Acetic Acid Industry Chain Analysis

Date : 2026-01-05

Reading : 1794

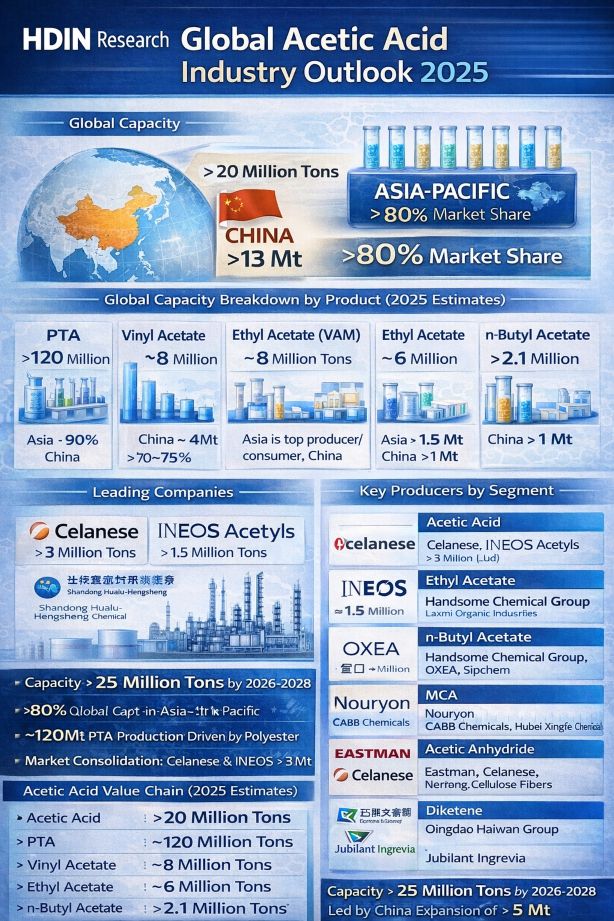

According to the latest monitoring data from HDIN Research, the global acetic acid industry has entered a new phase of capacity expansion. As of 2025, total global acetic acid production capacity has exceeded 20 million tons. The Asia-Pacific region has solidified its position as the world's largest production, consumption, and export hub, accounting for over 80% of total global capacity.

China remains the undisputed leader in the sector, with capacity exceeding 13 million tons in 2025. This represents a significant surge from approximately 9 million tons in 2020, with 2.5 million tons of new capacity added in 2025 alone. While China primarily utilizes coal-based methanol and synthesis gas for production, the rest of the world predominantly relies on natural gas feedstocks.

Market Landscape and Regional Distribution

Behind Asia, North America ranks as the second-largest production region, followed by the Middle East and Africa (MEA) and Europe. Within the Asia-Pacific region, excluding China, significant capacities exist in Japan, South Korea, Malaysia, Singapore, Taiwan (China), and India, totaling between 3 million and 4 million tons.

The market structure continues to evolve with significant consolidation among top players. Celanese remains the largest global manufacturer, followed closely by INEOS Acetyls. Both companies boast nominal capacities exceeding 3 million tons. Shandong Hualu-Hengsheng Chemical Co. Ltd. ranks third globally and first in China, with a capacity of 1.5 million tons.

Figure Key Data of Acetic Acid Industry Chain

Diversified Downstream Applications

The consumption of acetic acid is heavily concentrated in three major derivatives: Purified Terephthalic Acid (PTA), Vinyl Acetate, and Ethyl Acetate, which together account for 55% to 60% of total demand. PTA, primarily used in polyester production (fiber, bottle chips, and films), sees massive scale in Asia. Vinyl Acetate is crucial for producing PVA, EVA, and PVB.

The remaining demand is driven by Butyl Acetate, Monochloroacetic Acid (MCA), Acetic Anhydride, and Diketene, collectively representing 20% to 30% of consumption.

Ethyl Acetate and Butyl Acetate serve as vital solvents in paints, coatings, adhesives, and packaging. Notably, the bio-based Ethyl Acetate market is gaining traction due to green chemistry trends. Major players like Jubilant Ingrevia Limited and Godavari Biorefineries Limited are leading this niche, while Solvay is also active. Viridis Chemical LLC has postponed its bio-based facility launch to 2026.

