Global Civil Explosives & Ammonium Nitrate 2026 Outlook: Upstream Feedstock Decoupling Diverges from Downstream Blasting Consolidation as China's Zero-Personnel Mandates Trigger 53% Detonator Capacity Contraction

Date : 2026-07-15

Reading : 430

HDIN Executive Takeaways

1. Downstream civil explosives operators are shifting to integrated "drill-blast-dig-haul" contracts, with Chinese players driving domestic M&A to meet the MIIT's 2027 target of forming 3 to 5 mega-groups while export footprints expand into Belt and Road mining hubs.

2. Upstream giants are abandoning capital-inefficient green hydrogen, illustrated by CF Industries' $51.0 million write-down on its Donaldsonville electrolyzer, and redirecting capital to large-scale blue ammonia and carbon capture infrastructure.

3. Balance sheets face rising transitional friction, with Western multi-nationals holding extensive sub-surface remediation provisions like Orica's $119.7 million Botany project, while Chinese operators apply strict 0.00% terminal growth rates to domestic acquisition models.

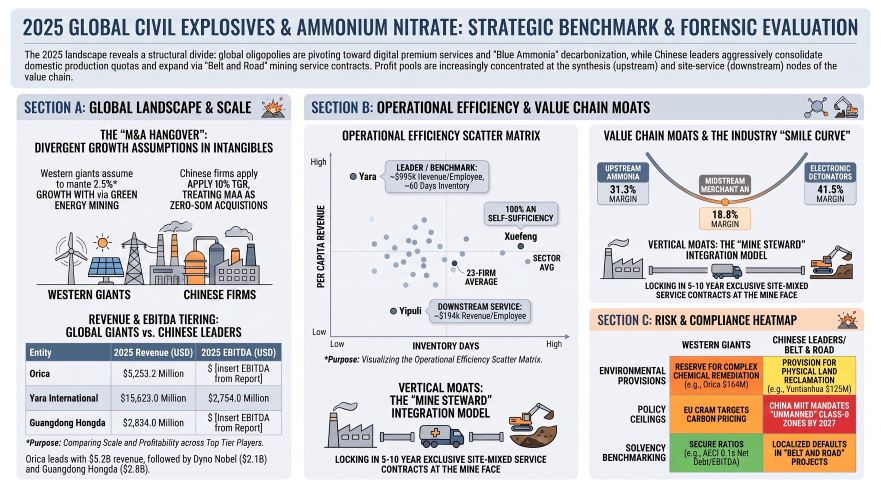

Figure 2025 GLOBAL CIVIL EXPLOSIVES & AMMONIUM NITRATE: STRATEGIC BENCHMARK & FORENSIC EVALUATION

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

A rigorous corporate finance and operational audit of the global civil explosives and upstream ammonium nitrate (AN) sectors in 2025 reveals a structural divergence. Upstream commodity suppliers are navigating a normalization phase as raw feedstock and product prices stabilize, while downstream explosives providers are aggressively pursuing margin capture through vertical integration, electronic initiation systems, and high-margin integrated "drill-blast-dig-haul" engineering contracts (the "Mine Steward" model).

The primary value-driver across this chain is governed by a distinct "Smile Curve." The highest gross margins are concentrated at the absolute extremes of the value chain: upstream ammonia synthesis (benefited by scale and regional natural gas price differentials) and downstream proprietary initiation systems/digital services (protected by technological and licensing barriers). Midstream merchant AN processing remains the most squeezed node.

The tables below synthesize the 2025 financial disclosures, asset capacities, and utilization rates across the 23 monitored corporations.

Table 1: Financial Performance and Labor Productivity

*Note: Currencies converted at 2025 average rates: 1 USD = 7.1875 CNY, 1 AUD = 0.645 USD, 1 ZAR = 0.056 USD, 1 EUR = 1.1306 USD.*

Table 2: Financial Performance and Capacity Profiles

Intra-Company Sourcing and Transfer Pricing Dynamics

To defend downstream margins from volatile raw material input costs, integrated corporations deploy divergent internal transfer pricing structures:

* Cost-Based Internal Transfers: CF Industries transfers synthetic ammonia and chemical intermediates downstream at manufacturing cost to upgrade into Granular Urea, UAN, and Ammonium Nitrate. This subsidizes upgraded product margins during feedstock surges. Similarly, Dyno Nobel secured a 25-year ammonia supply agreement with CF Industries for up to 200,000 short tons per annum, priced at estimated producer cost, insulating its North American explosives margin from Henry Hub volatility.

* Arm’s Length Market Pricing: Yara International operates its Global Production units as independent profit centers, selling intermediates to regional downstream entities (Europe, Americas, Africa & Asia) based strictly on the arm's length principle. Downstream regional divisions must justify their market positioning through "Premium generated" metrics, which reached $1.37 billion in 2025.

* Full Captive Closed-Loops: Xuefeng Technology operates a complete, circular local supply chain: "Natural Gas -> Synthetic Ammonia (400,000 tons capacity) -> Ammonium Nitrate (460,000 tons capacity) -> Civil Explosives -> Blasting Services." This closed-loop isolates the firm's cost structure from merchant AN price fluctuations, which fell to a 2025 average of ~2,200 RMB/ton (a year-over-year decrease of 7.7% to 10.0%).

