ideaForge Technology Limited: Strategic Shift Toward Mission-Systems Near Mahape as 94.18% R&D Capitalization Rate Signals EBITDA Inflation Amid Capital Constraints

Date : 2026-07-16

Reading : 242

HDIN Executive Takeaways

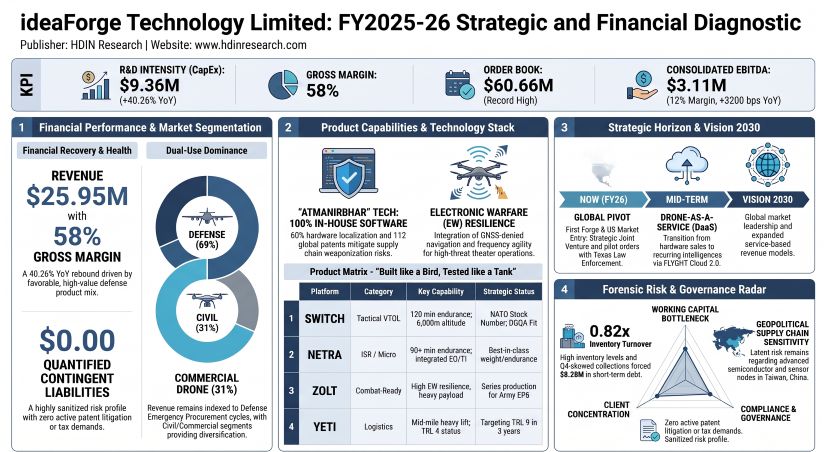

1. ideaForge Technology Limited's FY26 top-line rebounded 40.26% to $25.95M (INR 2,261.29M) with a 58.0% gross margin, but negative ROCE (-3.0%) and deteriorating cash cycles expose deep operational bottlenecks.

2. Aggressive accounting capitalized 94.18% ($9.36M) of product development costs, masking negative organic profitability as statutory auditors flag revenue recognition and R&D capitalization.

3. The parent balance sheet is insulated from downstream credit risks with zero subsidiary debt guarantees, despite a $1.095M net loss at its US sales node.

Figure ideaForge Technology Limited: FY2025-26 Strategic and Financial Diagnostic

Segmental Realities and Margin Compression

Segmental Realities and Margin Compression

A forensic analysis of the consolidated financial statements of ideaForge Technology Limited [NSE: IDEAFORGE] reveals a sharp top-line recovery in FY26 compared to the depressed levels of FY25, although total revenue remains approximately 28% below the FY24 peak. The recovery was driven by a strong performance in the final quarter of the fiscal year, where the company converted approximately 40% of its open order book into recognized revenue, establishing a record order book of $60.66M (INR 5,286.00M).

The company's revenue mix is heavily concentrated in its domestic defense sector, while service-based recurring models and international channels remain in embryonic stages.

Segmental Revenue Splits (FY26)

* Application Sector:

* Defense & Homeland Security (B2G): $17.96M (INR 1,565.39M), representing 69.23% of total revenue, catalyzed by Indian Army Emergency Procurement (EP5 and EP6) windows.

* Civil & Commercial (B2B/B2G): $7.98M (INR 695.66M), representing 30.77% of total revenue, driven by mapping projects and the domestic SVAMITVA scheme.

* Value Chain Component:

* Hardware (UAV Platforms & Spares): $25.08M (INR 2,185.82M), representing 96.67% of total revenues. Embedded software and proprietary autopilot systems are bundled inside these physical platform sales.

* Services & Solutions: $0.86M (INR 75.24M), representing 3.33% of total revenues. Within this segment, Drone-as-a-Service (DaaS) generated $0.43M (INR 37.54M), Maintenance Services (AMC) brought in $0.29M (INR 25.60M), and Training Services contributed $0.05M (INR 4.07M).

* Geographical Footprint:

* Domestic (India): $25.92M (INR 2,259.18M), representing 99.9% of consolidated revenue.

* International Markets: $0.02M (INR 1.88M) on a consolidated basis (accounting for less than 0.1% of total sales). On a standalone basis, FOB export of goods was recorded at $0.10M (INR 9.09M). International touchpoints currently span Bhutan, Nigeria, Oman, and the United States.

Infrastructure Layout and Regional Moats

ideaForge Technology Limited operates a vertically integrated model designed to bypass outsourced contract manufacturing and satisfy the stringent indigenous content guidelines of the Indian Defense Acquisition Procedure (DAP).

