AngioDynamics, Inc.: Transition to Globally Outsourced Manufacturing Near New York Facilities as 18.4% Med Tech Segment Growth Signals High-Margin Revenue Pivot

Date : 2026-07-17

Reading : 138

HDIN Market Intelligence Brief

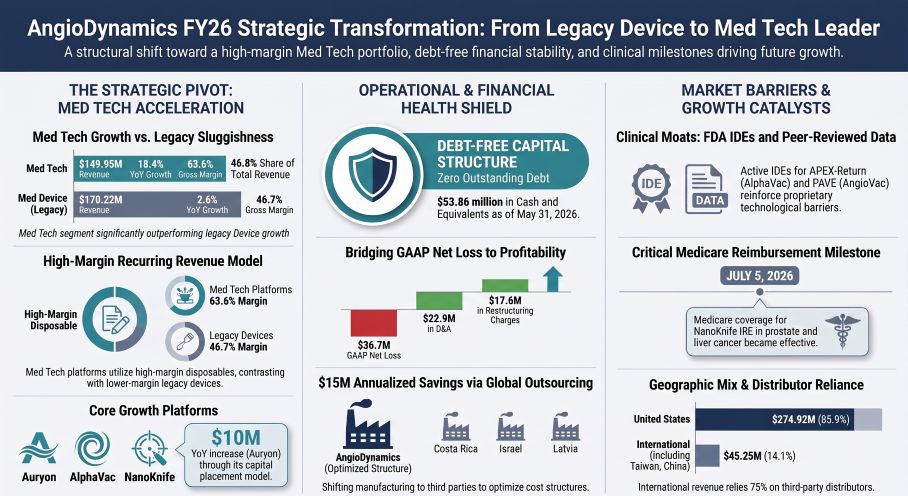

1. AngioDynamics, Inc. [NASDAQ: ANGO] delivered 9.5% YoY revenue growth to $320.17 million in FY26, driven by an 18.4% expansion in its high-margin Med Tech segment ($149.95 million).

2. The company is finalizing its manufacturing transition from New York to global third-party contractors, targeting $15.0 million in annualized cost savings beginning in Q1 FY27.

3. A debt-free capital structure and positive $3.09 million operating cash flow buffer the firm against impending CEO succession and unquantified port-product liability litigation.

Figure AngioDynamics FY26 Strategic Transformation: From Legacy Device to Med Tech Leader

Segmental Realities and Margin Expansion Dynamics

AngioDynamics, Inc. manages its commercial operations through two primary reporting segments, yielding a consolidated top-line of $320.17 million in Fiscal Year 2026 (FY26), up 9.5% compared to $292.50 million in FY25.

* Geographic Sales Mix: Domestic sales rose by $23.94 million YoY to $274.92 million, representing 85.9% of total net sales. International sales expanded by $3.73 million YoY to $45.25 million (14.1% of total net sales), with independent third-party distributors generating approximately 75% of total international revenues.

* Gross Margin Architecture: Consolidated gross profit rose to $174.89 million in FY26 from $157.71 million in FY25. Gross margin expanded by 70 basis points (bps) to 54.6%. The expansion was primarily driven by favorable sales volume, pricing, and product mix contributing positive $26.6 million, alongside a $0.9 million benefit from the strategic transition to third-party contract manufacturers. These core operational tailwinds offset headwinds of $5.2 million in higher production and operations costs, $3.2 million in global tariffs, and $1.9 million in broader inflationary pressures.

* GAAP to Non-GAAP Reconciliation & EBITDA Proxies: The company reported a GAAP Net Loss of $36.74 million in FY26, widening slightly from a Net Loss of $33.99 million in FY25. Operating loss stood at $39.93 million. To bridge the GAAP loss to an Adjusted EBITDA run-rate, the following non-cash and non-recurring items are isolated:

* Depreciation and Amortization: $22.96 million (comprising $10.68 million in intangible amortization and $12.28 million in property and equipment depreciation).

