Tin Market Report 2025: Electronics and EV Sectors Drive Demand Toward $21 Billion Valuation by 2030

Date : 2025-12-30

Reading : 1000

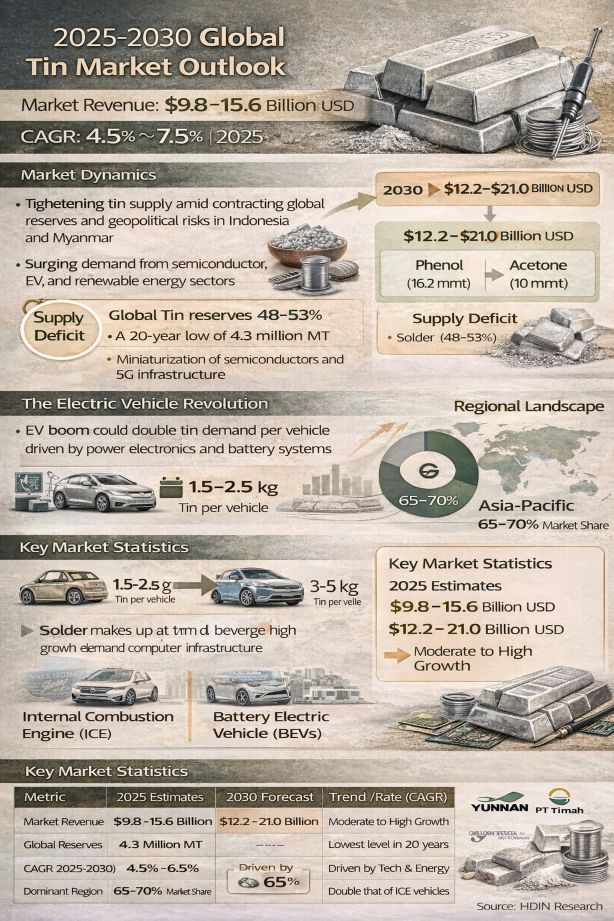

HDIN Research has released its latest comprehensive study titled "Tin (Sn) Global Market Insights 2025." The report provides an in-depth analysis of the global tin industry, highlighting a critical divergence between tightening raw material supplies and accelerating demand from the semiconductor, electric vehicle (EV), and renewable energy sectors. As of the base year 2025, the global market is valued between 9.8 billion USD and 15.6 billion USD.

Market Overview and Growth Dynamics

According to the report, the global tin market is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.5% to 6.5% through 2030, potentially reaching a valuation of 21.0 billion USD. This growth is underpinned by the metal's indispensable role in modern technology. Tin solder, which accounts for approximately 48-53% of total consumption, is seeing surged demand due to the miniaturization of semiconductors and the deployment of 5G infrastructure.

The analysis highlights a structural supply deficit. Global tin reserves have contracted to 4.3 million metric tons in 2023, the lowest level in two decades. Declining ore grades in major producing regions, particularly in Myanmar and China, coupled with geopolitical supply disruptions in Indonesia, are creating a structurally tight market environment.

The Electric Vehicle Revolution

A key finding of the HDIN Research report is the impact of automotive electrification on tin consumption. While traditional internal combustion engine vehicles contain approximately 1.5 kg to 2.5 kg of tin, Battery Electric Vehicles (BEVs) require between 3 kg and 5 kg per unit. This increase is driven by the need for extensive soldering in power electronics, battery management systems, and charging infrastructure. The report estimates that the EV revolution could add significant incremental demand by 2030.

Regional and Competitive Landscape

The Asia-Pacific region continues to dominate the global landscape, accounting for 65-70% of global consumption. This is largely driven by China's massive electronics manufacturing ecosystem. China also remains the world's largest producer, though it faces challenges regarding ore grades.

The competitive landscape remains concentrated. Top players such as Yunnan Tin Company, PT Timah, and Minsur S.A. control significant portions of the upstream market. The report notes that integrated producers with control over mining and refining operations are best positioned to navigate the current volatility.

Key Market Statistics Summary

About HDIN Research

HDIN Research is a leading market research firm providing strategic intelligence and detailed analysis across the chemical, material, and energy industries. We help global clients navigate complex market environments with data-driven insights.

Media Contact:

HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

Market Overview and Growth Dynamics

According to the report, the global tin market is projected to expand at a Compound Annual Growth Rate (CAGR) of 4.5% to 6.5% through 2030, potentially reaching a valuation of 21.0 billion USD. This growth is underpinned by the metal's indispensable role in modern technology. Tin solder, which accounts for approximately 48-53% of total consumption, is seeing surged demand due to the miniaturization of semiconductors and the deployment of 5G infrastructure.

The analysis highlights a structural supply deficit. Global tin reserves have contracted to 4.3 million metric tons in 2023, the lowest level in two decades. Declining ore grades in major producing regions, particularly in Myanmar and China, coupled with geopolitical supply disruptions in Indonesia, are creating a structurally tight market environment.

The Electric Vehicle Revolution

A key finding of the HDIN Research report is the impact of automotive electrification on tin consumption. While traditional internal combustion engine vehicles contain approximately 1.5 kg to 2.5 kg of tin, Battery Electric Vehicles (BEVs) require between 3 kg and 5 kg per unit. This increase is driven by the need for extensive soldering in power electronics, battery management systems, and charging infrastructure. The report estimates that the EV revolution could add significant incremental demand by 2030.

Regional and Competitive Landscape

The Asia-Pacific region continues to dominate the global landscape, accounting for 65-70% of global consumption. This is largely driven by China's massive electronics manufacturing ecosystem. China also remains the world's largest producer, though it faces challenges regarding ore grades.

The competitive landscape remains concentrated. Top players such as Yunnan Tin Company, PT Timah, and Minsur S.A. control significant portions of the upstream market. The report notes that integrated producers with control over mining and refining operations are best positioned to navigate the current volatility.

Key Market Statistics Summary

About HDIN Research

HDIN Research is a leading market research firm providing strategic intelligence and detailed analysis across the chemical, material, and energy industries. We help global clients navigate complex market environments with data-driven insights.

Media Contact:

HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com