* Pure Merchant Sourcing: EPC Groupe [ENXTPA: EXPL] operates without captive AN synthesis, sourcing requirements from the global merchant market. EPC manages price volatility via pluriannual contracts (3 to 7 years) that feature automatic monthly or quarterly price indexation alongside "unforeseeability clauses" (clauses d’imprévisibilités) to immediately pass through cost hikes to mining clients.

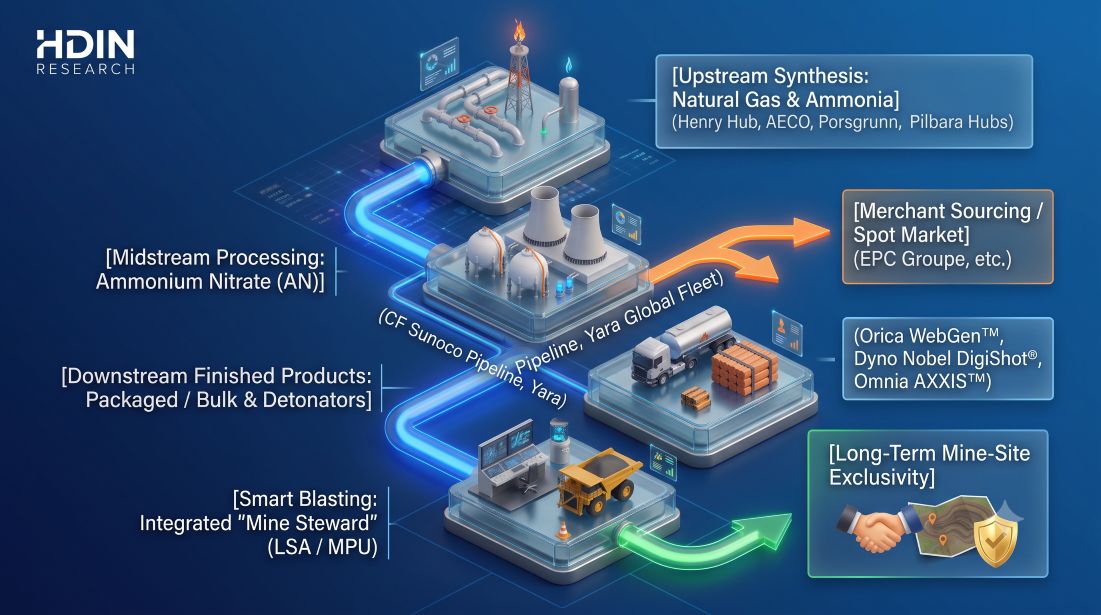

Infrastructure Layout and Regional Moats

Due to high transportation costs and strict security classifications governing Class 1 (explosives) and Class 5 (oxidizing agents/AN) materials, competitive moats are highly localized.

Figure Infrastructure Layout of Civil Explosives

Global Logistics Networks and Sourcing Hubs

* CF Industries: Operates 6 US production facilities (Donaldsonville, Port Neal, Yazoo City, Verdigris, Woodward, Waggaman) and 2 Canadian facilities. The Donaldsonville and Waggaman plants link directly to the 2,000-mile Sunoco ammonia pipeline, optimizing low-cost transport to the US Midwest. Sourcing is anchored to major trading hubs: Henry Hub (Louisiana), SONAT/TETCO ELA (Mississippi), ONEOK (Oklahoma), and AECO (Alberta). The firm permanently idled ammonia production at Billingham (UK), converting it into an import terminal sourcing lower-cost global ammonia.

* Yara International: Operates the world's largest ammonia trading network with 10,800+ transport units, 60+ ships, and 140+ terminal/warehouse locations. Export-oriented ammonia production is anchored in Porsgrunn (Norway), Sluiskil (Netherlands), and Pilbara (Australia).

* Orica Limited: Leverages geographical redundancy, maintaining a critical "supply switching" capability between its primary manufacturing hubs in Yarwun (Australia) and Alvin (USA) to service Latin American and North American clients during local shortages. Additional regional hubs include Kooragang Island (Australia) and specialized subsidiaries, including operations in Hong Kong, China.

* Dyno Nobel: Anchors its Asia-Pacific footprint in Moranbah (Bowen Basin) and Helidon, Australia. The firm sharpened its strategic focus by divesting its Australian fertilizer distribution division (Incitec Pivot Fertilisers) to Ridley Corporation to operate as a pure-play mining services provider.

Cross-Border "Belt and Road" Expansion and Regional Assets

Chinese domestic leaders, facing a saturated home market, are following Chinese mining state-owned enterprises (SOEs) overseas to capture high-margin blasting and engineering contracts:

* Jiangnan Chemical: Generated $179.9 million (12.96% of total revenue) from overseas markets, achieving 26.43% year-over-year growth. Its global logistics footprint spans Mongolia, Serbia, Namibia, the Democratic Republic of the Congo (DRC), and Liberia. In Namibia, operations are anchored by key account contracts with Swakop Uranium (Pty) Ltd ($71.39 million; 5.14% of revenue) and Rossing Uranium Limited ($46.82 million; 3.37% of revenue).

* Guangdong Hongda: Acquired a 51% controlling stake in a Peruvian explosives plant in January 2025 to establish a South American operating base. This complements its infrastructure nodes in Serbia, Pakistan, Laos, Guyana, Colombia, Guinea, the Republic of the Congo, the DRC, and Sierra Leone.