Physical Infrastructure Base

* Manufacturing Hub: A single vertically integrated production facility located in the Electronic Zone, MIDC, Mahape, Navi Mumbai, Maharashtra. The plant is certified to AS9100D aerospace standards.

* Research & Development (R&D) Centers: Four dedicated product development hubs, with primary locations in Ghansoli (Aurum Q Parc, Navi Mumbai) and two facilities in Bangalore, Karnataka, housing over 300 engineering personnel.

* International Headquarters: A localized marketing, sales, and distribution node located in Austin, Texas, operating under the wholly-owned subsidiary, ideaForge Technology Inc.

Table Portfolio Benchmarking & Technical Specifications

Intellectual Property and Localization Architecture

To maintain sovereign assurance, the company has completed 100% in-house software development and achieved 60% hardware localization. The company's global intellectual property portfolio consists of 112 patents, including 61 granted patents and 51 pending applications.

Despite this defensive setup, the company remains structurally dependent on foreign supplies for critical sub-systems. Camera sensor technology and ruggedized Ground Control Stations are entirely imported. In FY26, the company imported raw materials valued at $4.75M (INR 413.72M). The concentration of these specialized electronics, semiconductor components, batteries, and electro-optical (EO/IR) sensors in East Asian manufacturing hubs—specifically Taiwan, China—leaves the company vulnerable to regional supply chain disruptions and input cost volatility.

HDIN Institutional Verdict

While ideaForge Technology Limited's executive team highlights its 40.26% top-line expansion and its ranking as the third-largest dual-use drone manufacturer globally according to the 2024 Drone Industry Insights Report, a forensic audit of the financial statements reveals significant operational and accounting friction.

R&D Capitalization and EBITDA Overstatement

The statutory auditors (B S R & Co. LLP) flagged the "Capitalisation of Product under development" as a Key Audit Matter (KAM). In FY26, the company deployed $9.94M (INR 866.08M) toward total product development and R&D. Of this sum, the company expensed only $0.58M (INR 50.42M) to the P&L statement, while capitalizing an aggressive 94.18%, or $9.36M (INR 815.66M), to the balance sheet under Intangible Assets Under Development (IAUD). This brought the total year-end IAUD balance to $12.57M (INR 1,095.12M), which is divided into product development ($12.45M / INR 1,084.88M) and patents ($0.12M / INR 10.24M).

Had the company expensed its R&D outlays under a more conservative policy, its reported EBITDA of $3.11M (INR 271.17M) would have been deeply negative at roughly -$6.25M. This aggressive accounting shields the current-year P&L but leaves a heavy amortization burden for future periods. In FY26, the company already recorded $3.14M (INR 273.52M) in intangible asset amortization based on its standard 3-year useful-life policy for drone designs and autopilot software.

Working Capital Strains and Debt Accumulation

The cash conversion cycle is heavily strained. High inventory requirements needed to satisfy sudden military procurement mandates caused the company's inventory turnover ratio to deteriorate from 1.18x in FY25 to 0.82x in FY26. Concurrently, slow government payment cycles, combined with the fact that approximately 40% of the year's revenue was recognized in the fourth quarter, slowed the trade receivable turnover ratio to 2.43x (representing an average of 150 receivable days).

To bridge this liquidity gap, the company shifted from a historically debt-free capital structure to introducing short-term borrowings of $8.28M (INR 721.31M) in the form of bank overdrafts and cash credit facilities from HDFC Bank, Axis Bank, ICICI, and Exim Bank. This debt was secured via personal guarantees from the promoter group (Ankit Mehta, Rahul Singh, Ashish Bhat, and Vipul Joshi), preserving the parent balance sheet from corporate guarantee exposures but highlighting tight cash flows. This sudden leverage contracted the company's current ratio from 8.58x in FY25 to 2.56x in FY26.

Sub-scale International Subsidiaries

The company’s international expansion is proving highly dilutive to parent capital. During FY26, the parent company completed a direct cash investment of $2.021M (INR 176.10M) into its wholly-owned US subsidiary, ideaForge Technology Inc., bringing the total carrying value of this investment to $3.954M (INR 344.57M).

However, Form AOC-1 disclosures reveal that the US subsidiary recorded an annual turnover of just $0.022M (INR 1.88M) against a net loss after tax of -$1.095M (INR -95.39M). While the parent company has avoided issuing downstream corporate guarantees to secure subsidiary-level debt, the ongoing cash burn at the US sales node remains a drag on parent equity. Furthermore, the anticipated "First Forge Inc." joint venture with First Breach remains non-operational, with zero capital transferred as of March 31, 2026.

