Nuburu, Inc.: Radical Strategic Pivot to European Defense Platform Amid 216% Share Dilution Threat and Severe Liquidity Deficit

Date : 2026-07-16

Reading : 211

HDIN Market Intelligence Brief

1. Nuburu, Inc. [NYSE American: BURU] has abandoned organic US laser manufacturing following a Q1 2025 foreclosure on its 220-patent portfolio, pivoting to a highly leveraged European dual-use defense holding company model.

2. Cash reserves of $8.26 million as of March 31, 2026, provide less than 2.7 months of operational runway against a monthly cash burn rate of $3.03 million, triggering explicit going-concern warnings from auditors.

3. The proposed $38.0 million S-1 offering, paired with highly dilutive convertible debt and preferred instruments, threatens to expand the common share count by 216%, primarily to service legacy liabilities.

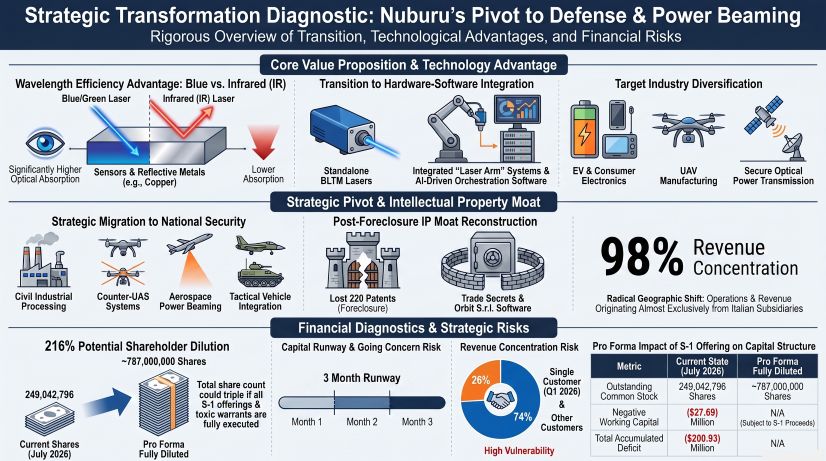

Figure Strategic Transformation Diagnostic: Nuburu's Pivot to Defense & Power Beaming

Segmental Realities, M&A Dilution, and Balance Sheet Distress

Segmental Realities, M&A Dilution, and Balance Sheet Distress

The transition of Nuburu, Inc. [NYSE American: BURU] from an organic industrial laser manufacturer to an inorganic holding company has resulted in severe top-line volatility and structural expense changes.

* S&M expenses in FY 2025 expanded by 898% due to $3.66 million in public relations and branding consulting services linked to the Transformation Plan.

* Net loss for FY 2025 was heavily influenced by non-cash charges, including a $13.89 million loss on warrant liabilities and a $10.13 million debt extinguishment charge.

* The Q1 2026 net loss of $(459,898) was heavily modified by non-cash paper gains, specifically an $11.39 million gain on warrant liabilities and an $8.27 million gain on the fair value of debt.

* The Q1 2026 revenue of $407,644 was entirely inorganic, derived from newly consolidated subsidiaries. Software & Resilience (Orbit S.r.l.) contributed $67,279 (consisting of $48,499 in SaaS/hosted subscriptions and $18,780 in application maintenance), while Hardware & Services (Lyocon S.r.l.) contributed $340,365 (consisting of $317,588 in product sales and $22,777 in professional services).

Customer Concentration and Account Receivables Risks

* Revenue Concentration: In Q1 2026, a single buyer accounted for 74% of total revenue. In FY 2024, two buyers accounted for 50% and 25% of revenues, respectively.

* Accounts Receivable Concentration: As of March 31, 2026, four clients represented 23%, 16%, 16%, and 15% of the total accounts receivable balance, respectively.

Balance Sheet Instability and Solvency Metrics

* Cash Balances: Cash and cash equivalents fluctuated from $209,337 at the end of FY 2024, rising to $24.66 million at the end of FY 2025 (inflated by the Yorkville YA Debenture), and falling to $8.26 million as of March 31, 2026.

* Working Capital Deficit: As of March 31, 2026, current assets stood at $35.69 million against current liabilities of $63.38 million, creating a working capital deficit of $(27.69) million.

* Debt Leverage Profile: The current portion of debt reached $39.67 million as of March 31, 2026. The balance sheet is dominated by two primary liabilities: the $24.09 million outstanding on the December 2025 YA Debenture and the $14.10 million Brick Lane H&K Investment Note. Total debt maturities scheduled for repayment in FY 2026 alone equal $23.52 million.