* Stock-Based Compensation: $13.96 million.

* Acquisition, Restructuring, and Other Net Items: $17.60 million (featuring zero mergers and acquisitions expenses in FY26, down from $0.74 million in FY25). This figure includes $13.12 million in plant closure expenses.

* Asset Impairment Stabilization: The company recorded $0 in goodwill and $0 in intangible asset impairments in FY26, stabilizing from a massive $159.48 million goodwill impairment and a $6.26 million intangible asset impairment in FY24.

* Balance Sheet and Liquidity Strength: Operating cash flow experienced a positive inflection, generating $3.09 million in FY26 compared to a cash burn of $10.13 million in FY25 (a $13.20 million recovery). This turnaround was heavily supported by a $10.05 million working capital reduction from inventory optimization. Cash and cash equivalents stood at $53.86 million as of May 31, 2026. The capital structure is entirely debt-free; the $25.0 million secured revolving credit facility established on May 28, 2025, remains undrawn with zero outstanding balance.

* Tax Optimization and Valuation Allowance: As of May 31, 2026, the company held $72.34 million in gross Deferred Tax Assets (DTAs)—composed of $46.34 million in net operating loss (NOL) carryforwards, $11.90 million in temporarily non-deductible expenses, and $7.85 million in federal and state R&D tax credits—offset by $12.07 million in Deferred Tax Liabilities (DTLs) related to depreciation and amortization. Due to prolonged GAAP unprofitability, management recorded a $65.49 million valuation allowance against the net DTAs (up from $58.44 million in FY25), leaving a net DTL of $5.23 million on the balance sheet.

* Commercial Concentration & Procurement Pressures: Credit risk is limited as no single customer, distributor, or health system exceeded the 10% consolidated net sales threshold in FY26. However, purchasing consolidation from Group Purchasing Organizations (GPOs) and Integrated Delivery Networks (IDNs) limits pricing power, compressing Average Selling Prices (ASPs). Under multi-year supply agreements, the company must pay administrative fees and offer volume-based rebates directly to GPOs, reducing recognized top-line revenue. This pressure is compounded as hospitals absorb disposable costs under fixed-rate procedural models, such as Medicare’s diagnosis-related group system.

Infrastructure Layout and Regional Moats

* Manufacturing Restructuring & Footprint Optimization: Historically centralized in Queensbury and Glens Falls, New York, AngioDynamics, Inc. is executing a transition to an outsourced global supply chain. In December 2024, the company completed a sale-and-leaseback of these New York facilities, generating $6.7 million in gross proceeds. A streamlined presence is maintained in Queensbury for customer service, logistics, shipping, quality control, and select product manufacturing, while other production lines are migrating to contract manufacturers in Costa Rica, Latvia, Italy, Israel, and China.

* Transition Costs and Annualized Savings: The restructuring plan is scheduled for finalization in Q1 FY27 and is projected to deliver $15.0 million in annualized cost savings. Total restructuring costs are budgeted at $33.40 million to $38.40 million. This budget comprises:

* Facilities Closeout: $16.0 million to $17.0 million.

* Outside Consultants: $7.5 million to $8.5 million.

* Employee Termination Benefits: $6.2 million to $7.2 million.

* Validation Expenses: $3.4 million to $4.4 million.

As of May 31, 2026, the company has cumulatively recorded $36.4 million in restructuring charges (including $13.12 million in plant closure expenses in FY26). Cash outflows for restructuring activities totaled $11.96 million during FY26. The shift directly impacts the company's streamlined workforce, which stood at approximately 632 full-time employees as of May 31, 2026.

* Divestiture Milestone: In Q3 FY26, the company finalized the manufacturing transfer of its PICC and Midline businesses to Spectrum Vascular, triggering a $5.0 million milestone cash payment.

* Research & Development Investment: R&D expenditure increased 12.3% YoY to $29.45 million in FY26 (9.2% of net sales), up from $26.22 million in FY25 (9.0% of net sales). The $3.23 million absolute increase was driven by a $2.0 million allocation to clinical trial timing and project expenditures, alongside a $1.2 million increase in R&D compensation and benefits.

