Acetic Acid Market Faces Structural Shift - Acetic Acid & Derivatives Industry Chain Series Report (1)

Date : 2026-01-19

Reading : 539

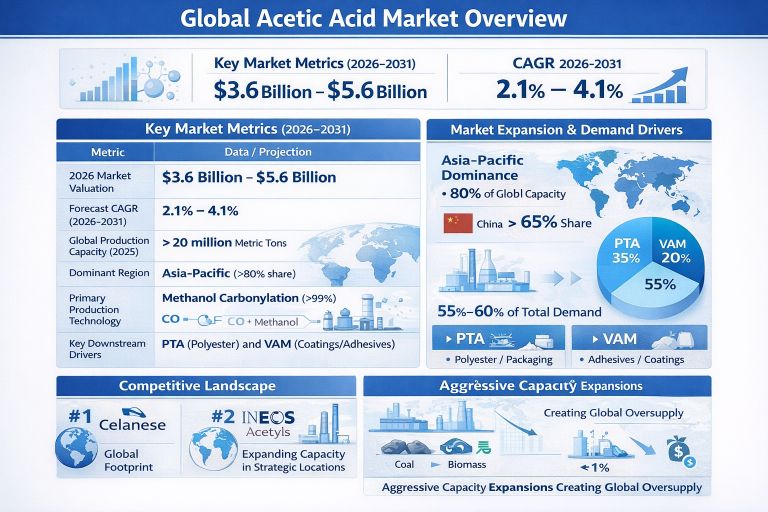

The global acetic acid market is navigating a period of significant transformation characterized by aggressive capacity expansions and shifting trade dynamics. According to the latest industry analysis released by HDIN Research, the global acetic acid market is valued at approximately $3.6 to $5.6 billion in 2026. The market is projected to expand at a Compound Annual Growth Rate (CAGR) of 2.1% to 4.1% through 2031, driven by industrialization in emerging economies despite persistent headwinds from global oversupply.

A Decade of Capacity Expansion

The defining characteristic of the current market landscape is the rapid expansion of production capabilities, particularly within the Asia-Pacific region. HDIN Research data indicates that Asia-Pacific now accounts for over 80% of global production capacity. China alone represents more than 65% of the worldwide total, having expanded its domestic capacity from approximately 9 million metric tons in 2020 to over 13 million metric tons by 2025.

This structural shift has been fueled by massive projects from major players such as Shanghai Huayi Group and Hebei Kingboard, utilizing coal-to-methanol feedstock routes to establish cost-competitive production bases.

Figure Key Market Data of Acetic Acid

Application Trends and Demand Drivers

Demand for acetic acid remains heavily concentrated in two primary derivative chains: Purified Terephthalic Acid (PTA) and Vinyl Acetate Monomer (VAM). Together, these applications account for 55% to 60% of total global consumption.

The PTA segment links the acetic acid market directly to the global textile and packaging industries, heavily influenced by polyester fiber production growth in China and India. Meanwhile, the VAM segment serves the construction and automotive sectors through adhesives, paints, and coatings. Emerging applications in specialty chemicals, while smaller in volume, continue to offer diversification opportunities.

Competitive Landscape and Future Developments

The competitive environment has evolved into a mix of global multinational corporations and large-scale regional producers. Celanese Corporation remains the world's largest producer, maintaining a strategic global footprint. INEOS Acetyls follows as the second-largest player, continuing its expansion strategy through recent acquisitions and joint ventures, including a notable agreement with Gujarat Narmada Valley Fertilizers & Chemicals to establish a new plant in India by 2028.

However, the market faces challenges. The aggressive capacity additions since 2020 have created oversupply conditions, exerting downward pressure on prices and producer margins. Furthermore, the report notes that bio-based acetic acid alternatives currently struggle to compete economically against fossil-based routes, remaining a niche segment with less than 1% global share.

HDIN Research concludes that while near-term pricing remains challenged by overcapacity, the long-term outlook is supported by robust industrial demand in developing markets and the potential for industry consolidation.

For more detailed analysis, capacity data, and regional forecasts, please visit the HDIN Research website.

About HDIN Research

HDIN Research is a trusted provider of detailed market intelligence and strategic analysis for the global petrochemical and energy industries.

Contact:

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

A Decade of Capacity Expansion

The defining characteristic of the current market landscape is the rapid expansion of production capabilities, particularly within the Asia-Pacific region. HDIN Research data indicates that Asia-Pacific now accounts for over 80% of global production capacity. China alone represents more than 65% of the worldwide total, having expanded its domestic capacity from approximately 9 million metric tons in 2020 to over 13 million metric tons by 2025.

This structural shift has been fueled by massive projects from major players such as Shanghai Huayi Group and Hebei Kingboard, utilizing coal-to-methanol feedstock routes to establish cost-competitive production bases.

Figure Key Market Data of Acetic Acid

Application Trends and Demand Drivers

Demand for acetic acid remains heavily concentrated in two primary derivative chains: Purified Terephthalic Acid (PTA) and Vinyl Acetate Monomer (VAM). Together, these applications account for 55% to 60% of total global consumption.

The PTA segment links the acetic acid market directly to the global textile and packaging industries, heavily influenced by polyester fiber production growth in China and India. Meanwhile, the VAM segment serves the construction and automotive sectors through adhesives, paints, and coatings. Emerging applications in specialty chemicals, while smaller in volume, continue to offer diversification opportunities.

Competitive Landscape and Future Developments

The competitive environment has evolved into a mix of global multinational corporations and large-scale regional producers. Celanese Corporation remains the world's largest producer, maintaining a strategic global footprint. INEOS Acetyls follows as the second-largest player, continuing its expansion strategy through recent acquisitions and joint ventures, including a notable agreement with Gujarat Narmada Valley Fertilizers & Chemicals to establish a new plant in India by 2028.

However, the market faces challenges. The aggressive capacity additions since 2020 have created oversupply conditions, exerting downward pressure on prices and producer margins. Furthermore, the report notes that bio-based acetic acid alternatives currently struggle to compete economically against fossil-based routes, remaining a niche segment with less than 1% global share.

HDIN Research concludes that while near-term pricing remains challenged by overcapacity, the long-term outlook is supported by robust industrial demand in developing markets and the potential for industry consolidation.

For more detailed analysis, capacity data, and regional forecasts, please visit the HDIN Research website.

About HDIN Research

HDIN Research is a trusted provider of detailed market intelligence and strategic analysis for the global petrochemical and energy industries.

Contact:

Website: www.hdinresearch.com

Email: sales@hdinresearch.com