* Yipuli: Deploys site-mixed mobile processing units (MPUs) and ground stations across Namibia, Liberia, Pakistan, and Malaysia.

* Huhua: Exports initiating systems and civil explosives to over 30 countries, including Nepal, Myanmar, Australia, and Zimbabwe.

Capital Allocation for Decarbonization and Green Chemistry

* CF Industries: Abandoned its 20 MW alkaline water electrolyzer (green ammonia) project at Donaldsonville, taking a $51.0 million asset impairment charge due to unviable capital returns. Capital was reallocated to Carbon Capture and Storage (CCS) projects, including a $200.0 million CCS compression unit at Donaldsonville (capturing 2.0 million metric tons of CO2 annually) and a $100.0 million project at Yazoo City. CF directed $307.0 million of its $950.0 million total 2025 CapEx into the "Blue Point" joint venture (partnered with JERA and Mitsui), a $3.7 billion autothermal reforming (ATR) ammonia facility with integrated CCS designed to sequester 2.3 million metric tons of CO2 annually by 2029.

* Yara International: Operationalized its 24 MW renewable green hydrogen pilot at Herøya, Norway (producing 20,000 tonnes of green ammonia annually), but is focusing commercial-scale decarbonization on the Sluiskil CCS project (Netherlands), designed to capture and sequester 800,000 tonnes of CO2 annually via the Northern Lights offshore aquifer starting in 2026.

* Dyno Nobel: Invested $8.0 million to install tertiary N2O abatement at its Louisiana, Missouri (LOMO) nitric acid plant, lowering Scope 1 greenhouse gas emissions by 30% (550,000 tCO2e annually). An earlier $12.9 million ($20.0 million AUD) Moranbah abatement project continues to eliminate 200,000 tCO2e annually. The firm also commercialized the world's first fully electric MPU (eMPU) in Western Australia, powered by a 390-kWh lithium phosphate battery.

* Omnia (BME): Invested $2.97 million (53.0 million ZAR) to expand its Sasolburg solar facility to 10MW. In Canada, it partnered with Hypex Bio to build a hydrogen peroxide (nitrate-free) emulsion explosive plant scheduled for FY26 to eliminate nitrogen runoff.

* Product-Level Innovations: Orica commercialized its OPTEX® Low Carbon Emulsifiers, lowering carbon emissions by 70% to 85%. AECI validated its "PowerBoost" TNT/PETN-free booster technology, utilizing non-explosive raw materials that only sensitize when mixed on-site.

Chinese Regulatory and Consolidation Mandates (MIIT)

The Ministry of Industry and Information Technology (MIIT) is enforcing structural market changes:

* Enterprise Consolidation: Mandates a reduction in active civil explosives manufacturing enterprises from 76 to 50, with a policy goal of forging 3 to 5 internationally competitive mega-groups by 2027. In 2025, the top 10 groups commanded 63.26% of total industry output.

* Technology Phase-Out: Traditional packaged explosives capacity is strictly capped in favor of bulk site-mixed explosives (actual bulk output reached 36.4% to 44.74% in 2025, surpassing the >35% policy target). Peak industrial detonator capacity was cut by 53%, down from 3.6 billion units to ~1.7 billion units, via the mandatory substitution of traditional detonators with digital electronic detonators.

* Unmanned Safety Thresholds: Under MIIT's 2025 safety directives, all Class-0 dangerous equipment must be eliminated, and 1.1-level high-risk workshops must achieve zero fixed personnel by the end of 2027. This has driven high domestic R&D intensities (e.g., Shenzhen King's [SHE: 002917] at 6.22% and Yipuli at 5.17%) to commercialize JWL-ZW unmanned emulsion production lines operating under total human-machine isolation.

HDIN Institutional Verdict

An objective forensic audit of the 2025 reporting period reveals significant underlying balance sheet friction, M&A overvaluation risk, and structural anomalies that challenge management narratives.

M&A Overvaluation and Goodwill Impairment Risks

Aggressive corporate consolidation has bloated balance sheets with intangible goodwill. To justify these carrying values, Western and Chinese firms utilize vastly divergent testing parameters:

* The Chinese "Zero-Growth" Terminal Assumption: While Western giants apply inflation-linked terminal growth rates (Orica: 2.7%; Dyno Nobel: 2.5% CPI-linked) to justify their goodwill, Chinese consolidators (Guangdong Hongda, Jiangnan Chemical, Yahua Group) uniformly utilize a 0.00% Terminal Growth Rate (TGR) for their domestic impairment tests. This reflects a structural reality: domestic M&A is a zero-sum acquisition of state-allocated MIIT production quotas, with zero organic volume growth expected in a highly saturated, quota-capped domestic market.

* Realized Impairment Shocks: Orica executed a complete $87.2 million ($135.2 million AUD) goodwill write-off in its Latin America Blasting Solutions unit after forward cash flows failed to support carrying values. Dyno Nobel fully wrote down the carrying value of its Phosphate Hill manufacturing operations due to east coast Australian gas pricing risks. Yahua Group holds $114.7 million (824.5 million CNY) in original goodwill, but has been forced to record a massive $50.2 million (360.8 million CNY) impairment provision against acquired subsidiaries Keda and Jinheng, requiring highly elevated discount rates (14.27%) to reflect heightened risk premiums.