High-Barrier Segments: Cellulose Acetate

The production of Cellulose Acetate Flake involves high technical barriers, resulting in a concentrated market dominated by four global giants: Eastman, Celanese, Daicel, and Cerdia. These companies typically operate facilities in Europe, North America, and Japan. In China, Nantong Cellulose Fibers Co. Ltd. leads local production. Cellulose Diacetate Flake accounts for over 80% of total flake capacity, mainly used for cigarette filters (tow), while Cellulose Triacetate is critical for LCD optical films.

Please watch the presentation video on YouTube and download the PDF file from the related topics link below.

Future Outlook: 2026-2028

Despite pricing pressures observed since 2022 due to sluggish market demand, investment in the sector remains robust. HDIN Research identifies over 5 million tons of acetic acid capacity currently under construction, primarily located in China. These projects are scheduled to come online between 2026 and 2028. Upon completion, global acetic acid capacity is projected to surpass 25 million tons, further intensifying market competition and solidifying China's pivotal role in the global supply chain.

About HDIN Research

HDIN Research is a leading market research and consulting firm, providing deep insights into chemical, energy, and material industries. We help clients navigate complex market dynamics through precise data and expert analysis.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

China remains the undisputed leader in the sector, with capacity exceeding 13 million tons in 2025. This represents a significant surge from approximately 9 million tons in 2020, with 2.5 million tons of new capacity added in 2025 alone. While China primarily utilizes coal-based methanol and synthesis gas for production, the rest of the world predominantly relies on natural gas feedstocks.

Market Landscape and Regional Distribution

Behind Asia, North America ranks as the second-largest production region, followed by the Middle East and Africa (MEA) and Europe. Within the Asia-Pacific region, excluding China, significant capacities exist in Japan, South Korea, Malaysia, Singapore, Taiwan (China), and India, totaling between 3 million and 4 million tons.

The market structure continues to evolve with significant consolidation among top players. Celanese remains the largest global manufacturer, followed closely by INEOS Acetyls. Both companies boast nominal capacities exceeding 3 million tons. Shandong Hualu-Hengsheng Chemical Co. Ltd. ranks third globally and first in China, with a capacity of 1.5 million tons.

Figure Key Data of Acetic Acid Industry Chain

Diversified Downstream Applications

The consumption of acetic acid is heavily concentrated in three major derivatives: Purified Terephthalic Acid (PTA), Vinyl Acetate, and Ethyl Acetate, which together account for 55% to 60% of total demand. PTA, primarily used in polyester production (fiber, bottle chips, and films), sees massive scale in Asia. Vinyl Acetate is crucial for producing PVA, EVA, and PVB.

The remaining demand is driven by Butyl Acetate, Monochloroacetic Acid (MCA), Acetic Anhydride, and Diketene, collectively representing 20% to 30% of consumption.

Ethyl Acetate and Butyl Acetate serve as vital solvents in paints, coatings, adhesives, and packaging. Notably, the bio-based Ethyl Acetate market is gaining traction due to green chemistry trends. Major players like Jubilant Ingrevia Limited and Godavari Biorefineries Limited are leading this niche, while Solvay is also active. Viridis Chemical LLC has postponed its bio-based facility launch to 2026.

High-Barrier Segments: Cellulose Acetate

The production of Cellulose Acetate Flake involves high technical barriers, resulting in a concentrated market dominated by four global giants: Eastman, Celanese, Daicel, and Cerdia. These companies typically operate facilities in Europe, North America, and Japan. In China, Nantong Cellulose Fibers Co. Ltd. leads local production. Cellulose Diacetate Flake accounts for over 80% of total flake capacity, mainly used for cigarette filters (tow), while Cellulose Triacetate is critical for LCD optical films.

Please watch the presentation video on YouTube and download the PDF file from the related topics link below.

Future Outlook: 2026-2028

Despite pricing pressures observed since 2022 due to sluggish market demand, investment in the sector remains robust. HDIN Research identifies over 5 million tons of acetic acid capacity currently under construction, primarily located in China. These projects are scheduled to come online between 2026 and 2028. Upon completion, global acetic acid capacity is projected to surpass 25 million tons, further intensifying market competition and solidifying China's pivotal role in the global supply chain.

About HDIN Research

HDIN Research is a leading market research and consulting firm, providing deep insights into chemical, energy, and material industries. We help clients navigate complex market dynamics through precise data and expert analysis.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com