Phenol-Acetone Industry Chain Report 2026: Supply Surge in Asia Transforms Downstream Markets

Date : 2026-01-02

Reading : 1482

HDIN Research, a leading market research firm, has released its latest comprehensive analysis of the global Phenol-Acetone value chain. The report highlights a significant shift in global supply dynamics, driven primarily by aggressive capacity expansions in China across the entire value chain—from upstream Phenol and Acetone to downstream derivatives such as Bisphenol A (BPA), Polycarbonate (PC), and Methyl Methacrylate (MMA).

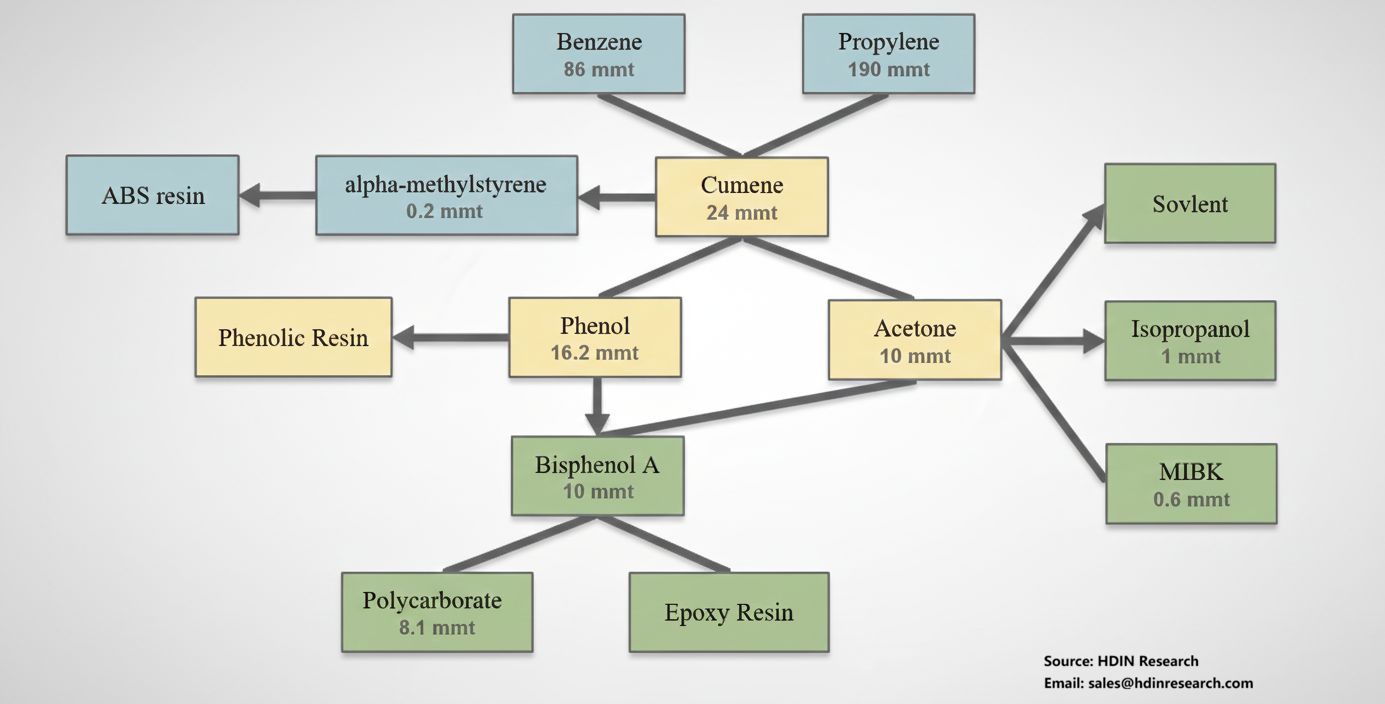

Figure Phenol-Acetone Industry Chain Structure (Upstream–Midstream–Downstream)

Note: the number is production capacity data and mmt is million metric tons

Upstream Supply and Phenol-Acetone Market Overview

The global supply of primary raw materials, Pure Benzene and Propylene, remains robust, with global capacities standing at approximately 86 million tons and 190 million tons, respectively. These materials are synthesized into the intermediate Cumene, which is then processed into Phenol and Acetone.