Financial Reporting Red Flags and Receivables Friction

* The Tongde Chemical Going Concern Crisis: Tongde Chemical [SHE: 002360] represents the most severe risk in the peer group. The company posted a net loss of -$152.1 million (-1.09 billion CNY) for 2025. Crucially, the company's audit report disclosed "uncertainty in the company's continuous operational capability" alongside a restatement of accounting errors spanning an entire decade (2015-2024). This is compounded by severe customer concentration, with the top 5 clients generating 69.62% of sales, and a single client representing 34.20% ($22.21 million).

* Capital Occupation and Related-Party Non-Trade Receivables: Several Chinese firms exhibit unusually high concentrations of non-trade "Other Receivables," signaling potential capital occupation by affiliates:

* Poly Union: Holds a staggering $346.6 million (2.49 billion CNY) in "Other Receivables" owed entirely by its affiliated entity, Poly Xinlian Blasting Engineering Group.

* Yahua Group: Disclosed an exceptionally high Other Receivables balance of $199.3 million (1.43 billion CNY).

* Xuefeng Technology: 88.84% of its Other Receivables ($20.9 million / 150.5 million CNY) is concentrated in transactions with its internal related-party, Xinjiang Xuefeng Blasting Engineering Co.

* Off-Balance Sheet Risks: Kailong Chemical carries significant contingent risk via corporate guarantees provided to subsidiaries, with approved guarantee quotas reaching $161.0 million (1.157 billion CNY).

* "Belt and Road" Write-Offs & Bad Debts: Global expansion into frontier markets is yielding credit defaults. Yipuli recorded 100% impairment provisions on receivables from Hunan Zhong'an Resource ($3.07 million / 22.1 million CNY) and China Union Investment (Liberia) Bong Mining ($2.35 million / 16.9 million CNY). Huhua wrote off 100% of receivables from foreign entities PERSIMMON LLC ($1.5 million / 10.8 million CNY) and Myanmar Welfare Mining ($295,000 / 2.1 million CNY).

Litigations and Environmental Clean-Up Liabilities

* Orica vs. CF Industries (The Trans-Pacific Dispute): Orica and its US joint venture (Nelson Brothers) are locked in litigation in Illinois court against CF Industries regarding a long-term (expiring 2031) AN Purchase Agreement. Orica has alleged breach of contract, anti-trust violations, and fraud, projecting legal costs of $32.2 million to $38.7 million ($50.0 million to $60.0 million AUD) for 2026 alone. Escalating this friction, CF Industries issued a Force Majeure notice to Orica in November 2025, declaring an inability to supply industrial AN following a major incident at its Yazoo City plant (which also resulted in a $25.0 million physical asset write-down for CF).

* Under-Provisioned Environmental Liabilities: The balance sheets of Western giants are heavily burdened by multi-decade, sub-surface chemical liabilities:

* Orica: Carries total environmental and decommissioning provisions of $164.7 million ($255.4 million AUD). This is heavily dominated by the Botany groundwater remediation project ($119.7 million / $185.6 million AUD), which requires continuous groundwater extraction and remediation of Dense Non-Aqueous Phase Liquid (DNAPL) contamination until at least 2036.

* Dyno Nobel: Booked $114.2 million ($177.0 million AUD) in environmental liabilities, including a $71.7 million ($111.2 million AUD) remediation provision for the Gibson Island land sale, and $42.2 million ($65.5 million AUD) for the closure of its Geelong facility.

* CF Industries: Identified as a Potentially Responsible Party (PRP) under CERCLA (Superfund) for a former phosphate mine in Georgetown Canyon, Idaho, exposing the firm to indefinite natural resource damage claims.

* Yara International: Carries environmental provisions of $122.0 million (covering industrial site restoration, including the Siilinjärvi apatite mine in Finland) and a further $111.0 million for asset decommissioning.

* Yuntianhua: Disclosed a massive environmental recovery provision of $125.07 million (898.9 million CNY). Unlike the chemical groundwater liabilities of the West, this is geared toward volume-based, visible physical land reclamation, mine geological restoration, and phosphogypsum solid waste treatment to comply with China's "Green Mine" certifications.

In conclusion, while upstream nitrogen manufacturers have extracted robust profitability due to low North American natural gas costs ($3.31/MMBtu realized by CF Industries), their capital-intensive decarbonization pathways are shifting toward blue carbon capture. Downstream, the civil explosives sector's transition to the integrated "Mine Steward" model has successfully driven volume pull-through, but has simultaneously bloated balance sheets with non-trade receivables, unamortized goodwill, and regional credit exposure across developing markets.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. Downstream civil explosives operators are shifting to integrated "drill-blast-dig-haul" contracts, with Chinese players driving domestic M&A to meet the MIIT's 2027 target of forming 3 to 5 mega-groups while export footprints expand into Belt and Road mining hubs.

2. Upstream giants are abandoning capital-inefficient green hydrogen, illustrated by CF Industries' $51.0 million write-down on its Donaldsonville electrolyzer, and redirecting capital to large-scale blue ammonia and carbon capture infrastructure.

3. Balance sheets face rising transitional friction, with Western multi-nationals holding extensive sub-surface remediation provisions like Orica's $119.7 million Botany project, while Chinese operators apply strict 0.00% terminal growth rates to domestic acquisition models.

