlying gross margin pressures. The company achieved total revenues of $27,510,815 (€24,332,934) in FY2025, representing a 25.6% year-over-year expansion from the $21,894,624 (€19,365,491) reported in FY24.

However, the consolidated gross margin compressed by 410 basis points, declining from 38.6% in FY2024 to 34.5% in FY2025, highlighting elevated procurement costs and reliance on third-party service providers.

Table Segment Performance Metrics (FY2025)

| Segment Performance Metric | Business Solutions (Lifecycle Support) | Smart Tech (Refurbishment & Repair) | CORE (SaaS & AI Traceability) |

|---|---|---|---|

| FY2025 Revenue Share | ~80.0% | ~16.0% | ~4.0% |

| FY2025 Revenue (USD) | $21.94M | $4.40M | $1.10M |

| FY2025 Revenue (EUR) | €19.407M | €3.89M | €0.97M |

| YoY Revenue Growth | +5.0% | +1,103.0% | +116.0% |

| Primary Operational Focus | End-to-end ICT support, unified communications, outsourced IT services | Refurbishment, device reuse, reverse logistics, and repair services | "Corely" SaaS licensing, AI-assisted diagnostics, and ESG reporting solutions |

Operational leverage was partially sustained through disciplined fixed-cost absorption. Personnel expenses grew by 10.2%, lagging behind top-line growth and enabling EBITDA to expand by 81.7% to $1,750,000 (€1,550,000 approx.) in FY2025, up from $960,000 (€850,000 approx.) in FY24. This drove EBITDA margins from 4.4% to 6.4%. Reported net income reached $599,500 (€530,249) in FY2025, up from $54,300 (€48,028) in FY2024. Return on Invested Capital (ROIC) was estimated at 11.7% based on a Net Operating Profit After Tax (NOPAT) of ~$880,000 and average Invested Capital of ~$7.57M, outpacing the company's Weighted Average Cost of Capital (WACC) of 10.68%.

Operational throughput metrics for the 2024 cycle included:

* Device Recovery Volume: Exceeded 35,000 physical electronic devices.

* WEEE Managed: Handled over 190 tonnes of Waste Electrical and Electronic Equipment.

* Environmental Impact: Avoided approximately 58,000 kg of CO2 emissions.

* Workforce Integration: Trained over 1,360 individuals in digital/green skills; 753 individuals completed employment integration pathways.

The working capital cycle reflects a Cash Conversion Cycle (CCC) of 33 days, optimized through aggressive bank confirming and factoring lines to offset extended collections:

* Days Sales Outstanding (DSO): Averaged ~82 days. Trade receivables expanded by 15.0% to $6,580,000, with Telefónica Group representing ~60% of outstanding accounts, mitigated through non-recourse bank factoring.

* Days Inventory Outstanding (DIO): Optimized to ~70 days. Inventories decreased by 11.3% to $3,230,000, reflecting inventory impairment adjustments and faster throughput.

* Days Payable Outstanding (DPO): Extended to ~118 days. Accounts payable surged by 50.3% to $7,020,000, with ALE Internacional S.A.S. accounting for 63% of outstanding payables.

Infrastructure Layout and Regional Moats

EXXITA BE CIRCULAR, S.A. centralizes its physical infrastructure in Southern Europe. The primary operational asset is the "Circular Innovation Hub" in Bollullos de la Mitación, Seville, Spain, encompassing more than 10,000 square meters of technical, industrial, and logistical footprint.

The physical asset footprint includes:

* Polígono 6, Parcela 50, Nave B: An owned 2,768 m² warehouse, subject to a real encumbrance linked to a $276,884 (€244,900) incentive grant from the Andalusian Innovation and Development Agency.

* Parcela 73, Avenida de Umbrete: An owned 639.20 m² operational facility.

* Leased Industrial Facility: Expiring in May 2028.

The technical workforce comprises 158 employees, with 77 classified as technology/engineering staff (67 IT staff, 8 programmers, and 2 technical engineers), representing 48.7% of the total corporate headcount. This technical talent supports the "Tandem Algoritmo Verde" training initiative run via its 100%-owned Special Employment Centre subsidiary, Exxita Be Social, S.L.

This subsidiary operates under a formalized framework agreement dated February 3, 2025, featuring a 360-day payment window and a 6% transfer pricing mark-up.

The company possesses no registered patents. Its intellectual property moat is driven by its proprietary "Corely" software platform (comprising Corely Plant, Corely Retail Returns, and Corely Impact modules) and the "Aitana" AI-driven diagnostic engine, trained on data from over 20 years of operational interactions.

R&D capitalization on the balance sheet within Intangible Assets reached $534,153 (€472,451) in FY24 (2.44% of revenue) and $303,358 (€268,316) in FY25 (1.10% of revenue).