Tax Assets and Defensive Balance Sheet Offsets

The company holds unrecognized tax assets that could support future net cash flows. In FY26, the company posted a Consolidated Accounting Loss Before Tax of -$2.29M (INR -199.36M). Under the statutory tax rate of 25.17%, this would typically yield a tax credit of $0.58M (INR 50.18M), but conservative accounting led management to only recognize a Deferred Tax Credit of $0.33M (INR 29.07M), leaving deferred tax assets unrecognized on $1.37M (INR 119.69M) of current-year losses.

As a result, the company has built a gross unutilized tax loss pool of $7.04M (INR 613.65M) across FY25 and FY26, which is set to expire between March 31, 2033, and March 31, 2034. Once the company establishes steady taxable profitability, this accumulated tax shield will offset future cash tax outflows, helping to convert future EBITDA gains directly into operating cash flows.

Additionally, the company's contingent liability profile is highly clean. Total outstanding quantified tax demands fell to $0.00 (INR 0.00M) in FY26, down from the $0.40M (INR 35.22M) reported in FY25. The company's only unquantified risk is a pending Supreme Court of India judgment regarding basic wage calculations for Provident Fund contributions prior to March 31, 2019, which management has assessed as immaterial.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at [http://www.hdinresearch.com](http://www.hdinresearch.com).

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. ideaForge Technology Limited's FY26 top-line rebounded 40.26% to $25.95M (INR 2,261.29M) with a 58.0% gross margin, but negative ROCE (-3.0%) and deteriorating cash cycles expose deep operational bottlenecks.

2. Aggressive accounting capitalized 94.18% ($9.36M) of product development costs, masking negative organic profitability as statutory auditors flag revenue recognition and R&D capitalization.

3. The parent balance sheet is insulated from downstream credit risks with zero subsidiary debt guarantees, despite a $1.095M net loss at its US sales node.

Figure ideaForge Technology Limited: FY2025-26 Strategic and Financial Diagnostic

Segmental Realities and Margin CompressionA forensic analysis of the consolidated financial statements of ideaForge Technology Limited [NSE: IDEAFORGE] reveals a sharp top-line recovery in FY26 compared to the depressed levels of FY25, although total revenue remains approximately 28% below the FY24 peak. The recovery was driven by a strong performance in the final quarter of the fiscal year, where the company converted approximately 40% of its open order book into recognized revenue, establishing a record order book of $60.66M (INR 5,286.00M).

Table Key Financial Performance Metrics (FY2024–FY2026)

| Key Financial Metric | FY2026 (FY2025–26) | FY2025 (FY2024–25) | FY2024 (FY2023–24) | YoY Growth / Change (FY2026 vs. FY2025) |

|---|---|---|---|---|

| Revenue from Operations | $25.95M (INR 2,261.29M) | $18.50M (INR 1,612.16M) | $36.05M (INR 3,141.97M) | +40.26% |

| Gross Profit | $15.05M (INR 1,311.63M) | $6.10M (INR 531.77M) | $17.99M (INR 1,567.39M) | +146.65% |

| Gross Margin | 58.0% | 33.0% | 50.0% | +2,500 bps |

| EBITDA | $3.11M (INR 271.17M) | ($3.62M) (INR -315.28M) | $9.86M (INR 858.94M) | Turnaround from loss to profit |

| EBITDA Margin | 12.0% | -20.0% | 27.0% | +3,200 bps |

| Net Profit (PAT) | ($1.95M) (INR -170.29M) | ($7.15M) (INR -622.78M) | $5.19M (INR 452.68M) | Loss reduced by 72.6% |

| Net Profit Margin | -8.0% | -39.0% | 14.0% | +3,100 bps |

| ROCE | -3.0% | -13.0% | 11.0% | +1,000 bps |

| ROE / RONW | -3.0% | -10.0% | 9.0% | +700 bps |

| Inventory Turnover | 0.82× | 1.18× | N/A | -30.5% |

| Receivable Turnover | 2.43× | 3.10× | N/A | -21.6% |

| Current Ratio | 2.56× | 8.58× | N/A | -70.2% |

| Debt-to-Equity Ratio | 0.12× | 0.00× | N/A | Leverage introduced |

Segmental Revenue Splits (FY26)

* Application Sector:

* Defense & Homeland Security (B2G): $17.96M (INR 1,565.39M), representing 69.23% of total revenue, catalyzed by Indian Army Emergency Procurement (EP5 and EP6) windows.