Figure 2025 GLOBAL CIVIL EXPLOSIVES & AMMONIUM NITRATE: STRATEGIC BENCHMARK & FORENSIC EVALUATION

Segmental Realities and Margin CompressionA rigorous corporate finance and operational audit of the global civil explosives and upstream ammonium nitrate (AN) sectors in 2025 reveals a structural divergence. Upstream commodity suppliers are navigating a normalization phase as raw feedstock and product prices stabilize, while downstream explosives providers are aggressively pursuing margin capture through vertical integration, electronic initiation systems, and high-margin integrated "drill-blast-dig-haul" engineering contracts (the "Mine Steward" model).

The primary value-driver across this chain is governed by a distinct "Smile Curve." The highest gross margins are concentrated at the absolute extremes of the value chain: upstream ammonia synthesis (benefited by scale and regional natural gas price differentials) and downstream proprietary initiation systems/digital services (protected by technological and licensing barriers). Midstream merchant AN processing remains the most squeezed node.

The tables below synthesize the 2025 financial disclosures, asset capacities, and utilization rates across the 23 monitored corporations.

Table 1: Financial Performance and Labor Productivity

*Note: Currencies converted at 2025 average rates: 1 USD = 7.1875 CNY, 1 AUD = 0.645 USD, 1 ZAR = 0.056 USD, 1 EUR = 1.1306 USD.*

| Company [Ticker] | Revenue (USD M) | Operating Income / EBITDA (USD M) | Net Profit / NPAT (USD M) | Margin / Working Capital Metrics | Workforce / Employee Count | Revenue per Employee (USD) |

|---|---|---|---|---|---|---|

| Yara International [OL: YAR] | $15,623.0 | EBITDA: $2,754.0Operating Income: $1,571.0 | Net Income: $1,372.0 | Net Operating Capital Cycle: 58 daysCredit Days: 39Inventory Days: 60Payable Days: 41 | 15,702 | ~$995,000 |

| CF Industries [NYSE: CF] | $7,084.0 | Gross Profit: $2,724.0 | Net Profit: $1,798.0 | Consolidated Gross Margin: 38.5%Granular Urea: 47.0%UAN: 42.6%Ammonia: 31.3%AN: 18.8% | N/A | N/A |

| Orica Limited [ASX: ORI] | $5,253.2(AUD 8,144.5M) | EBIT: $639.8 | NPAT: $348.9 | N/A | N/A | N/A |

| Dyno Nobel [ASX: IPL] | $2,071.9(AUD 3,212.3M) | EBITDA: $440.1 | NPAT: $104.7(AUD 162.3M) | Trade Working Capital: 20.4% of sales | ~5,500 | ~$376,700 |

| Omnia Holdings [JSE: OMN] | $1,278.3(ZAR 22,818M) | N/A | Net Profit: $64.0 | Mining Segment Working Capital: 17.8% | Mining Segment: 1,803 | ~$283,400(Mining Revenue: $511.0M) |

| AECI Ltd [JSE: AFE] | $987.2(ZAR 17,622M) | Mining EBITDA: $152.5 | N/A | Mining EBITDA Margin: 15.0% | Mining Segment: 5,459 | ~$180,800 |

| Ancora Indonesia Resources [IDX: OKAS] | $161.64 | Gross Profit: $47.5 | N/A | Gross Margin: 29.4% | N/A | N/A |

Table 2: Financial Performance and Capacity Profiles

| Company [Ticker] | Revenue (USD M) | Net Profit / Total Profit (USD M) | Segment Structure & Margin Profile | Industrial Explosives Capacity & Utilization | Electronic Detonator Capacity & Utilization |

|---|---|---|---|---|---|

| Guangdong Hongda [SHE: 002683] | $2,834.0(CNY 20.37B) | Net Profit: $133.1 | R&D Intensity: 3.42%($96.8M / CNY 695.9M) | Utilization: 84.27%Capacity: 701,500 tons | Utilization: 47.84%Capacity: 52.24M units |

| Jiangnan Chemical [SHE: 002226] | $1,388.7(CNY 9.98B) | N/A | Blasting Services: 53.33% ($740.6M)Product Sales: 30.88% ($428.8M)R&D Intensity: 3.16% | Utilization: 77.81%Capacity: 892,000 tons | Utilization: 64.14%Capacity: 150.65M units |

| Yipuli [SHE: 002096] | $1,367.9(CNY 9.83B) | Total Profit: $144.9 | R&D Intensity: 5.17%($70.7M / CNY 508.1M) | Utilization: 90.04%Capacity: 581,500 tons | Utilization: 57.16%Capacity: 64.5M units |

| Poly Union [SHE: 002037] | $930.9(CNY 6.69B) | N/A | Blasting & Engineering: 65.72% ($611.8M)Product Sales: 30.93% ($287.9M)Product Gross Margin: 31.75% | Utilization: 69.97%Capacity: 484,500 tons | N/A |

| Xuefeng Technology [SHA: 603727] | $774.1(CNY 5.56B) | Net Profit: $70.1 | AN Upstream Capacity: 460,000 tonsAN Design Capacity: 660,000 tonsAN Utilization: 65.86% | Utilization: 95.25%Capacity: 151,500 tons | Utilization: 37.19%Capacity: 18.9M units |

