Global Direct-Reduced Iron (DRI) Market Steadily Expands with Low-Carbon Push

Global Direct-Reduced Iron Market Steadily Expands with Low-Carbon Push

The global direct-reduced iron (DRI) market is entering a new phase of growth as steelmakers seek low-carbon alternatives to blast furnace production. Recent developments underscore this trend: on September 1, 2025, India’s Lloyds Metals commissioned a 360,000-ton sponge iron facility at Ghugus, lifting its total capacity to 700,000 tons.

Market Size and Growth

The global DRI market is projected to reach USD 14.6 billion by 2025, translating into around 132 million tons of production. With a compound annual growth rate (CAGR) of 2.5% through 2030, the industry is expanding steadily, driven by high-purity steelmaking demand and environmental regulations that favor low-carbon feedstocks.

Technology Overview

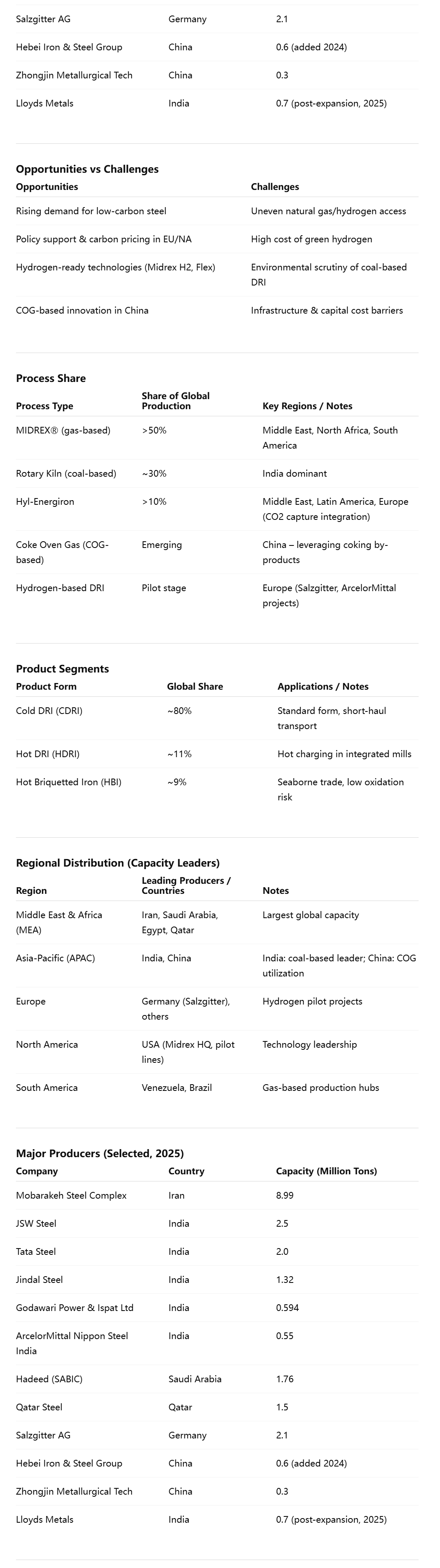

DRI is produced via solid-state reduction of iron ore using gas or coal. Gas-based technologies dominate in natural gas–rich regions such as the Middle East, North Africa, and South America, while coal-based rotary kilns remain entrenched in India.

Midrex Technologies leads with more than 50% global market share through its MIDREX® Process, including hydrogen-ready variants. Hyl-Energiron, developed by Tenova and Danieli, commands over 10%, featuring integrated CO2 capture. Rotary kiln processes account for about 30% of output, heavily concentrated in India.

Coke oven gas (COG)–based DRI, emerging in China, leverages coking by-products with 55–60% hydrogen content, improving both efficiency and environmental performance. Full-scale hydrogen-based DRI remains constrained by high costs and infrastructure limitations, though demonstration projects in Europe are advancing.

Product Segments

DRI is traded in three main forms:

– Cold DRI (CDRI), the most common, accounting for 80% of output.

– Hot DRI (HDRI), about 11%, used in integrated mills for hot charging.

– Hot briquetted iron (HBI), roughly 9%, favored for long-distance shipping.

Regional Dynamics and Producers

India, Iran, Russia, Saudi Arabia, and Egypt are the top five producing nations. The Middle East and Africa hold the largest installed capacity, followed by Asia-Pacific, North America, Europe, and South America.

In India, leading producers include JSW Steel (2.5 million tons), Tata Steel (2.0 million tons), Jindal Steel (1.32 million tons), and Godawari Power & Ispat Ltd (0.594 million tons). ArcelorMittal Nippon Steel India operates 550,000 tons.

Iran’s Mobarakeh Steel Complex leads globally with 8.99 million tons, alongside Khouzestan Steel (2.0 million tons). In the Middle East, Hadeed (1.76 million tons) and Qatar Steel (1.5 million tons) anchor capacity. Europe’s Salzgitter AG has commissioned a 2.1 million-ton hydrogen-ready facility, while in China, Hebei Iron & Steel Group added 600,000 tons in 2024.

Opportunities and Challenges

The industry faces a dual imperative: scaling up production while reducing emissions. Gas-based and hydrogen-ready technologies are well positioned for growth, supported by decarbonization policies and carbon pricing mechanisms in Europe and North America.

Challenges include high capital costs, uneven access to natural gas and hydrogen, and the environmental impact of coal-based DRI. Green hydrogen, though promising, remains commercially uncompetitive at present.

Outlook

In the near term, the Middle East and Africa will continue to dominate gas-based production, while India maintains leadership in coal-based output. Europe is driving hydrogen-based DRI pilots, and China is scaling up coke oven gas utilization.

Long-term market evolution will depend on the cost curve of green hydrogen. As costs decline, potentially by the early 2030s, hydrogen-based DRI could reshape the industry. Until then, incremental adoption of gas-based and hybrid solutions will characterize growth.

With steady demand, supportive policy frameworks, and technological innovation, DRI is emerging as a cornerstone of the global steel industry’s transition toward a low-carbon future.