* Operational Cash Burn and Going Concern: Net cash outflows from operating activities accelerated from $6.61 million in FY 2024 to $16.09 million in FY 2025. In Q1 2026, the cash burn reached $9.10 million, or approximately $3.03 million per month. Based on the March 31, 2026 cash balance of $8.26 million, the operational runway is less than 2.7 months. This has triggered an explicit going-concern explanatory warning from the company's independent auditors.

The Proposed S-1 Financing Structure

* Securities Offered: Up to 244,372,990 shares of Common Stock (or Pre-Funded Warrants) alongside 663,214 shares of Series B Preferred Stock.

* Pricing Terms: A fixed package price of $0.1555 per share of Common Stock (accompanied by 0.002714 shares of Series B Preferred Stock).

* Capital Proceeds: At maximum subscription, the best-efforts offering is designed to raise $38.0 million in gross proceeds ($35.62 million net of a 6.25% placement agent fee).

* Fund Allocation Priorities: Proceeds are contractually mandated to repay debt before funding operations. The first $25.0 million must be directed to clear the YA II PN, LTD. debenture, followed by $1.25 million to retire convertible notes from the Lyocon S.r.l. acquisition. Only the remaining residual balance can be utilized for general working capital.

* Immediate Capital Dilution: The transaction will expand the outstanding common share count from 249,042,796 shares to 493,415,786 shares. New investors will experience an immediate dilution of $0.05 per share against the post-offering pro forma net tangible book value of $0.11 per share.

Geographic Relocation, Defense Alliances, and Italian Regulatory Hurdles

The strategic shift of Nuburu, Inc. [NYSE American: BURU] has led to a geographic relocation of its operational and manufacturing footprint from the United States to Europe.

Physical Footprint Relocation

* Centennial, Colorado (Discontinued): Following a patent foreclosure and a lease default, the centralized U.S. facility was closed, and its manufacturing assets were written down.

* Vigevano, Italy (Lyocon S.r.l.): Prototyping, optical assembly, and clean-room testing are conducted at a leased 27,000 square-foot warehouse facility for an annual rental cost of $16,280.64 (€14,400).

* Ortona, Italy (Tekne S.p.A.): Large-scale vehicle mounting, armor integration, and defense system scaling are outsourced via an industrial network agreement with Tekne S.p.A.

* Kyiv, Ukraine (Operational Office): Nuburu Defense and Tekne S.p.A., in partnership with Engineering Bureau Beryl LLC, established a joint representative office in Kyiv to manage the deployment of the "Tekne Graelion" tactical defense vehicle.

* United States (Maddox Joint Venture): Frontline mobile 3D-printing containers are developed and assembled at Maddox Defense's U.S. facilities.

M&A Accounting Diagnostics under ASC 805

The acquisitions of Orbit S.r.l. and Lyocon S.r.l. on January 15, 2026, were accounted for under the purchase method:

* Orbit S.r.l. Purchase Price Allocation (PPA): Total consideration transferred of $16,592,107 (consisting of $2.0 million cash, a $0.73 million deposit, $12.96 million in common stock, and a $0.89 million pre-existing equity interest).

* *Tangible Assets Acquired:* $3,400,266 (primarily $1.67 million in prepaid expenses, $1.45 million in cash, and $13 in property and equipment).

* *Identified Intangibles:* $2,231,808 (comprising $2,092,320 in developed software technology and $139,488 in customer relationships).

* *Liabilities Assumed:* $6,558,776 (comprising $4.66 million in accrued operating expenses and a $0.79 million related-party contingent liability).

* *Goodwill Recognized:* $17,487,693.

* Lyocon S.r.l. Purchase Price Allocation (PPA): Total consideration of $2,310,558 (consisting of $0.75 million in cash, $1.42 million in initial fair value of convertible notes, and $0.13 million in contingent earn-out liabilities).

* *Tangible Assets Acquired:* $586,079 (including $0.24 million in accounts receivable, $0.24 million in net inventories, and $12,543 in property and equipment).

* *Identified Intangibles:* $678,842 (comprising $348,720 in developed laser technology, $267,352 in customer relationships, and $62,770 in trade names/trademarks).

* *Liabilities Assumed:* $729,521 (including $0.34 million in accrued expenses and $0.17 million in deferred tax liabilities).

* *Goodwill Recognized:* $1,775,158.

Contingent Liabilities and Funding Penalties

* Lyocon EBITDA Earn-Out: Sellers are entitled to performance payments capped at $1,000,000, payable at the end of FY 2028 and FY 2030 (valued on acquisition date at $138,558).