* Flagship Tech Portfolios and Clinical Pipeline:

* *Auryon (Laser Atherectomy)*: Employs a proprietary 355nm short-pulse laser for above- and below-the-knee peripheral arterial disease (PAD) treatment, minimizing vessel wall endothelial damage. Auryon was the largest absolute growth driver, generating a $10.0 million YoY sales increase. In FY26, the company invested $3.4 million in cash to add placement and evaluation units. Active clinical trials include the AMBITION BTK trial targeting below-the-knee disease.

* *Mechanical Thrombectomy (AlphaVac & AngioVac)*: Combined thrombus management sales grew by $4.6 million, driven by AlphaVac (+$4.7 million) and AngioVac (+$0.6 million), which offset a $0.7 million decline in legacy thrombolytic catheters. AlphaVac utilizes a non-surgical, nitinol-reinforced funnel distal tip, eliminating perfusionist support. The AlphaVac F1885 system received FDA 510(k) clearance for pulmonary embolism (PE). Active clinical trials include the APEX-Return study under FDA IDE (evaluating the AlphaReturn Blood Management System with AlphaVac F1885) and the PAVE study under FDA IDE (evaluating AngioVac for right-sided infective endocarditis). The company enrolled the first patients in the RECOVER-AV trial in FY26.

* *NanoKnife (Irreversible Electroporation - IRE)*: Utilizes low-energy direct current pulses to ablate soft tissue while preserving surrounding structures. NanoKnife sales grew by $8.6 million in FY26 across capital equipment and disposable needles (up to six probes per procedure). Key milestones include securing a Palmetto Local Coverage Determination (LCD) granting Medicare reimbursement coverage in prostate and liver cancer, effective July 5, 2026. This follows an expanded FDA 510(k) clearance for prostate tissue ablation in December 2024 and European MDR CE mark approval in February 2026 (prostate, pancreas, kidney, liver). Active clinical trials include the RELIEF BPH study (Benign Prostatic Hyperplasia) under FDA IDE and the PRESERVE trial (prostate cancer) published in *European Urology* with 2-year follow-up data presented at AUA 2026.

* *BioFlo*: Features Endexo Technology, a proprietary non-eluting polymer blended into polyurethane to resist thrombus accumulation.

* Product Liability, Patent Litigation, and Legal Realities:

* *Defensive Settlement*: A patent settlement with C.R. Bard, Inc. (Becton Dickinson [NYSE: BDX]) regarding implantable port products was settled on March 31, 2024. Following an initial $7.0 million lump-sum paid by March 31, 2025, AngioDynamics, Inc. must pay six minimum annual payments of $2.5 million to BD (commencing in FY25), leaving a total of $9.4 million payable as of May 31, 2026 ($2.5 million short-term, $6.9 million long-term). A December 2025 Federal Circuit ruling affirmed port patent invalidity in favor of AngioDynamics, Inc., negating any variable 6% royalty payments above the $2.5 million minimum.

* *Offensive Litigation*: On April 23, 2026, the company filed an offensive patent infringement lawsuit in Delaware against Endovascular Engineering, Inc., alleging its Hēlo Thrombectomy System violates patents on the proprietary self-expanding funnel design used in AlphaVac and AngioVac.

* *Product Liability MDL*: The company is defending against multidistrict litigation consolidated in the Southern District of California regarding personal injury claims related to its port products. Product liability insurance is capped at $10.0 million per claim and $10.0 million in the annual aggregate, subject to a $500,000 per occurrence self-retention and a $2.0 million aggregate self-insured retention.

* *Strategic Insulation*: The flagship high-margin NanoKnife and Auryon platforms are completely insulated from all ongoing port-related litigation, patent disputes, and BD royalty obligations.