According to HDIN Research data, global Phenol capacity has reached approximately 16.2 million tons. The Asia-Pacific region dominates both production and consumption, with China solidifying its position as the world's largest producer following five years of intensive capacity additions, now exceeding 6 million tons. Other key Asian producers include South Korea, Japan, Thailand, Singapore, and Taiwan China. In comparison, Europe holds approximately 2.5 million tons of capacity, while North America holds roughly 2 million tons.

Global Acetone capacity stands at approximately 10 million tons. Similar to Phenol, China leads the global Acetone market with a capacity exceeding 3.6 million tons. Leading global producers for the Phenol-Acetone complex include INEOS Phenol, Moeve, Chang Chun Group, Formosa Chemicals & Fibre Corporation, LG Chem, Zhejiang Petroleum & Chemical Co Ltd (ZPC), Kumho P&B Chemicals, AdvanSix, Versalis, and PTT Global Chemical.

Bisphenol A and Polycarbonate: The Shift to Chinese Exports

Bisphenol A (BPA), synthesized from Phenol and Acetone, has seen its global capacity reach approximately 9.5 million tons. The market is heavily concentrated in the Asia-Pacific region. China alone accounts for over 5.3 million tons of capacity. Europe and North America follow as the second and third largest production regions, respectively. Major players like Covestro and SABIC continue to dominate the high-end market, with capacities exceeding 1 million tons each, operating extensive production bases across the US, Europe, and Asia.

A pivotal shift has occurred in the Polycarbonate (PC) sector. Global PC capacity is now approximately 8.1 million tons. China's rapid expansion—growing from under 2 million tons in 2020 to nearly 4 million tons by the end of 2025—has transformed the country from a major importer into a net exporter of Polycarbonate. With an additional 1 million tons of capacity planned, HDIN Research warns that overcapacity in the PC sector may intensify. Outside of China, India is emerging as a new hub for capacity investment.

Acetone Derivatives: MMA, PMMA, and IPA

The report also details critical trends in Acetone derivatives. The Acetone Cyanohydrin (ACH) route, primarily used to produce Methyl Methacrylate (MMA), is facing structural changes. While ACH remains the mainstream technology accounting for 60% of capacity, new investments outside China are moving away from this method.

Global MMA capacity stands at around 6 million tons. China, having surpassed 2.7 million tons in capacity, transitioned to a net exporter in 2021. However, the industry faces utilization rates between 50-60% due to rapid expansion. In contrast, Japan has seen capacity reductions, being surpassed by South Korea as the second-largest Asian producer. Roehm remains the world’s largest MMA producer with a capacity of 697,000 tons.

The Polymethyl Methacrylate (PMMA) market, with a global capacity near 2 million tons, mirrors this trend. China possesses over 850,000 tons of capacity as of late 2025. The market is characterized by severe overcapacity in low-to-mid-end products, while Chinese firms are gradually breaking into the high-end segment, potentially leading to future saturation in that tier as well. Röhm leads the global PMMA market, followed by Trinseo and Mitsubishi Chemical.

The Isopropanol (IPA) market, totaling 3 million tons globally, has seen a demand correction following the decline of COVID-19 related hand sanitizer consumption. China remains the largest producer with over 800,000 tons. Notably, over 60% of Chinese IPA production utilizes the Acetone Hydrogenation process, whereas international producers like ExxonMobil and Shell predominantly use the Propylene Hydration process.

Methyl Isobutyl Ketone (MIBK) capacity is approximately 600,000 tons globally. The market experienced volatility following the 2022 closure of LCY Performance Materials' plant, but rapid capacity additions in China—including 130,000 tons in 2024—have pushed the market into oversupply, significantly lowering prices.

HDIN Research advises industry stakeholders to closely monitor the utilization rates in the Asian market and the shifting trade flows caused by China's transition to a net exporter across multiple derivatives.

Please watch the presentation video on YouTube and download the PDF file from the related topics link below.

About HDIN Research

HDIN Research is a premier provider of market intelligence and strategic analysis. We assist global enterprises in navigating complex market landscapes through data-driven insights and rigorous financial assessment.

For more information, please visit www.hdinresearch.com or contact sales@hdinresearch.com.

Figure Phenol-Acetone Industry Chain Structure (Upstream–Midstream–Downstream)

Note: the number is production capacity data and mmt is million metric tons

Upstream Supply and Phenol-Acetone Market Overview

The global supply of primary raw materials, Pure Benzene and Propylene, remains robust, with global capacities standing at approximately 86 million tons and 190 million tons, respectively. These materials are synthesized into the intermediate Cumene, which is then processed into Phenol and Acetone.