* Civil & Commercial (B2B/B2G): $7.98M (INR 695.66M), representing 30.77% of total revenue, driven by mapping projects and the domestic SVAMITVA scheme.

* Value Chain Component:

* Hardware (UAV Platforms & Spares): $25.08M (INR 2,185.82M), representing 96.67% of total revenues. Embedded software and proprietary autopilot systems are bundled inside these physical platform sales.

* Services & Solutions: $0.86M (INR 75.24M), representing 3.33% of total revenues. Within this segment, Drone-as-a-Service (DaaS) generated $0.43M (INR 37.54M), Maintenance Services (AMC) brought in $0.29M (INR 25.60M), and Training Services contributed $0.05M (INR 4.07M).

* Geographical Footprint:

* Domestic (India): $25.92M (INR 2,259.18M), representing 99.9% of consolidated revenue.

* International Markets: $0.02M (INR 1.88M) on a consolidated basis (accounting for less than 0.1% of total sales). On a standalone basis, FOB export of goods was recorded at $0.10M (INR 9.09M). International touchpoints currently span Bhutan, Nigeria, Oman, and the United States.

Infrastructure Layout and Regional Moats

ideaForge Technology Limited operates a vertically integrated model designed to bypass outsourced contract manufacturing and satisfy the stringent indigenous content guidelines of the Indian Defense Acquisition Procedure (DAP).

Physical Infrastructure Base

* Manufacturing Hub: A single vertically integrated production facility located in the Electronic Zone, MIDC, Mahape, Navi Mumbai, Maharashtra. The plant is certified to AS9100D aerospace standards.

* Research & Development (R&D) Centers: Four dedicated product development hubs, with primary locations in Ghansoli (Aurum Q Parc, Navi Mumbai) and two facilities in Bangalore, Karnataka, housing over 300 engineering personnel.

* International Headquarters: A localized marketing, sales, and distribution node located in Austin, Texas, operating under the wholly-owned subsidiary, ideaForge Technology Inc.

Table Portfolio Benchmarking & Technical Specifications

| Platform | Category / Portability | Target Application | Key Technical Parameters | Strategic Status / Certifications |

|---|---|---|---|---|

| Q4i | Micro UAV (<2 kg) / Backpack Portable | Tactical ISR and Surveillance | Endurance: <2 hours; Range: >5 km; Payload: EO/TI sensors | DGCA Type Certified |

| Q6 / Q6 V2 / Q6 V2 GEO | Mini UAV (2–25 kg) / Rucksack Portable | Enterprise Mapping and Geospatial Intelligence | Payload options: 2D/3D Mapping, LiDAR, Multispectral, Hyperspectral Sensors | DGCA Type Certified; NATO Stock Number Registered |

| NETRA Series (V4 PRO, V5) | Mini UAV (2–25 kg) / Rucksack Portable | Defense and Homeland Security Applications | Endurance: 90+ minutes; Payload: Integrated EO/TI Systems | Recognized for best-in-class endurance within weight class |

| SWITCH / SWITCH V2 | Mini UAV (2–25 kg) / Rucksack Portable | High-Altitude Tactical Defense | VTOL Hybrid Fixed-Wing Platform; Endurance: 120 minutes; Range: 15 km; Maximum Take-off Altitude: 6,000 m | NATO Stock Number; DGQA Certified; DGCA Type Certified |

| ZOLT | Small UAV Category / Small Vehicle Portable | Combat-Ready Tactical ISR | High payload capacity; Advanced Electronic Warfare (EW) resilience | Secured INR 920M (~$10.5M) Army EP6 cycle orders; Series production underway |

| YETI | Mid-Mile Logistics UAV / Container Portable | Tactical Logistics and Heavy-Lift Operations | Heavy-lift capability designed for extreme terrains | Technology Demonstrator Phase (TRL 4); Targeting TRL 9 within 3 years |

Intellectual Property and Localization Architecture

To maintain sovereign assurance, the company has completed 100% in-house software development and achieved 60% hardware localization. The company's global intellectual property portfolio consists of 112 patents, including 61 granted patents and 51 pending applications.

Despite this defensive setup, the company remains structurally dependent on foreign supplies for critical sub-systems. Camera sensor technology and ruggedized Ground Control Stations are entirely imported. In FY26, the company imported raw materials valued at $4.75M (INR 413.72M). The concentration of these specialized electronics, semiconductor components, batteries, and electro-optical (EO/IR) sensors in East Asian manufacturing hubs—specifically Taiwan, China—leaves the company vulnerable to regional supply chain disruptions and input cost volatility.