* *Compliance & Macro Hurdles*: The global expansion exposes the firm to FCPA, Stark Law, and Anti-Kickback Statute risks. Geopolitical friction, including conflicts in Europe and the Middle East, along with US-China trade disputes, led to a negative gross margin impact of $3.2 million from tariffs in FY26. Additionally, European Union Medical Device Regulation (MDR) certification delays (typically 12 to 18 months or longer) forced the company to discontinue selective legacy products in the EU.

* Corporate Governance and Executive Transition: James C. Clemmer, President and CEO since April 2016, announced his retirement, effective the earlier of November 30, 2026, or the appointment of a successor. The board has initiated a formal search, and the company incurred $1.63 million in CEO transition and management retention expenses in FY26.

HDIN Institutional Verdict

The financial performance of AngioDynamics, Inc. in FY26 reflects a successful segment re-weighting, but the execution risk remains exceptionally concentrated in the next 12 months.

* High-Margin Med Tech Substitution: The deliberate cannibalization of the low-margin legacy Med Device catheter portfolio (-$0.7 million in older thrombolytic catheters) in favor of the high-margin, clinically differentiated Med Tech segment (63.6% GM vs. 46.7% GM) is fundamentally reshaping the company’s margin scalability. The $10.0 million growth in Auryon and the upcoming Medicare coverage for NanoKnife (effective July 5, 2026) act as high-conviction growth engines.

* Restructuring and CEO Continuity Risk: Transitioning to an asset-light, outsourced global supply chain across Costa Rica, Latvia, Italy, Israel, and China removes New York fixed overhead and targets $15.0 million in annualized savings. However, this pivot increases reliance on third-party Quality System Regulations (QSR) compliance and elevates exposure to bilateral tariff volatility, which already cost the company $3.2 million in FY26. Executing this supply chain migration simultaneously with a CEO succession by November 30, 2026, and unquantified Southern District of California port product liability claims, presents material execution risks.

* Liquidity & Capital Structure Resilience: Despite these headwinds, AngioDynamics, Inc. is entering this transition phase from a position of relative balance sheet strength. A debt-free capital structure, $53.86 million in cash, and the positive $3.09 million operating cash flow inflection—driven by a $10.05 million working capital inventory reduction—provide a solid capital buffer. If the new leadership can successfully execute the supply chain transition and leverage the Palmetto LCD prostate reimbursement pathway, the eventual reversal of the company’s $65.49 million deferred tax asset valuation allowance will deliver a highly material non-cash benefit to future GAAP earnings.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at [http://www.hdinresearch.com](http://www.hdinresearch.com).

2026 AI Transparency Footer

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

1. AngioDynamics, Inc. [NASDAQ: ANGO] delivered 9.5% YoY revenue growth to $320.17 million in FY26, driven by an 18.4% expansion in its high-margin Med Tech segment ($149.95 million).

2. The company is finalizing its manufacturing transition from New York to global third-party contractors, targeting $15.0 million in annualized cost savings beginning in Q1 FY27.

3. A debt-free capital structure and positive $3.09 million operating cash flow buffer the firm against impending CEO succession and unquantified port-product liability litigation.

Figure AngioDynamics FY26 Strategic Transformation: From Legacy Device to Med Tech Leader

Segmental Realities and Margin Expansion Dynamics

AngioDynamics, Inc. manages its commercial operations through two primary reporting segments, yielding a consolidated top-line of $320.17 million in Fiscal Year 2026 (FY26), up 9.5% compared to $292.50 million in FY25.

Table Segment Financial Performance (FY2026)

| Segment | FY2026 Net Sales (USD M) | YoY Growth | Revenue Share | Gross Margin | Gross Profit (USD M) | Core Growth Drivers / Product Portfolio |

|---|---|---|---|---|---|---|

| Med Tech | $149.95M | 18.4% | 46.8% | 63.6% | $95.36M | Auryon, NanoKnife, AlphaVac, AngioVac |

| Med Device | $170.22M | 2.6% | 53.2% | 46.7% | $79.54M | Core, Venous, Ports, Legacy Oncology |

| Consolidated Total | $320.17M | 9.5% | 100.0% | 54.6% | $174.89M | Volume/Mix Contribution: +$26.6M; Outsourcing Impact: +$0.9M |

* Geographic Sales Mix: Domestic sales rose by $23.94 million YoY to $274.92 million, representing 85.9% of total net sales. International sales expanded by $3.73 million YoY to $45.25 million (14.1% of total net sales), with independent third-party distributors generating approximately 75% of total international revenues.