* Lyocon Capital Injection Penalty: Nuburu, Inc. is contractually obligated to inject $1,000,000 in capital into Lyocon S.r.l. ($500,000 at closing, $250,000 at month 12, and $250,000 at month 24). Failure to meet these schedules triggers a penalty of 30% of the $1,000,000 earn-out cap ($300,000).

* Orbit/RegTech Contingent Liability: A legacy liability requiring a 10% cash collection payout on Orbit's commercial revenues through September 30, 2028, capped at €1,000,000 ($1,130,600 USD based on a 1.1306 EUR/USD exchange rate), with an acquisition-date fair value of $790,432.

* Consolidated Intangible Assets: As of March 31, 2026, the balance sheet holds $19.26 million in combined goodwill and $2.79 million in net amortizable intangible assets.

FDI and Defense Regulatory Hurdles

* Italian "Golden Power" FDI Restrictions: The planned $33.57 million (€29.69 million) acquisition of a 70% controlling stake in Tekne S.p.A. and the $1.13 million (€1.0 million) investment in SunCubes S.r.l. are legally blocked pending formal clearance from the Italian Government (Presidenza del Consiglio dei Ministri). Denials or excessive conditions will automatically terminate the transactions.

* Maddox Defense Joint Venture Structure: Formed in February 2026. Phase I requires Nuburu, Inc. to provide up to $4.0 million to fund a frontline mobile 3D-printing container. Phase II will create a joint operating commercial entity ("NewCo") owned 60% by Nuburu, Inc. and 40% by Maddox Defense to act as prime contractor for U.S. and NATO defense contracts.

* Export Controls and Sanctions: Operations are subject to the U.S. International Traffic in Arms Regulations (ITAR), the U.S. Export Administration Regulations (EAR), and the EU Dual-Use Regulation (2021/821). The company is prohibited under the Office of Foreign Assets Control (OFAC) from conducting business within Belarus, Cuba, Iran, Syria, North Korea, Russia, and occupied territories in Ukraine.

Governance Conflicts, Related-Party Exposure, and Institutional Capital Dilution

Following the company's restructuring, the executive leadership has transitioned from technical hardware engineering toward corporate restructuring, resulting in a high density of related-party transactions (RPTs) and significant capital structure changes.

Executive Leadership Profiles and Compensations

* Alessandro Zamboni (Executive Chairman & Co-CEO): Founder of The AvantGarde Group (TAG) and CEO of Supply@ME Capital plc [LSE: SYME]. In FY 2025, Zamboni received a total realized compensation of $1,198,452 (comprising a $380,000 base salary, a $530,000 cash bonus, and $288,452 in stock awards).

* Dario Barisoni (Co-CEO & Director): Former executive at Rohde & Schwarz. In FY 2025, Barisoni received total compensation of $1,101,219 (comprising a $110,000 base salary, a $650,000 cash bonus, and $341,219 in equity and other awards).

* FY 2026 Compensation Structure: Effective January 1, 2026, base salaries for both Co-CEOs were increased to $600,000 each. They are eligible for an annual bonus of up to 140% of their base salary, based on strategic execution (30%), stock performance (20%), and capital/liquidity milestones (30%).

* Board Composition: Shawn Taylor (Independent Director, fractional CFO) and Matteo Ricchebuono (Independent Director, European debt capital markets specialist).

Interconnected Related-Party Transactions (RPTs)

1. The Orbit Acquisition: Acquired from Vanguard Holdings S.r.l. (100% owned by Co-CEO Alessandro Zamboni) for a total consideration of $12.5 million ($3.75 million in cash and $8.75 million in stock settled via ~10.02 million common shares). It includes a commitment to inject up to $5.0 million in working capital.

2. The Supply@ME Capital (SYME) Investment: Nuburu, Inc. invested $5.15 million of its cash reserves into a convertible note in SYME, where Alessandro Zamboni is the founder, CEO, and director, and his holding company (TAG) owns 22.6%. The notes convert into ordinary shares of SYME at a fixed rate of £0.00003 ($0.000039 USD), with warrants exercisable at £0.000039 ($0.000051 USD).

3. Discounted Promissory Notes (TAG and AZ Notes): Alessandro Zamboni advanced loans of $545,000 (via TAG) and $900,000 (via Vanguard) to Nuburu, Inc. In late FY 2025, terms were amended to allow these notes to convert into common stock at 33.3% of the 5-day Volume Weighted Average Price (VWAP), resulting in the issuance of 4,332,525 shares to Zamboni.