| Kailong Chemical [SHE: 002783] | $493.1(CNY 3.54B) | N/A | AN & Fertilizer Segment: $128.3M (26.03%)Explosives Gross Margin: 38.68%Blasting Gross Margin: 38.40% | Utilization: 84.26%Capacity: 259,700 tons | Utilization: 85.98%Capacity: 50.0M units |

| Tibet Gaozheng [SHE: 002827] | $254.3(CNY 1.83B) | N/A | Blasting Services: 50.89% ($129.4M)Product Sales: 38.74% | N/A | N/A |

| Huhua [SHE: 003022] | $182.6(CNY 1.31B) | Net Profit: $23.9 | Industrial Detonators GM: 41.49%Industrial Explosives GM: 38.31%Blasting Services GM: 33.76% | Utilization: 71.51%Capacity: 114,000 tons | Utilization: 79.42%Capacity: 58.8M units |

| Tongde Chemical [SHE: 002360] | $65.7(CNY 472.4M) | Net Loss: -$152.1M(CNY -1.09B) | N/A | Utilization: 43.79%Capacity: 68,000 tons | N/A |

| Guotai Group [SHA: 603977] | N/A | N/A | N/A | Utilization: 87.62%Capacity: 188,000 tons | Utilization: 99.95%Capacity: 30.27M units |

| Hualu-Hengsheng [SHA: 600426] | $3,980.5(CNY 28.61B) | N/A | Fertilizer Segment Revenue: $1,016.4MFertilizer Gross Margin: 32.30% | N/A | N/A |

Intra-Company Sourcing and Transfer Pricing Dynamics

To defend downstream margins from volatile raw material input costs, integrated corporations deploy divergent internal transfer pricing structures:

* Cost-Based Internal Transfers: CF Industries transfers synthetic ammonia and chemical intermediates downstream at manufacturing cost to upgrade into Granular Urea, UAN, and Ammonium Nitrate. This subsidizes upgraded product margins during feedstock surges. Similarly, Dyno Nobel secured a 25-year ammonia supply agreement with CF Industries for up to 200,000 short tons per annum, priced at estimated producer cost, insulating its North American explosives margin from Henry Hub volatility.

* Arm’s Length Market Pricing: Yara International operates its Global Production units as independent profit centers, selling intermediates to regional downstream entities (Europe, Americas, Africa & Asia) based strictly on the arm's length principle. Downstream regional divisions must justify their market positioning through "Premium generated" metrics, which reached $1.37 billion in 2025.

* Full Captive Closed-Loops: Xuefeng Technology operates a complete, circular local supply chain: "Natural Gas -> Synthetic Ammonia (400,000 tons capacity) -> Ammonium Nitrate (460,000 tons capacity) -> Civil Explosives -> Blasting Services." This closed-loop isolates the firm's cost structure from merchant AN price fluctuations, which fell to a 2025 average of ~2,200 RMB/ton (a year-over-year decrease of 7.7% to 10.0%).

* Pure Merchant Sourcing: EPC Groupe [ENXTPA: EXPL] operates without captive AN synthesis, sourcing requirements from the global merchant market. EPC manages price volatility via pluriannual contracts (3 to 7 years) that feature automatic monthly or quarterly price indexation alongside "unforeseeability clauses" (clauses d’imprévisibilités) to immediately pass through cost hikes to mining clients.

Infrastructure Layout and Regional Moats

Due to high transportation costs and strict security classifications governing Class 1 (explosives) and Class 5 (oxidizing agents/AN) materials, competitive moats are highly localized.

Figure Infrastructure Layout of Civil Explosives

Global Logistics Networks and Sourcing Hubs

* CF Industries: Operates 6 US production facilities (Donaldsonville, Port Neal, Yazoo City, Verdigris, Woodward, Waggaman) and 2 Canadian facilities. The Donaldsonville and Waggaman plants link directly to the 2,000-mile Sunoco ammonia pipeline, optimizing low-cost transport to the US Midwest. Sourcing is anchored to major trading hubs: Henry Hub (Louisiana), SONAT/TETCO ELA (Mississippi), ONEOK (Oklahoma), and AECO (Alberta). The firm permanently idled ammonia production at Billingham (UK), converting it into an import terminal sourcing lower-cost global ammonia.

* Yara International: Operates the world's largest ammonia trading network with 10,800+ transport units, 60+ ships, and 140+ terminal/warehouse locations. Export-oriented ammonia production is anchored in Porsgrunn (Norway), Sluiskil (Netherlands), and Pilbara (Australia).

* Orica Limited: Leverages geographical redundancy, maintaining a critical "supply switching" capability between its primary manufacturing hubs in Yarwun (Australia) and Alvin (USA) to service Latin American and North American clients during local shortages. Additional regional hubs include Kooragang Island (Australia) and specialized subsidiaries, including operations in Hong Kong, China.

* Dyno Nobel: Anchors its Asia-Pacific footprint in Moranbah (Bowen Basin) and Helidon, Australia. The firm sharpened its strategic focus by divesting its Australian fertilizer distribution division (Incitec Pivot Fertilisers) to Ridley Corporation to operate as a pure-play mining services provider.