* Gross Margin Architecture: Consolidated gross profit rose to $174.89 million in FY26 from $157.71 million in FY25. Gross margin expanded by 70 basis points (bps) to 54.6%. The expansion was primarily driven by favorable sales volume, pricing, and product mix contributing positive $26.6 million, alongside a $0.9 million benefit from the strategic transition to third-party contract manufacturers. These core operational tailwinds offset headwinds of $5.2 million in higher production and operations costs, $3.2 million in global tariffs, and $1.9 million in broader inflationary pressures.

* GAAP to Non-GAAP Reconciliation & EBITDA Proxies: The company reported a GAAP Net Loss of $36.74 million in FY26, widening slightly from a Net Loss of $33.99 million in FY25. Operating loss stood at $39.93 million. To bridge the GAAP loss to an Adjusted EBITDA run-rate, the following non-cash and non-recurring items are isolated:

* Depreciation and Amortization: $22.96 million (comprising $10.68 million in intangible amortization and $12.28 million in property and equipment depreciation).

* Stock-Based Compensation: $13.96 million.

* Acquisition, Restructuring, and Other Net Items: $17.60 million (featuring zero mergers and acquisitions expenses in FY26, down from $0.74 million in FY25). This figure includes $13.12 million in plant closure expenses.

* Asset Impairment Stabilization: The company recorded $0 in goodwill and $0 in intangible asset impairments in FY26, stabilizing from a massive $159.48 million goodwill impairment and a $6.26 million intangible asset impairment in FY24.

* Balance Sheet and Liquidity Strength: Operating cash flow experienced a positive inflection, generating $3.09 million in FY26 compared to a cash burn of $10.13 million in FY25 (a $13.20 million recovery). This turnaround was heavily supported by a $10.05 million working capital reduction from inventory optimization. Cash and cash equivalents stood at $53.86 million as of May 31, 2026. The capital structure is entirely debt-free; the $25.0 million secured revolving credit facility established on May 28, 2025, remains undrawn with zero outstanding balance.

* Tax Optimization and Valuation Allowance: As of May 31, 2026, the company held $72.34 million in gross Deferred Tax Assets (DTAs)—composed of $46.34 million in net operating loss (NOL) carryforwards, $11.90 million in temporarily non-deductible expenses, and $7.85 million in federal and state R&D tax credits—offset by $12.07 million in Deferred Tax Liabilities (DTLs) related to depreciation and amortization. Due to prolonged GAAP unprofitability, management recorded a $65.49 million valuation allowance against the net DTAs (up from $58.44 million in FY25), leaving a net DTL of $5.23 million on the balance sheet.

* Commercial Concentration & Procurement Pressures: Credit risk is limited as no single customer, distributor, or health system exceeded the 10% consolidated net sales threshold in FY26. However, purchasing consolidation from Group Purchasing Organizations (GPOs) and Integrated Delivery Networks (IDNs) limits pricing power, compressing Average Selling Prices (ASPs). Under multi-year supply agreements, the company must pay administrative fees and offer volume-based rebates directly to GPOs, reducing recognized top-line revenue. This pressure is compounded as hospitals absorb disposable costs under fixed-rate procedural models, such as Medicare’s diagnosis-related group system.

Infrastructure Layout and Regional Moats

* Manufacturing Restructuring & Footprint Optimization: Historically centralized in Queensbury and Glens Falls, New York, AngioDynamics, Inc. is executing a transition to an outsourced global supply chain. In December 2024, the company completed a sale-and-leaseback of these New York facilities, generating $6.7 million in gross proceeds. A streamlined presence is maintained in Queensbury for customer service, logistics, shipping, quality control, and select product manufacturing, while other production lines are migrating to contract manufacturers in Costa Rica, Latvia, Italy, Israel, and China.