4. SFE EI Escrow Shares: SFE EI (where Alessandro Zamboni and Matteo Ricchebuono hold indirect beneficial interests) placed $4.2 million in escrow to guarantee Nuburu's performance obligations for the Tekne S.p.A. acquisition. In exchange, Nuburu, Inc. issued 1,219,831 "Escrow Shares" to SFE EI.

5. Ron Nicol Settlement: Former Executive Chairman Ron Nicol personally paid $1.5 million to fund the company’s Director & Officer (D&O) insurance premiums during a liquidity shortfall. Nuburu, Inc. settled this liability in December 2025 by paying Nicol $1,162,704 in cash.

Intellectual Property Foreclosure and Legal Disputes

* Complete Loss of Patent Portfolio: In Q1 2025, senior secured lenders completed a foreclosure sale on Nuburu's entire global patent portfolio (~220 granted and pending patents covering blue laser welding, single-mode technology, and 3D printing) to extinguish outstanding secured debt. The company currently owns zero foundational patents and relies entirely on trade secrets, software integration, and "Commissioned New IP Rights" through its SunCubes S.r.l. partnership.

* Darbie FINRA Arbitration: On September 19, 2025, J.H. Darbie & Co., Inc. filed a lawsuit alleging breach of a Finder's Fee Agreement and a Financial Advisory Agreement. The federal suit was dismissed for lack of jurisdiction on January 7, 2026, and active arbitration was subsequently initiated under the Financial Industry Regulatory Authority (FINRA) on March 10, 2026.

* Resolved H2 2025 Supplier Defaults: Default judgments settled during the second half of FY 2025 include: CFGI, LLC ($86,826); FICTIV, Inc. ($197,899); Centennial Tech Industrial Owner ($409,278 plus 10% annual interest); ficonTEC, Inc. ($394,274 plus 8% annual interest); and Corporation for International Business ($30,379).

* Cybersecurity Asset Loss: In October 2025, material weaknesses in wire-transfer controls resulted in an unrecoverable phishing loss of $1.0 million.

Capital Structure Diagnostics and Toxic Dilution Mechanisms

As of July 10, 2026, outstanding common stock stood at 249,042,796 shares. The company's capital structure is subject to several dilutive, structured financing agreements:

* Outstanding Convertible Notes (22,086,794 shares issuable as of July 10, 2026):

* *2026 Brick Lane H&K Investment Note: $15.0 million principal, converting at a fixed rate of $0.756 per share, maturing in March 2027.

* *Lyocon Convertible Notes: $1.25 million principal, converting at $1.47 per share, maturing in March 2027.

* *Legacy 2025 Notes: Remaining balances of $198,300 (Brick Lane) and $17,400 (Indigo) converting at floating discount rates of 70% to 100% of the lowest 5-day VWAP.

* *December 2025 YA Debenture: $25.0 million principal senior debt (issued at 7% OID), requiring monthly cash payments of $2.77 million.

* Outstanding Warrants (64,290,933 shares issuable as of July 10, 2026):

* *February 2026 Warrants: 32,792,859 outstanding with a strike price of $0.5489 (stepping down to $0.287 in January 2027, expiring February 2031).

* *December 2025 YA Warrants: ~30 million outstanding, expiring December 2030, with tiered strikes at $1.25 (20.04M shares), $1.871 (5.01M shares), and $2.35 (5.01M shares).

* *Legacy / Placement Agent Warrants: Includes 673,617 warrants at $0.8907 (exp. September 2030), 437,239 warrants at $0.6861 (exp. February 2031), 377,460 warrants at $0.8553 (exp. September 2030), and 172,209 Junior Note Warrants at $24.95 (exp. December 2028).

* Preferred Stock: Series A Preferred (8,988 shares). The proposed Series B Preferred converts using a variable calculation based on the lower of two closing bid prices prior to conversion (floating death spiral structure).

* Standby Equity Purchase Agreement (SEPA): A $100 million agreement with YA II PN, LTD. allowing advances at a 3% discount (97%) to the lowest 3-day VWAP.

* NYSE American Compliance Status: Received notices of noncompliance for falling below minimum stockholder equity thresholds of $2.0 million and $4.0 million. A trading halt in February 2026 due to the stock price falling below $0.10 forced a 1-for-4.99 reverse stock split.

Mathematical Dilution Model (Fully Diluted Scenario)

The table below outlines the changes in outstanding shares under a full conversion scenario:

Under this fully diluted scenario, the total share count will expand by approximately 216%. Consequently, existing common shareholders' voting rights and claims to future earnings will be reduced by more than two-thirds.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. Nuburu, Inc. [NYSE American: BURU] has abandoned organic US laser manufacturing following a Q1 2025 foreclosure on its 220-patent portfolio, pivoting to a highly leveraged European dual-use defense holding company model.

