Surgical Stapler Market Valued at 10-12 Billion USD in 2025 as Intelligent Devices and Centralized Procurement Reshape the Landscape

Date : 2025-12-26

Reading : 470

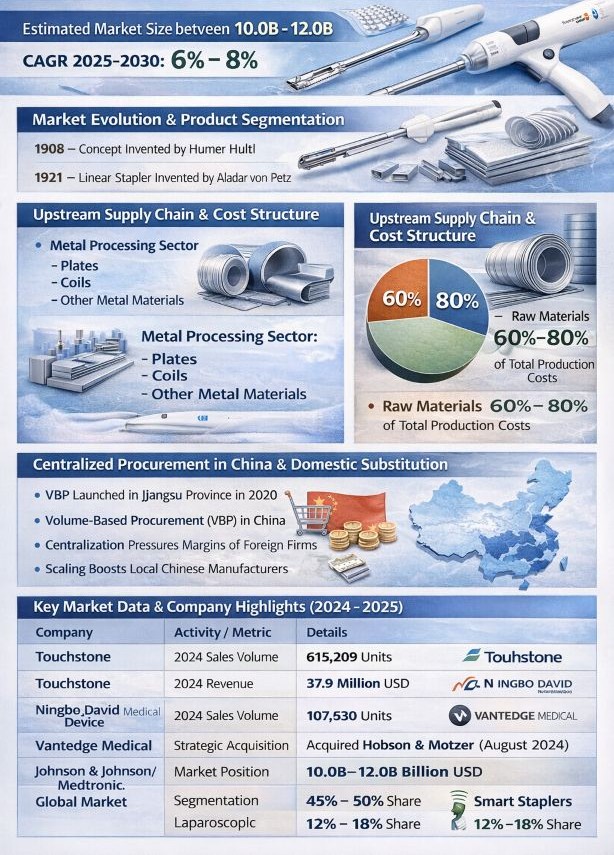

HDIN Research, a premier market intelligence provider, has announced the release of its 2025 Global Surgical Stapler Market Report. The study estimates the current market size between 10.0 and 12.0 billion USD. Driven by technological advancements in minimally invasive surgery and aging global populations, the market is projected to expand at a Compound Annual Growth Rate (CAGR) of 6% to 8% from 2025 through 2030.

Market Evolution and Product Segmentation

Surgical staplers, which utilize titanium staples to connect or remove tissues, have become the standard alternative to manual suturing since their conceptual inception by Hungarian physician Humer Hultl in 1908 and the subsequent linear stapler invention by Aladar Von Petz in 1921. Today, the market is segmented by surgical application and technology level. Laparoscopic staplers currently dominate the sector, accounting for 45% to 50% of the market share, reflecting the global shift toward minimally invasive procedures. Open surgery staplers retain a 35% to 40% share, while intelligent or smart staplers represent the fastest-growing segment, capturing 12% to 18% of the market.

Upstream Supply Chain and Cost Structure

The industry is heavily dependent on the metal processing sector. Upstream components primarily consist of plates, coils, and other metal materials. Raw materials represent a significant portion of the cost structure, accounting for 60% to 80% of total production costs. This high sensitivity to raw material prices places pressure on manufacturers to optimize supply chains and manufacturing efficiency.

Impact of Centralized Procurement and Domestic Substitution in China

A major structural shift is occurring in the Chinese market, a key growth region. Following the initial volume-based procurement (VBP) pilot in Jiangsu province in November 2020, centralized purchasing has become a standard policy tool. This policy has compressed profit margins across the board. Multinational corporations, which traditionally operate with higher cost structures, face intensified challenges in this low-margin environment. Consequently, this has accelerated the trend of domestic substitution, where local Chinese manufacturers are gaining market share from global giants.

While multinational leaders like Johnson & Johnson and Medtronic continue to hold the majority of the global market share, the VBP policy is forcing consolidation among Chinese manufacturers. The market is moving away from fragmentation, as the rigorous demands of centralized procurement favor local enterprises with strong technical innovation capabilities and economies of scale.

Company Developments and Market Data

The competitive landscape is active with both organic growth and strategic acquisitions. In a notable move to strengthen its manufacturing capabilities, Vantedge Medical acquired Hobson & Motzer in August 2024. Meanwhile, operational data from 2024 highlights the scale of key emerging players. Touchstone reported a sales volume of 615,209 units with revenues hitting 37.9 million USD, while Ningbo David Medical Device recorded sales of 107,630 units.

Summary

About HDIN Research

HDIN Research is a leading independent market research and consulting firm focused on the medical device and healthcare industries. We provide data-driven insights to help companies navigate complex regulatory environments and competitive landscapes.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

Market Evolution and Product Segmentation

Surgical staplers, which utilize titanium staples to connect or remove tissues, have become the standard alternative to manual suturing since their conceptual inception by Hungarian physician Humer Hultl in 1908 and the subsequent linear stapler invention by Aladar Von Petz in 1921. Today, the market is segmented by surgical application and technology level. Laparoscopic staplers currently dominate the sector, accounting for 45% to 50% of the market share, reflecting the global shift toward minimally invasive procedures. Open surgery staplers retain a 35% to 40% share, while intelligent or smart staplers represent the fastest-growing segment, capturing 12% to 18% of the market.

Upstream Supply Chain and Cost Structure

The industry is heavily dependent on the metal processing sector. Upstream components primarily consist of plates, coils, and other metal materials. Raw materials represent a significant portion of the cost structure, accounting for 60% to 80% of total production costs. This high sensitivity to raw material prices places pressure on manufacturers to optimize supply chains and manufacturing efficiency.

Impact of Centralized Procurement and Domestic Substitution in China

A major structural shift is occurring in the Chinese market, a key growth region. Following the initial volume-based procurement (VBP) pilot in Jiangsu province in November 2020, centralized purchasing has become a standard policy tool. This policy has compressed profit margins across the board. Multinational corporations, which traditionally operate with higher cost structures, face intensified challenges in this low-margin environment. Consequently, this has accelerated the trend of domestic substitution, where local Chinese manufacturers are gaining market share from global giants.

While multinational leaders like Johnson & Johnson and Medtronic continue to hold the majority of the global market share, the VBP policy is forcing consolidation among Chinese manufacturers. The market is moving away from fragmentation, as the rigorous demands of centralized procurement favor local enterprises with strong technical innovation capabilities and economies of scale.

Company Developments and Market Data

The competitive landscape is active with both organic growth and strategic acquisitions. In a notable move to strengthen its manufacturing capabilities, Vantedge Medical acquired Hobson & Motzer in August 2024. Meanwhile, operational data from 2024 highlights the scale of key emerging players. Touchstone reported a sales volume of 615,209 units with revenues hitting 37.9 million USD, while Ningbo David Medical Device recorded sales of 107,630 units.

Summary

About HDIN Research

HDIN Research is a leading independent market research and consulting firm focused on the medical device and healthcare industries. We provide data-driven insights to help companies navigate complex regulatory environments and competitive landscapes.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com