Cross-Border "Belt and Road" Expansion and Regional Assets

Chinese domestic leaders, facing a saturated home market, are following Chinese mining state-owned enterprises (SOEs) overseas to capture high-margin blasting and engineering contracts:

* Jiangnan Chemical: Generated $179.9 million (12.96% of total revenue) from overseas markets, achieving 26.43% year-over-year growth. Its global logistics footprint spans Mongolia, Serbia, Namibia, the Democratic Republic of the Congo (DRC), and Liberia. In Namibia, operations are anchored by key account contracts with Swakop Uranium (Pty) Ltd ($71.39 million; 5.14% of revenue) and Rossing Uranium Limited ($46.82 million; 3.37% of revenue).

* Guangdong Hongda: Acquired a 51% controlling stake in a Peruvian explosives plant in January 2025 to establish a South American operating base. This complements its infrastructure nodes in Serbia, Pakistan, Laos, Guyana, Colombia, Guinea, the Republic of the Congo, the DRC, and Sierra Leone.

* Yipuli: Deploys site-mixed mobile processing units (MPUs) and ground stations across Namibia, Liberia, Pakistan, and Malaysia.

* Huhua: Exports initiating systems and civil explosives to over 30 countries, including Nepal, Myanmar, Australia, and Zimbabwe.

Capital Allocation for Decarbonization and Green Chemistry

* CF Industries: Abandoned its 20 MW alkaline water electrolyzer (green ammonia) project at Donaldsonville, taking a $51.0 million asset impairment charge due to unviable capital returns. Capital was reallocated to Carbon Capture and Storage (CCS) projects, including a $200.0 million CCS compression unit at Donaldsonville (capturing 2.0 million metric tons of CO2 annually) and a $100.0 million project at Yazoo City. CF directed $307.0 million of its $950.0 million total 2025 CapEx into the "Blue Point" joint venture (partnered with JERA and Mitsui), a $3.7 billion autothermal reforming (ATR) ammonia facility with integrated CCS designed to sequester 2.3 million metric tons of CO2 annually by 2029.

* Yara International: Operationalized its 24 MW renewable green hydrogen pilot at Herøya, Norway (producing 20,000 tonnes of green ammonia annually), but is focusing commercial-scale decarbonization on the Sluiskil CCS project (Netherlands), designed to capture and sequester 800,000 tonnes of CO2 annually via the Northern Lights offshore aquifer starting in 2026.

* Dyno Nobel: Invested $8.0 million to install tertiary N2O abatement at its Louisiana, Missouri (LOMO) nitric acid plant, lowering Scope 1 greenhouse gas emissions by 30% (550,000 tCO2e annually). An earlier $12.9 million ($20.0 million AUD) Moranbah abatement project continues to eliminate 200,000 tCO2e annually. The firm also commercialized the world's first fully electric MPU (eMPU) in Western Australia, powered by a 390-kWh lithium phosphate battery.

* Omnia (BME): Invested $2.97 million (53.0 million ZAR) to expand its Sasolburg solar facility to 10MW. In Canada, it partnered with Hypex Bio to build a hydrogen peroxide (nitrate-free) emulsion explosive plant scheduled for FY26 to eliminate nitrogen runoff.

* Product-Level Innovations: Orica commercialized its OPTEX® Low Carbon Emulsifiers, lowering carbon emissions by 70% to 85%. AECI validated its "PowerBoost" TNT/PETN-free booster technology, utilizing non-explosive raw materials that only sensitize when mixed on-site.

Chinese Regulatory and Consolidation Mandates (MIIT)

The Ministry of Industry and Information Technology (MIIT) is enforcing structural market changes:

* Enterprise Consolidation: Mandates a reduction in active civil explosives manufacturing enterprises from 76 to 50, with a policy goal of forging 3 to 5 internationally competitive mega-groups by 2027. In 2025, the top 10 groups commanded 63.26% of total industry output.

* Technology Phase-Out: Traditional packaged explosives capacity is strictly capped in favor of bulk site-mixed explosives (actual bulk output reached 36.4% to 44.74% in 2025, surpassing the >35% policy target). Peak industrial detonator capacity was cut by 53%, down from 3.6 billion units to ~1.7 billion units, via the mandatory substitution of traditional detonators with digital electronic detonators.

* Unmanned Safety Thresholds: Under MIIT's 2025 safety directives, all Class-0 dangerous equipment must be eliminated, and 1.1-level high-risk workshops must achieve zero fixed personnel by the end of 2027. This has driven high domestic R&D intensities (e.g., Shenzhen King's [SHE: 002917] at 6.22% and Yipuli at 5.17%) to commercialize JWL-ZW unmanned emulsion production lines operating under total human-machine isolation.

HDIN Institutional Verdict

An objective forensic audit of the 2025 reporting period reveals significant underlying balance sheet friction, M&A overvaluation risk, and structural anomalies that challenge management narratives.

M&A Overvaluation and Goodwill Impairment Risks

Aggressive corporate consolidation has bloated balance sheets with intangible goodwill. To justify these carrying values, Western and Chinese firms utilize vastly divergent testing parameters:

* The Chinese "Zero-Growth" Terminal Assumption: While Western giants apply inflation-linked terminal growth rates (Orica: 2.7%; Dyno Nobel: 2.5% CPI-linked) to justify their goodwill, Chinese consolidators (Guangdong Hongda, Jiangnan Chemical, Yahua Group) uniformly utilize a 0.00% Terminal Growth Rate (TGR) for their domestic impairment tests. This reflects a structural reality: domestic M&A is a zero-sum acquisition of state-allocated MIIT production quotas, with zero organic volume growth expected in a highly saturated, quota-capped domestic market.