2. Cash reserves of $8.26 million as of March 31, 2026, provide less than 2.7 months of operational runway against a monthly cash burn rate of $3.03 million, triggering explicit going-concern warnings from auditors.

3. The proposed $38.0 million S-1 offering, paired with highly dilutive convertible debt and preferred instruments, threatens to expand the common share count by 216%, primarily to service legacy liabilities.

Figure Strategic Transformation Diagnostic: Nuburu's Pivot to Defense & Power Beaming

Segmental Realities, M&A Dilution, and Balance Sheet DistressThe transition of Nuburu, Inc. [NYSE American: BURU] from an organic industrial laser manufacturer to an inorganic holding company has resulted in severe top-line volatility and structural expense changes.

Table Income Statement & Operating Metrics (FY2024–Q1 2026)

| Metric | FY2024 | FY2025 | Q1 2026 |

|---|---|---|---|

| Organic Revenue | $152,127 | $0 | $0 |

| Inorganic Revenue | $0 | $0 | $407,644 |

| Total Revenue | $152,127 | $0 | $407,644 |

| Cost of Goods Sold (COGS) | $2,201,845 | $181,373 | $652,760 |

| Gross Margin / Gross Profit | ($2,049,718) (Negative) | ($181,373) (Negative) | ($245,116) (Negative) |

| Research & Development (R&D) | $1,820,000 | $174,559 | $67,500 |

| Selling & Marketing (S&M) | $468,074 | $4,670,000 | N/A |

| General & Administrative (G&A) | $8,800,000 | $13,340,000 | N/A |

| Net Income / (Loss) | ($34.51M) | ($79.07M) | ($459,898) |

| Accumulated Deficit | N/A | N/A | $200.93M |

Notes on Financial Reconciliations:

* The organic revenue drop to $0 in FY 2025 was driven by employee furloughs and the cessation of internal laser manufacturing operations.* S&M expenses in FY 2025 expanded by 898% due to $3.66 million in public relations and branding consulting services linked to the Transformation Plan.

* Net loss for FY 2025 was heavily influenced by non-cash charges, including a $13.89 million loss on warrant liabilities and a $10.13 million debt extinguishment charge.

* The Q1 2026 net loss of $(459,898) was heavily modified by non-cash paper gains, specifically an $11.39 million gain on warrant liabilities and an $8.27 million gain on the fair value of debt.

* The Q1 2026 revenue of $407,644 was entirely inorganic, derived from newly consolidated subsidiaries. Software & Resilience (Orbit S.r.l.) contributed $67,279 (consisting of $48,499 in SaaS/hosted subscriptions and $18,780 in application maintenance), while Hardware & Services (Lyocon S.r.l.) contributed $340,365 (consisting of $317,588 in product sales and $22,777 in professional services).

Customer Concentration and Account Receivables Risks

* Revenue Concentration: In Q1 2026, a single buyer accounted for 74% of total revenue. In FY 2024, two buyers accounted for 50% and 25% of revenues, respectively.

* Accounts Receivable Concentration: As of March 31, 2026, four clients represented 23%, 16%, 16%, and 15% of the total accounts receivable balance, respectively.

Balance Sheet Instability and Solvency Metrics

* Cash Balances: Cash and cash equivalents fluctuated from $209,337 at the end of FY 2024, rising to $24.66 million at the end of FY 2025 (inflated by the Yorkville YA Debenture), and falling to $8.26 million as of March 31, 2026.

* Working Capital Deficit: As of March 31, 2026, current assets stood at $35.69 million against current liabilities of $63.38 million, creating a working capital deficit of $(27.69) million.

* Debt Leverage Profile: The current portion of debt reached $39.67 million as of March 31, 2026. The balance sheet is dominated by two primary liabilities: the $24.09 million outstanding on the December 2025 YA Debenture and the $14.10 million Brick Lane H&K Investment Note. Total debt maturities scheduled for repayment in FY 2026 alone equal $23.52 million.

* Operational Cash Burn and Going Concern: Net cash outflows from operating activities accelerated from $6.61 million in FY 2024 to $16.09 million in FY 2025. In Q1 2026, the cash burn reached $9.10 million, or approximately $3.03 million per month. Based on the March 31, 2026 cash balance of $8.26 million, the operational runway is less than 2.7 months. This has triggered an explicit going-concern explanatory warning from the company's independent auditors.

The Proposed S-1 Financing Structure

* Securities Offered: Up to 244,372,990 shares of Common Stock (or Pre-Funded Warrants) alongside 663,214 shares of Series B Preferred Stock.