HDIN Institutional Verdict

An independent forensic normalization of EXXITA BE CIRCULAR, S.A.’s operating metrics challenges management's profitability narrative. After stripping out non-operating items, the core commercial business operated at a normalized organic EBIT loss of $228,908 (€-202,466) in FY2025.

Table Normalized Sustainable Operating Profit (EBIT) Bridge Analysis

| Operating Profit Adjustment Item | Amount (USD) | Amount (EUR) |

|---|---|---|

| Reported Operating Profit (EBIT) | $1.19M | €1.05M |

| (-) Non-Recurring Subsidies & Capital Grants | ($0.98M) | (€0.87M) |

| (-) Percentage-of-Completion Accounting Boost | ($0.46M) | (€0.40M) |

| (+) Exceptional One-Off Losses | $0.02M | €0.02M |

| Normalized Sustainable Operating Profit (EBIT) | ($0.23M) | (€0.20M) |

The 2025 accounting policy shift to a percentage-of-completion basis accelerated $961,010 (€850,000) in revenues against $504,248 (€446,000) in costs, delivering a net pre-tax boost of $456,762 (€404,000). Furthermore, "Other operating income" of $980,175 (€866,951) consisted entirely of capitalized non-refundable government grants recognized in proportion to asset depreciation.

Excluding these adjustments, the core business remains unprofitable.

The company's balance sheet exposes public investors to significant operational counterparty concentrations:

[Total FY2025 Billings: $26.2M Verified Base]

│

├── Telefónica Group (52.3% of Billings / ~60.4% of Trade Receivables)

│ ├── Telefónica Soluciones, S.A.U.: $5.77M (€5.10M) [22.0% of billings / 24.8% of receivables]

│ ├── Telefónica de España, S.A.U.: $5.13M (€4.54M) [19.6% of billings / 28.9% of receivables]

│ └── Telefónica Cybersecurity & Cloud Tech, S.L.: $2.79M (€2.47M) [10.7% of billings / 5.6% of receivables]

│

└── Other Key Clients (47.7% of Billings)

└── DXC (ES Field Delivery), Siemens Financial, TCL Europe, Lenovo Spain

Purchasing is equally concentrated with ALE Internacional S.A.S. accounting for $11.52M (€10.19M), representing 54% of total supplier purchases and up to 63% of outstanding supplier liabilities by early 2026. The distributorship agreement lacks volume guarantees and contains change-of-control termination clauses.

The capital structure is highly dependent on short-term bank credit. Total financial debt stands at $3.22M (€2.85M) against equity of $7.47M (Debt-to-Equity: 0.43x). Short-term debt decreased by 30.4% to $2.55M, but the company remains dependent on factoring and confirming limits of $4.55M ($1.56M outstanding) that require annual renewal. Cash of $4.19M includes $2.71M in liquid investment funds.

The corporate governance structure lacks standard public market safeguards. There are zero independent board members across the 5 seats, split between the co-founders (Alejandro Costa, Jose Angel Costa, Ricardo Gonzalez) and private equity sponsor Global Social Impact Fund Spain (GSI), which owns 39.11% in Preferred Shares carrying liquidation preferences. Emprépolis, S.L. holds 60.89% (CEO Alejandro Costa holds 30.59% UBO via Puro Trece, S.L.U.). No Audit, Remuneration, or Nomination committees exist.

Related-party risk is highlighted by transactions with the CEO’s holding company Puro Trece, S.L.U., including a land lease of $11,032 (€9,758) in 2025 and a land purchase of $16,283 sqm in February 2026 for $223,859 (€198,000) cash. Aggregate related-party balances in FY25 include $1,851,199 (€1,637,360) in intercompany sales and current related-party assets of $686,327 (€607,047).

Liquidity is exposed to several contingent risks:

* Pending Litigation: Contentious-administrative proceedings against the Andalusian Agency for Innovation and Development (hearing June 24, 2026) regarding public subsidy clawbacks.

* Receivables Recovery: Ongoing litigation against RB Europa, S.L. to recover an impaired trade receivable of $61,052 (€54,000).

* Phantom Share Plan: 1,620 allocated phantom share units represent 2.32% of fully diluted capital, creating an off-balance-sheet cash liability triggered upon a change of control.

* Covenants: Change-of-control clauses in bank facilities and commercial contracts with Telefónica/ALE mandate minimum liability insurance policies between $2.26M and $5.65M.

With no contractually committed CapEx plans for physical expansion and 2026 cash flows projected to be negative due to working capital expansion, EXXITA’s proposed European expansion remains reliant on software licensing (Corely SaaS) rather than physical infrastructure deployment. The company's Enterprise Value of $28.19M (€24.9M) remains sensitive to execution risk under its 10.68% WACC assumption.

Presentation Download & Video Access

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."