* Transition Costs and Annualized Savings: The restructuring plan is scheduled for finalization in Q1 FY27 and is projected to deliver $15.0 million in annualized cost savings. Total restructuring costs are budgeted at $33.40 million to $38.40 million. This budget comprises:

* Facilities Closeout: $16.0 million to $17.0 million.

* Outside Consultants: $7.5 million to $8.5 million.

* Employee Termination Benefits: $6.2 million to $7.2 million.

* Validation Expenses: $3.4 million to $4.4 million.

As of May 31, 2026, the company has cumulatively recorded $36.4 million in restructuring charges (including $13.12 million in plant closure expenses in FY26). Cash outflows for restructuring activities totaled $11.96 million during FY26. The shift directly impacts the company's streamlined workforce, which stood at approximately 632 full-time employees as of May 31, 2026.

* Divestiture Milestone: In Q3 FY26, the company finalized the manufacturing transfer of its PICC and Midline businesses to Spectrum Vascular, triggering a $5.0 million milestone cash payment.

* Research & Development Investment: R&D expenditure increased 12.3% YoY to $29.45 million in FY26 (9.2% of net sales), up from $26.22 million in FY25 (9.0% of net sales). The $3.23 million absolute increase was driven by a $2.0 million allocation to clinical trial timing and project expenditures, alongside a $1.2 million increase in R&D compensation and benefits.

* Flagship Tech Portfolios and Clinical Pipeline:

* *Auryon (Laser Atherectomy)*: Employs a proprietary 355nm short-pulse laser for above- and below-the-knee peripheral arterial disease (PAD) treatment, minimizing vessel wall endothelial damage. Auryon was the largest absolute growth driver, generating a $10.0 million YoY sales increase. In FY26, the company invested $3.4 million in cash to add placement and evaluation units. Active clinical trials include the AMBITION BTK trial targeting below-the-knee disease.

* *Mechanical Thrombectomy (AlphaVac & AngioVac)*: Combined thrombus management sales grew by $4.6 million, driven by AlphaVac (+$4.7 million) and AngioVac (+$0.6 million), which offset a $0.7 million decline in legacy thrombolytic catheters. AlphaVac utilizes a non-surgical, nitinol-reinforced funnel distal tip, eliminating perfusionist support. The AlphaVac F1885 system received FDA 510(k) clearance for pulmonary embolism (PE). Active clinical trials include the APEX-Return study under FDA IDE (evaluating the AlphaReturn Blood Management System with AlphaVac F1885) and the PAVE study under FDA IDE (evaluating AngioVac for right-sided infective endocarditis). The company enrolled the first patients in the RECOVER-AV trial in FY26.

* *NanoKnife (Irreversible Electroporation - IRE)*: Utilizes low-energy direct current pulses to ablate soft tissue while preserving surrounding structures. NanoKnife sales grew by $8.6 million in FY26 across capital equipment and disposable needles (up to six probes per procedure). Key milestones include securing a Palmetto Local Coverage Determination (LCD) granting Medicare reimbursement coverage in prostate and liver cancer, effective July 5, 2026. This follows an expanded FDA 510(k) clearance for prostate tissue ablation in December 2024 and European MDR CE mark approval in February 2026 (prostate, pancreas, kidney, liver). Active clinical trials include the RELIEF BPH study (Benign Prostatic Hyperplasia) under FDA IDE and the PRESERVE trial (prostate cancer) published in *European Urology* with 2-year follow-up data presented at AUA 2026.

* *BioFlo*: Features Endexo Technology, a proprietary non-eluting polymer blended into polyurethane to resist thrombus accumulation.