* Pricing Terms: A fixed package price of $0.1555 per share of Common Stock (accompanied by 0.002714 shares of Series B Preferred Stock).

* Capital Proceeds: At maximum subscription, the best-efforts offering is designed to raise $38.0 million in gross proceeds ($35.62 million net of a 6.25% placement agent fee).

* Fund Allocation Priorities: Proceeds are contractually mandated to repay debt before funding operations. The first $25.0 million must be directed to clear the YA II PN, LTD. debenture, followed by $1.25 million to retire convertible notes from the Lyocon S.r.l. acquisition. Only the remaining residual balance can be utilized for general working capital.

* Immediate Capital Dilution: The transaction will expand the outstanding common share count from 249,042,796 shares to 493,415,786 shares. New investors will experience an immediate dilution of $0.05 per share against the post-offering pro forma net tangible book value of $0.11 per share.

Geographic Relocation, Defense Alliances, and Italian Regulatory Hurdles

The strategic shift of Nuburu, Inc. [NYSE American: BURU] has led to a geographic relocation of its operational and manufacturing footprint from the United States to Europe.

Physical Footprint Relocation

* Centennial, Colorado (Discontinued): Following a patent foreclosure and a lease default, the centralized U.S. facility was closed, and its manufacturing assets were written down.

* Vigevano, Italy (Lyocon S.r.l.): Prototyping, optical assembly, and clean-room testing are conducted at a leased 27,000 square-foot warehouse facility for an annual rental cost of $16,280.64 (€14,400).

* Ortona, Italy (Tekne S.p.A.): Large-scale vehicle mounting, armor integration, and defense system scaling are outsourced via an industrial network agreement with Tekne S.p.A.

* Kyiv, Ukraine (Operational Office): Nuburu Defense and Tekne S.p.A., in partnership with Engineering Bureau Beryl LLC, established a joint representative office in Kyiv to manage the deployment of the "Tekne Graelion" tactical defense vehicle.

* United States (Maddox Joint Venture): Frontline mobile 3D-printing containers are developed and assembled at Maddox Defense's U.S. facilities.

M&A Accounting Diagnostics under ASC 805

The acquisitions of Orbit S.r.l. and Lyocon S.r.l. on January 15, 2026, were accounted for under the purchase method:

* Orbit S.r.l. Purchase Price Allocation (PPA): Total consideration transferred of $16,592,107 (consisting of $2.0 million cash, a $0.73 million deposit, $12.96 million in common stock, and a $0.89 million pre-existing equity interest).

* *Tangible Assets Acquired:* $3,400,266 (primarily $1.67 million in prepaid expenses, $1.45 million in cash, and $13 in property and equipment).

* *Identified Intangibles:* $2,231,808 (comprising $2,092,320 in developed software technology and $139,488 in customer relationships).

* *Liabilities Assumed:* $6,558,776 (comprising $4.66 million in accrued operating expenses and a $0.79 million related-party contingent liability).

* *Goodwill Recognized:* $17,487,693.

* Lyocon S.r.l. Purchase Price Allocation (PPA): Total consideration of $2,310,558 (consisting of $0.75 million in cash, $1.42 million in initial fair value of convertible notes, and $0.13 million in contingent earn-out liabilities).

* *Tangible Assets Acquired:* $586,079 (including $0.24 million in accounts receivable, $0.24 million in net inventories, and $12,543 in property and equipment).

* *Identified Intangibles:* $678,842 (comprising $348,720 in developed laser technology, $267,352 in customer relationships, and $62,770 in trade names/trademarks).

* *Liabilities Assumed:* $729,521 (including $0.34 million in accrued expenses and $0.17 million in deferred tax liabilities).

* *Goodwill Recognized:* $1,775,158.

Contingent Liabilities and Funding Penalties

* Lyocon EBITDA Earn-Out: Sellers are entitled to performance payments capped at $1,000,000, payable at the end of FY 2028 and FY 2030 (valued on acquisition date at $138,558).

* Lyocon Capital Injection Penalty: Nuburu, Inc. is contractually obligated to inject $1,000,000 in capital into Lyocon S.r.l. ($500,000 at closing, $250,000 at month 12, and $250,000 at month 24). Failure to meet these schedules triggers a penalty of 30% of the $1,000,000 earn-out cap ($300,000).

* Orbit/RegTech Contingent Liability: A legacy liability requiring a 10% cash collection payout on Orbit's commercial revenues through September 30, 2028, capped at €1,000,000 ($1,130,600 USD based on a 1.1306 EUR/USD exchange rate), with an acquisition-date fair value of $790,432.