According to HDIN Research data, global Phenol capacity has reached approximately 16.2 million tons. The Asia-Pacific region dominates both production and consumption, with China solidifying its position as the world's largest producer following five years of intensive capacity additions, now exceeding 6 million tons. Other key Asian producers include South Korea, Japan, Thailand, Singapore, and Taiwan China. In comparison, Europe holds approximately 2.5 million tons of capacity, while North America holds roughly 2 million tons.

Global Acetone capacity stands at approximately 10 million tons. Similar to Phenol, China leads the global Acetone market with a capacity exceeding 3.6 million tons. Leading global producers for the Phenol-Acetone complex include INEOS Phenol, Moeve, Chang Chun Group, Formosa Chemicals & Fibre Corporation, LG Chem, Zhejiang Petroleum & Chemical Co Ltd (ZPC), Kumho P&B Chemicals, AdvanSix, Versalis, and PTT Global Chemical.

Bisphenol A and Polycarbonate: The Shift to Chinese Exports

Bisphenol A (BPA), synthesized from Phenol and Acetone, has seen its global capacity reach approximately 9.5 million tons. The market is heavily concentrated in the Asia-Pacific region. China alone accounts for over 5.3 million tons of capacity. Europe and North America follow as the second and third largest production regions, respectively. Major players like Covestro and SABIC continue to dominate the high-end market, with capacities exceeding 1 million tons each, operating extensive production bases across the US, Europe, and Asia.

A pivotal shift has occurred in the Polycarbonate (PC) sector. Global PC capacity is now approximately 8.1 million tons. China's rapid expansion—growing from under 2 million tons in 2020 to nearly 4 million tons by the end of 2025—has transformed the country from a major importer into a net exporter of Polycarbonate. With an additional 1 million tons of capacity planned, HDIN Research warns that overcapacity in the PC sector may intensify. Outside of China, India is emerging as a new hub for capacity investment.

Acetone Derivatives: MMA, PMMA, and IPA

The report also details critical trends in Acetone derivatives. The Acetone Cyanohydrin (ACH) route, primarily used to produce Methyl Methacrylate (MMA), is facing structural changes. While ACH remains the mainstream technology accounting for 60% of capacity, new investments outside China are moving away from this method.

Global MMA capacity stands at around 6 million tons. China, having surpassed 2.7 million tons in capacity, transitioned to a net exporter in 2021. However, the industry faces utilization rates between 50-60% due to rapid expansion. In contrast, Japan has seen capacity reductions, being surpassed by South Korea as the second-largest Asian producer. Roehm remains the world’s largest MMA producer with a capacity of 697,000 tons.

The Polymethyl Methacrylate (PMMA) market, with a global capacity near 2 million tons, mirrors this trend. China possesses over 850,000 tons of capacity as of late 2025. The market is characterized by severe overcapacity in low-to-mid-end products, while Chinese firms are gradually breaking into the high-end segment, potentially leading to future saturation in that tier as well. Röhm leads the global PMMA market, followed by Trinseo and Mitsubishi Chemical.

The Isopropanol (IPA) market, totaling 3 million tons globally, has seen a demand correction following the decline of COVID-19 related hand sanitizer consumption. China remains the largest producer with over 800,000 tons. Notably, over 60% of Chinese IPA production utilizes the Acetone Hydrogenation process, whereas international producers like ExxonMobil and Shell predominantly use the Propylene Hydration process.

Methyl Isobutyl Ketone (MIBK) capacity is approximately 600,000 tons globally. The market experienced volatility following the 2022 closure of LCY Performance Materials' plant, but rapid capacity additions in China—including 130,000 tons in 2024—have pushed the market into oversupply, significantly lowering prices.

HDIN Research advises industry stakeholders to closely monitor the utilization rates in the Asian market and the shifting trade flows caused by China's transition to a net exporter across multiple derivatives.

Please watch the presentation video on YouTube and download the PDF file from the related topics link below.

About HDIN Research

HDIN Research is a premier provider of market intelligence and strategic analysis. We assist global enterprises in navigating complex market landscapes through data-driven insights and rigorous financial assessment.

For more information, please visit www.hdinresearch.com or contact sales@hdinresearch.com.