Anti-Reflective Coating for Photoresist Market: Strong Growth Ahead as Semiconductor Industry Scales

The semiconductor industry is undergoing a period of historic transformation. With relentless demand for smaller, faster, and more energy-efficient devices, chipmakers are pushing the limits of photolithography, the core process behind integrated circuit manufacturing. Among the supporting materials that make this possible, anti-reflective coatings (ARC) for photoresist have emerged as a crucial enabler of precision, yield, and scalability.

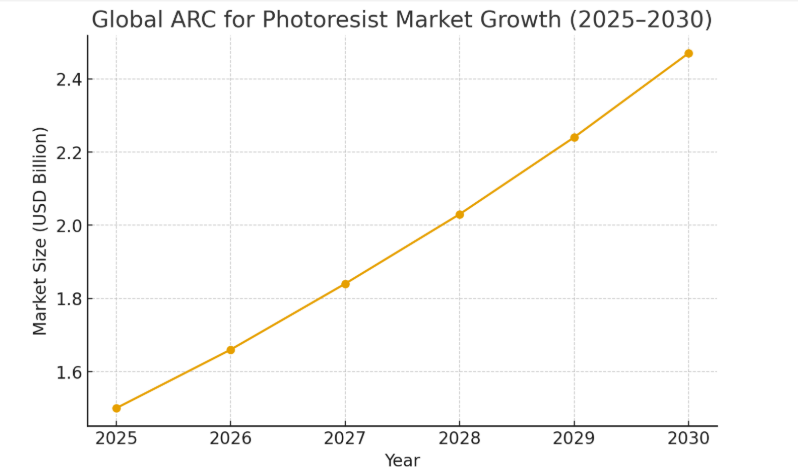

Industry forecasts suggest that the global market for ARCs will reach approximately USD 1.5 billion by 2025, growing at a compound annual growth rate (CAGR) of 10.5% through 2030. This growth trajectory is underpinned by the expansion of 5G networks, artificial intelligence (AI), advanced computing, and next-generation consumer electronics, all of which require cutting-edge semiconductor nodes. As IC geometries shrink and the number of lithographic layers increases, the role of ARC materials in ensuring accurate pattern transfer and minimizing defects has never been more important.

What Are Anti-Reflective Coatings for Photoresist?

Anti-reflective coatings are thin polymeric films applied during photolithography to suppress light reflections at critical interfaces. Without these coatings, incident light can reflect between the resist and substrate or between the resist and air, producing standing wave effects and line width variations that compromise chip performance.

ARCs mitigate these issues through two mechanisms:

By attenuating the light that passes through the coating layer.

By matching the refractive index of the coating with the photoresist at the exposure wavelength.

Depending on placement, ARCs are categorized into:

-

Bottom Anti-Reflective Coatings (BARC): Applied between the substrate and photoresist, BARC dominates the market with more than 75% share. BARC layers not only control reflectivity but also improve etch selectivity and profile control.

-

Top Anti-Reflective Coatings (TARC): Coated above the photoresist, TARC helps minimize reflections at the resist–air interface. Though smaller in scale than BARC, TARC remains important for specific applications.

-

EUV multilayer coatings: Emerging materials designed to support extreme ultraviolet (EUV) lithography at advanced nodes below 7 nm. These represent the fastest-growing ARC segment.

The application processes differ slightly. In BARC processes, wafers are first coated with BARC, cured, and then overlaid with photoresist for subsequent lithographic steps. In TARC processes, the photoresist is coated and cured first, followed by a thin TARC layer before exposure.

Market Drivers: Why Demand Is Rising

Several structural factors are fueling ARC adoption worldwide:

Shrinking Technology Nodes: As semiconductor geometries scale from 28 nm to 7 nm, 5 nm, and beyond, the margin for error in photolithography becomes vanishingly small. ARCs are indispensable in providing the line width control and process window optimization required at these scales.

Layer Proliferation: Modern logic and memory devices require dozens of lithography layers. Each additional layer increases the need for ARC materials to maintain pattern fidelity across the stack.