* Consolidated Intangible Assets: As of March 31, 2026, the balance sheet holds $19.26 million in combined goodwill and $2.79 million in net amortizable intangible assets.

FDI and Defense Regulatory Hurdles

* Italian "Golden Power" FDI Restrictions: The planned $33.57 million (€29.69 million) acquisition of a 70% controlling stake in Tekne S.p.A. and the $1.13 million (€1.0 million) investment in SunCubes S.r.l. are legally blocked pending formal clearance from the Italian Government (Presidenza del Consiglio dei Ministri). Denials or excessive conditions will automatically terminate the transactions.

* Maddox Defense Joint Venture Structure: Formed in February 2026. Phase I requires Nuburu, Inc. to provide up to $4.0 million to fund a frontline mobile 3D-printing container. Phase II will create a joint operating commercial entity ("NewCo") owned 60% by Nuburu, Inc. and 40% by Maddox Defense to act as prime contractor for U.S. and NATO defense contracts.

* Export Controls and Sanctions: Operations are subject to the U.S. International Traffic in Arms Regulations (ITAR), the U.S. Export Administration Regulations (EAR), and the EU Dual-Use Regulation (2021/821). The company is prohibited under the Office of Foreign Assets Control (OFAC) from conducting business within Belarus, Cuba, Iran, Syria, North Korea, Russia, and occupied territories in Ukraine.

Governance Conflicts, Related-Party Exposure, and Institutional Capital Dilution

Following the company's restructuring, the executive leadership has transitioned from technical hardware engineering toward corporate restructuring, resulting in a high density of related-party transactions (RPTs) and significant capital structure changes.

Executive Leadership Profiles and Compensations

* Alessandro Zamboni (Executive Chairman & Co-CEO): Founder of The AvantGarde Group (TAG) and CEO of Supply@ME Capital plc [LSE: SYME]. In FY 2025, Zamboni received a total realized compensation of $1,198,452 (comprising a $380,000 base salary, a $530,000 cash bonus, and $288,452 in stock awards).

* Dario Barisoni (Co-CEO & Director): Former executive at Rohde & Schwarz. In FY 2025, Barisoni received total compensation of $1,101,219 (comprising a $110,000 base salary, a $650,000 cash bonus, and $341,219 in equity and other awards).

* FY 2026 Compensation Structure: Effective January 1, 2026, base salaries for both Co-CEOs were increased to $600,000 each. They are eligible for an annual bonus of up to 140% of their base salary, based on strategic execution (30%), stock performance (20%), and capital/liquidity milestones (30%).

* Board Composition: Shawn Taylor (Independent Director, fractional CFO) and Matteo Ricchebuono (Independent Director, European debt capital markets specialist).

Interconnected Related-Party Transactions (RPTs)

1. The Orbit Acquisition: Acquired from Vanguard Holdings S.r.l. (100% owned by Co-CEO Alessandro Zamboni) for a total consideration of $12.5 million ($3.75 million in cash and $8.75 million in stock settled via ~10.02 million common shares). It includes a commitment to inject up to $5.0 million in working capital.

2. The Supply@ME Capital (SYME) Investment: Nuburu, Inc. invested $5.15 million of its cash reserves into a convertible note in SYME, where Alessandro Zamboni is the founder, CEO, and director, and his holding company (TAG) owns 22.6%. The notes convert into ordinary shares of SYME at a fixed rate of £0.00003 ($0.000039 USD), with warrants exercisable at £0.000039 ($0.000051 USD).

3. Discounted Promissory Notes (TAG and AZ Notes): Alessandro Zamboni advanced loans of $545,000 (via TAG) and $900,000 (via Vanguard) to Nuburu, Inc. In late FY 2025, terms were amended to allow these notes to convert into common stock at 33.3% of the 5-day Volume Weighted Average Price (VWAP), resulting in the issuance of 4,332,525 shares to Zamboni.

4. SFE EI Escrow Shares: SFE EI (where Alessandro Zamboni and Matteo Ricchebuono hold indirect beneficial interests) placed $4.2 million in escrow to guarantee Nuburu's performance obligations for the Tekne S.p.A. acquisition. In exchange, Nuburu, Inc. issued 1,219,831 "Escrow Shares" to SFE EI.

5. Ron Nicol Settlement: Former Executive Chairman Ron Nicol personally paid $1.5 million to fund the company’s Director & Officer (D&O) insurance premiums during a liquidity shortfall. Nuburu, Inc. settled this liability in December 2025 by paying Nicol $1,162,704 in cash.