HDIN Institutional Verdict

While ideaForge Technology Limited's executive team highlights its 40.26% top-line expansion and its ranking as the third-largest dual-use drone manufacturer globally according to the 2024 Drone Industry Insights Report, a forensic audit of the financial statements reveals significant operational and accounting friction.

R&D Capitalization and EBITDA Overstatement

The statutory auditors (B S R & Co. LLP) flagged the "Capitalisation of Product under development" as a Key Audit Matter (KAM). In FY26, the company deployed $9.94M (INR 866.08M) toward total product development and R&D. Of this sum, the company expensed only $0.58M (INR 50.42M) to the P&L statement, while capitalizing an aggressive 94.18%, or $9.36M (INR 815.66M), to the balance sheet under Intangible Assets Under Development (IAUD). This brought the total year-end IAUD balance to $12.57M (INR 1,095.12M), which is divided into product development ($12.45M / INR 1,084.88M) and patents ($0.12M / INR 10.24M).

Had the company expensed its R&D outlays under a more conservative policy, its reported EBITDA of $3.11M (INR 271.17M) would have been deeply negative at roughly -$6.25M. This aggressive accounting shields the current-year P&L but leaves a heavy amortization burden for future periods. In FY26, the company already recorded $3.14M (INR 273.52M) in intangible asset amortization based on its standard 3-year useful-life policy for drone designs and autopilot software.

Working Capital Strains and Debt Accumulation

The cash conversion cycle is heavily strained. High inventory requirements needed to satisfy sudden military procurement mandates caused the company's inventory turnover ratio to deteriorate from 1.18x in FY25 to 0.82x in FY26. Concurrently, slow government payment cycles, combined with the fact that approximately 40% of the year's revenue was recognized in the fourth quarter, slowed the trade receivable turnover ratio to 2.43x (representing an average of 150 receivable days).

To bridge this liquidity gap, the company shifted from a historically debt-free capital structure to introducing short-term borrowings of $8.28M (INR 721.31M) in the form of bank overdrafts and cash credit facilities from HDFC Bank, Axis Bank, ICICI, and Exim Bank. This debt was secured via personal guarantees from the promoter group (Ankit Mehta, Rahul Singh, Ashish Bhat, and Vipul Joshi), preserving the parent balance sheet from corporate guarantee exposures but highlighting tight cash flows. This sudden leverage contracted the company's current ratio from 8.58x in FY25 to 2.56x in FY26.

Sub-scale International Subsidiaries

The company’s international expansion is proving highly dilutive to parent capital. During FY26, the parent company completed a direct cash investment of $2.021M (INR 176.10M) into its wholly-owned US subsidiary, ideaForge Technology Inc., bringing the total carrying value of this investment to $3.954M (INR 344.57M).

However, Form AOC-1 disclosures reveal that the US subsidiary recorded an annual turnover of just $0.022M (INR 1.88M) against a net loss after tax of -$1.095M (INR -95.39M). While the parent company has avoided issuing downstream corporate guarantees to secure subsidiary-level debt, the ongoing cash burn at the US sales node remains a drag on parent equity. Furthermore, the anticipated "First Forge Inc." joint venture with First Breach remains non-operational, with zero capital transferred as of March 31, 2026.

Tax Assets and Defensive Balance Sheet Offsets

The company holds unrecognized tax assets that could support future net cash flows. In FY26, the company posted a Consolidated Accounting Loss Before Tax of -$2.29M (INR -199.36M). Under the statutory tax rate of 25.17%, this would typically yield a tax credit of $0.58M (INR 50.18M), but conservative accounting led management to only recognize a Deferred Tax Credit of $0.33M (INR 29.07M), leaving deferred tax assets unrecognized on $1.37M (INR 119.69M) of current-year losses.

As a result, the company has built a gross unutilized tax loss pool of $7.04M (INR 613.65M) across FY25 and FY26, which is set to expire between March 31, 2033, and March 31, 2034. Once the company establishes steady taxable profitability, this accumulated tax shield will offset future cash tax outflows, helping to convert future EBITDA gains directly into operating cash flows.

Additionally, the company's contingent liability profile is highly clean. Total outstanding quantified tax demands fell to $0.00 (INR 0.00M) in FY26, down from the $0.40M (INR 35.22M) reported in FY25. The company's only unquantified risk is a pending Supreme Court of India judgment regarding basic wage calculations for Provident Fund contributions prior to March 31, 2019, which management has assessed as immaterial.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at [http://www.hdinresearch.com](http://www.hdinresearch.com).

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."