Rise of 12-Inch Fabs: New wafer fabrication capacity, especially in Asia, is expanding the market for advanced lithography materials. China, Taiwan, and South Korea remain the engines of capacity growth, with the U.S. and Europe investing to regain ground.

Next-Generation Applications: The rapid spread of 5G, AI chips, automotive semiconductors, and Internet of Things (IoT) devices is accelerating demand for high-performance semiconductors, and by extension, for ARC materials.

EUV Transition: Extreme ultraviolet lithography is gaining adoption at leading-edge nodes. EUV-compatible ARC materials, particularly multi-layer underlayers, represent the most dynamic growth opportunity.

Opportunities and Challenges

Despite strong growth potential, the ARC market faces both opportunities and challenges:

Opportunities

Localization in China: With less than 5% of ARC demand currently met by domestic suppliers, the Chinese market represents a vast opportunity for local producers to scale up and capture share.

Material Innovation: Advanced ARCs that integrate simulation software (e.g., Brewer Science’s OptiStack®) or combine hard-mask and etch resistance properties will be critical for EUV adoption.

Partnership Models: Collaborations between Western technology leaders and Asian manufacturing partners, such as Brewer Science’s partnership with Nissan Chemical, will remain a template for future expansion.

Challenges

High R&D Costs: Formulating ARCs to meet the demands of shrinking nodes requires constant innovation, extensive testing, and close alignment with photoresist development.

Stringent Qualification Processes: Customers in the semiconductor sector impose lengthy and costly qualification steps, limiting the speed of market entry for new suppliers.

Supply Chain Vulnerabilities: Disruptions in global supply chains highlight the risks of over-reliance on a few producers. Diversification and localized production will be critical to ensuring continuity.

Integration Complexity: Chemical interactions between resists, ARCs, and substrates are becoming more pronounced, requiring constant fine-tuning of materials and processes.

Competitive Landscape

The ARC market is highly concentrated, dominated by five global leaders:

Tokyo Ohka Kogyo (TOK): A Japanese pioneer in photoresist and ARC technologies, closely integrated with leading-edge lithography processes.

DuPont: A diversified chemicals and materials company with a strong semiconductor materials division.

Merck KGaA: Through its Performance Materials business, Merck is a major supplier of advanced semiconductor chemicals.

JSR Corporation: Another Japanese leader with significant market share in both ARCs and photoresists.

Brewer Science: A U.S.-based specialist, known for its ARC® and OptiStack® technologies, with strong collaborative ties to Nissan Chemical.

Brewer Science and Nissan Chemical have extended their joint agreement through 2028, ensuring continuity of ARC and OptiStack® products for Asian customers. This collaboration combines Brewer’s technology leadership with Nissan’s manufacturing capacity, guaranteeing uninterrupted supply and technical support in the region.

In China, Xiamen Hengkun New Materials Technology Co. Ltd. is the largest domestic producer, with capacity exceeding 20,000 gallons annually. However, actual production and sales remain at around 4,000 gallons, reflecting the early stage of market development. Domestic ARC penetration remains below 5%, highlighting significant headroom for import substitution as China ramps up semiconductor self-sufficiency.

Regional Outlook

Asia-Pacific: The largest and fastest-growing market, driven by wafer fabrication capacity in Taiwan, South Korea, Japan, and increasingly China. Localization efforts in China add further momentum.

North America: Growth supported by U.S. government investments in reshoring semiconductor manufacturing and the expansion of advanced fabs by Intel, TSMC, and Samsung in the U.S.

Europe: Though smaller in scale, Europe’s semiconductor ecosystem is bolstered by ASML’s leadership in lithography tools and EU initiatives to strengthen chip supply chains.

Future Outlook: EUV and Beyond

Looking ahead, EUV lithography represents the most significant frontier for ARC development. With critical dimensions shrinking below 7 nm, multi-layer underlayers and hard-mask solutions will be essential. EUV-compatible ARC materials must deliver low defectivity, high etch resistance, and compatibility with new photoresist chemistries.

Meanwhile, sustainability will emerge as an increasingly important factor. Environmental regulations are pressuring the industry to reduce solvent use and develop greener chemistries without compromising performance. Suppliers investing in sustainable innovation may secure a long-term competitive advantage.