Intellectual Property Foreclosure and Legal Disputes

* Complete Loss of Patent Portfolio: In Q1 2025, senior secured lenders completed a foreclosure sale on Nuburu's entire global patent portfolio (~220 granted and pending patents covering blue laser welding, single-mode technology, and 3D printing) to extinguish outstanding secured debt. The company currently owns zero foundational patents and relies entirely on trade secrets, software integration, and "Commissioned New IP Rights" through its SunCubes S.r.l. partnership.

* Darbie FINRA Arbitration: On September 19, 2025, J.H. Darbie & Co., Inc. filed a lawsuit alleging breach of a Finder's Fee Agreement and a Financial Advisory Agreement. The federal suit was dismissed for lack of jurisdiction on January 7, 2026, and active arbitration was subsequently initiated under the Financial Industry Regulatory Authority (FINRA) on March 10, 2026.

* Resolved H2 2025 Supplier Defaults: Default judgments settled during the second half of FY 2025 include: CFGI, LLC ($86,826); FICTIV, Inc. ($197,899); Centennial Tech Industrial Owner ($409,278 plus 10% annual interest); ficonTEC, Inc. ($394,274 plus 8% annual interest); and Corporation for International Business ($30,379).

* Cybersecurity Asset Loss: In October 2025, material weaknesses in wire-transfer controls resulted in an unrecoverable phishing loss of $1.0 million.

Capital Structure Diagnostics and Toxic Dilution Mechanisms

As of July 10, 2026, outstanding common stock stood at 249,042,796 shares. The company's capital structure is subject to several dilutive, structured financing agreements:

* Outstanding Convertible Notes (22,086,794 shares issuable as of July 10, 2026):

* *2026 Brick Lane H&K Investment Note: $15.0 million principal, converting at a fixed rate of $0.756 per share, maturing in March 2027.

* *Lyocon Convertible Notes: $1.25 million principal, converting at $1.47 per share, maturing in March 2027.

* *Legacy 2025 Notes: Remaining balances of $198,300 (Brick Lane) and $17,400 (Indigo) converting at floating discount rates of 70% to 100% of the lowest 5-day VWAP.

* *December 2025 YA Debenture: $25.0 million principal senior debt (issued at 7% OID), requiring monthly cash payments of $2.77 million.

* Outstanding Warrants (64,290,933 shares issuable as of July 10, 2026):

* *February 2026 Warrants: 32,792,859 outstanding with a strike price of $0.5489 (stepping down to $0.287 in January 2027, expiring February 2031).

* *December 2025 YA Warrants: ~30 million outstanding, expiring December 2030, with tiered strikes at $1.25 (20.04M shares), $1.871 (5.01M shares), and $2.35 (5.01M shares).

* *Legacy / Placement Agent Warrants: Includes 673,617 warrants at $0.8907 (exp. September 2030), 437,239 warrants at $0.6861 (exp. February 2031), 377,460 warrants at $0.8553 (exp. September 2030), and 172,209 Junior Note Warrants at $24.95 (exp. December 2028).

* Preferred Stock: Series A Preferred (8,988 shares). The proposed Series B Preferred converts using a variable calculation based on the lower of two closing bid prices prior to conversion (floating death spiral structure).

* Standby Equity Purchase Agreement (SEPA): A $100 million agreement with YA II PN, LTD. allowing advances at a 3% discount (97%) to the lowest 3-day VWAP.

* NYSE American Compliance Status: Received notices of noncompliance for falling below minimum stockholder equity thresholds of $2.0 million and $4.0 million. A trading halt in February 2026 due to the stock price falling below $0.10 forced a 1-for-4.99 reverse stock split.

Mathematical Dilution Model (Fully Diluted Scenario)

The table below outlines the changes in outstanding shares under a full conversion scenario:

| Equity Category | Share Count Impact | Fully Diluted Ownership (%) |

|---|---|---|

| Current Outstanding Common Stock (July 10, 2026) | 249,042,796 | 31.6% |

| Proposed S-1 Common Stock Issuance | +244,372,990 | 31.1% |

| New Series B Preferred Stock Conversion | +205,627,010 | 26.1% |

| Outstanding Warrants (July 10, 2026) | +64,290,933 | 8.2% |

| Convertible Notes / Series A Preferred Conversion | +22,095,782 | 2.8% |

| Other Outstanding Equity Commitments | +1,559,487 | 0.2% |

| Fully Diluted Share Count | ~787,000,000 | 100.0% |

Under this fully diluted scenario, the total share count will expand by approximately 216%. Consequently, existing common shareholders' voting rights and claims to future earnings will be reduced by more than two-thirds.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."