* Product Liability, Patent Litigation, and Legal Realities:

* *Defensive Settlement*: A patent settlement with C.R. Bard, Inc. (Becton Dickinson [NYSE: BDX]) regarding implantable port products was settled on March 31, 2024. Following an initial $7.0 million lump-sum paid by March 31, 2025, AngioDynamics, Inc. must pay six minimum annual payments of $2.5 million to BD (commencing in FY25), leaving a total of $9.4 million payable as of May 31, 2026 ($2.5 million short-term, $6.9 million long-term). A December 2025 Federal Circuit ruling affirmed port patent invalidity in favor of AngioDynamics, Inc., negating any variable 6% royalty payments above the $2.5 million minimum.

* *Offensive Litigation*: On April 23, 2026, the company filed an offensive patent infringement lawsuit in Delaware against Endovascular Engineering, Inc., alleging its Hēlo Thrombectomy System violates patents on the proprietary self-expanding funnel design used in AlphaVac and AngioVac.

* *Product Liability MDL*: The company is defending against multidistrict litigation consolidated in the Southern District of California regarding personal injury claims related to its port products. Product liability insurance is capped at $10.0 million per claim and $10.0 million in the annual aggregate, subject to a $500,000 per occurrence self-retention and a $2.0 million aggregate self-insured retention.

* *Strategic Insulation*: The flagship high-margin NanoKnife and Auryon platforms are completely insulated from all ongoing port-related litigation, patent disputes, and BD royalty obligations.

* *Compliance & Macro Hurdles*: The global expansion exposes the firm to FCPA, Stark Law, and Anti-Kickback Statute risks. Geopolitical friction, including conflicts in Europe and the Middle East, along with US-China trade disputes, led to a negative gross margin impact of $3.2 million from tariffs in FY26. Additionally, European Union Medical Device Regulation (MDR) certification delays (typically 12 to 18 months or longer) forced the company to discontinue selective legacy products in the EU.

* Corporate Governance and Executive Transition: James C. Clemmer, President and CEO since April 2016, announced his retirement, effective the earlier of November 30, 2026, or the appointment of a successor. The board has initiated a formal search, and the company incurred $1.63 million in CEO transition and management retention expenses in FY26.

HDIN Institutional Verdict

The financial performance of AngioDynamics, Inc. in FY26 reflects a successful segment re-weighting, but the execution risk remains exceptionally concentrated in the next 12 months.

* High-Margin Med Tech Substitution: The deliberate cannibalization of the low-margin legacy Med Device catheter portfolio (-$0.7 million in older thrombolytic catheters) in favor of the high-margin, clinically differentiated Med Tech segment (63.6% GM vs. 46.7% GM) is fundamentally reshaping the company’s margin scalability. The $10.0 million growth in Auryon and the upcoming Medicare coverage for NanoKnife (effective July 5, 2026) act as high-conviction growth engines.

* Restructuring and CEO Continuity Risk: Transitioning to an asset-light, outsourced global supply chain across Costa Rica, Latvia, Italy, Israel, and China removes New York fixed overhead and targets $15.0 million in annualized savings. However, this pivot increases reliance on third-party Quality System Regulations (QSR) compliance and elevates exposure to bilateral tariff volatility, which already cost the company $3.2 million in FY26. Executing this supply chain migration simultaneously with a CEO succession by November 30, 2026, and unquantified Southern District of California port product liability claims, presents material execution risks.

* Liquidity & Capital Structure Resilience: Despite these headwinds, AngioDynamics, Inc. is entering this transition phase from a position of relative balance sheet strength. A debt-free capital structure, $53.86 million in cash, and the positive $3.09 million operating cash flow inflection—driven by a $10.05 million working capital inventory reduction—provide a solid capital buffer. If the new leadership can successfully execute the supply chain transition and leverage the Palmetto LCD prostate reimbursement pathway, the eventual reversal of the company’s $65.49 million deferred tax asset valuation allowance will deliver a highly material non-cash benefit to future GAAP earnings.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at [http://www.hdinresearch.com](http://www.hdinresearch.com).

2026 AI Transparency Footer

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."