* Realized Impairment Shocks: Orica executed a complete $87.2 million ($135.2 million AUD) goodwill write-off in its Latin America Blasting Solutions unit after forward cash flows failed to support carrying values. Dyno Nobel fully wrote down the carrying value of its Phosphate Hill manufacturing operations due to east coast Australian gas pricing risks. Yahua Group holds $114.7 million (824.5 million CNY) in original goodwill, but has been forced to record a massive $50.2 million (360.8 million CNY) impairment provision against acquired subsidiaries Keda and Jinheng, requiring highly elevated discount rates (14.27%) to reflect heightened risk premiums.

Financial Reporting Red Flags and Receivables Friction

* The Tongde Chemical Going Concern Crisis: Tongde Chemical [SHE: 002360] represents the most severe risk in the peer group. The company posted a net loss of -$152.1 million (-1.09 billion CNY) for 2025. Crucially, the company's audit report disclosed "uncertainty in the company's continuous operational capability" alongside a restatement of accounting errors spanning an entire decade (2015-2024). This is compounded by severe customer concentration, with the top 5 clients generating 69.62% of sales, and a single client representing 34.20% ($22.21 million).

* Capital Occupation and Related-Party Non-Trade Receivables: Several Chinese firms exhibit unusually high concentrations of non-trade "Other Receivables," signaling potential capital occupation by affiliates:

* Poly Union: Holds a staggering $346.6 million (2.49 billion CNY) in "Other Receivables" owed entirely by its affiliated entity, Poly Xinlian Blasting Engineering Group.

* Yahua Group: Disclosed an exceptionally high Other Receivables balance of $199.3 million (1.43 billion CNY).

* Xuefeng Technology: 88.84% of its Other Receivables ($20.9 million / 150.5 million CNY) is concentrated in transactions with its internal related-party, Xinjiang Xuefeng Blasting Engineering Co.

* Off-Balance Sheet Risks: Kailong Chemical carries significant contingent risk via corporate guarantees provided to subsidiaries, with approved guarantee quotas reaching $161.0 million (1.157 billion CNY).

* "Belt and Road" Write-Offs & Bad Debts: Global expansion into frontier markets is yielding credit defaults. Yipuli recorded 100% impairment provisions on receivables from Hunan Zhong'an Resource ($3.07 million / 22.1 million CNY) and China Union Investment (Liberia) Bong Mining ($2.35 million / 16.9 million CNY). Huhua wrote off 100% of receivables from foreign entities PERSIMMON LLC ($1.5 million / 10.8 million CNY) and Myanmar Welfare Mining ($295,000 / 2.1 million CNY).

Litigations and Environmental Clean-Up Liabilities

* Orica vs. CF Industries (The Trans-Pacific Dispute): Orica and its US joint venture (Nelson Brothers) are locked in litigation in Illinois court against CF Industries regarding a long-term (expiring 2031) AN Purchase Agreement. Orica has alleged breach of contract, anti-trust violations, and fraud, projecting legal costs of $32.2 million to $38.7 million ($50.0 million to $60.0 million AUD) for 2026 alone. Escalating this friction, CF Industries issued a Force Majeure notice to Orica in November 2025, declaring an inability to supply industrial AN following a major incident at its Yazoo City plant (which also resulted in a $25.0 million physical asset write-down for CF).

* Under-Provisioned Environmental Liabilities: The balance sheets of Western giants are heavily burdened by multi-decade, sub-surface chemical liabilities:

* Orica: Carries total environmental and decommissioning provisions of $164.7 million ($255.4 million AUD). This is heavily dominated by the Botany groundwater remediation project ($119.7 million / $185.6 million AUD), which requires continuous groundwater extraction and remediation of Dense Non-Aqueous Phase Liquid (DNAPL) contamination until at least 2036.

* Dyno Nobel: Booked $114.2 million ($177.0 million AUD) in environmental liabilities, including a $71.7 million ($111.2 million AUD) remediation provision for the Gibson Island land sale, and $42.2 million ($65.5 million AUD) for the closure of its Geelong facility.

* CF Industries: Identified as a Potentially Responsible Party (PRP) under CERCLA (Superfund) for a former phosphate mine in Georgetown Canyon, Idaho, exposing the firm to indefinite natural resource damage claims.

* Yara International: Carries environmental provisions of $122.0 million (covering industrial site restoration, including the Siilinjärvi apatite mine in Finland) and a further $111.0 million for asset decommissioning.

* Yuntianhua: Disclosed a massive environmental recovery provision of $125.07 million (898.9 million CNY). Unlike the chemical groundwater liabilities of the West, this is geared toward volume-based, visible physical land reclamation, mine geological restoration, and phosphogypsum solid waste treatment to comply with China's "Green Mine" certifications.

In conclusion, while upstream nitrogen manufacturers have extracted robust profitability due to low North American natural gas costs ($3.31/MMBtu realized by CF Industries), their capital-intensive decarbonization pathways are shifting toward blue carbon capture. Downstream, the civil explosives sector's transition to the integrated "Mine Steward" model has successfully driven volume pull-through, but has simultaneously bloated balance sheets with non-trade receivables, unamortized goodwill, and regional credit exposure across developing markets.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."