AI Computing Market Report: Financial Penetration Analysis Reveals Structural Divide Between International Giants and Emerging Domestic Vendors

Date : 2026-01-16

Reading : 750

HDIN Research, a leading independent market consulting firm, today announced the release of its comprehensive analysis report titled "Global AI Computing Power Industry Pattern and Financial Penetration Analysis." Utilizing the Harvard Financial Analytical Framework, the report offers a deep dive into the strategic and financial positions of industry leaders NVIDIA and AMD, alongside Chinese challengers such as Moore Threads, Biren Technology, Cambricon, and MetaX.

The report identifies that the current AI computing market is driven by a structural cycle where model complexity and computing demand reshape the underlying architecture approximately every two years. This cycle has created a distinct market characteristic: high-end concentration in the training sector and low-end differentiation in the inference sector.

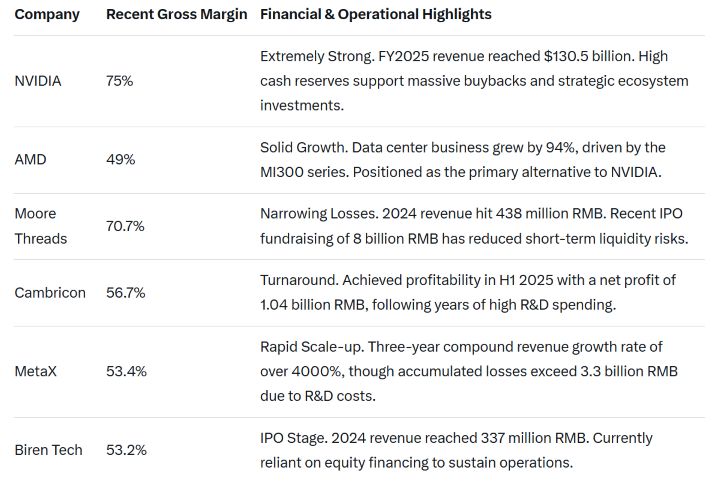

Financial Divergence: The Profitability Gap

The analysis highlights a stark contrast in financial health and capital efficiency between established global giants and emerging Chinese vendors. While international leaders benefit from massive economies of scale, Chinese firms are characterized by high R&D intensity and long return cycles.

HDIN Research has summarized the key financial and operational metrics for the 2024-2025 period in the following table:

Accounting Analysis: High R&D Intensity vs. Inventory Risks

The report sheds light on the accounting nuances of the sector. Chinese vendors exhibit exceptionally high R&D-to-revenue ratios, with Cambricon allocating 91.30% of revenue to R&D in 2024, and Moore Threads reaching extreme ratios during its early expansion. This high-intensity expenditure reflects the industry's heavy investment nature.

Conversely, international giants face inventory risks tied to geopolitical shifts. NVIDIA recorded a $4.5 billion inventory provision in fiscal 2025 due to export policy changes affecting its H20 products. Similarly, AMD recorded approximately $800 million in inventory charges related to export controls on its MI308 data center GPUs.

Strategic Analysis: The "1/8th" Performance Reality

While domestic Chinese vendors have made significant strides in establishing a "Sovereign AI" foundation, the report emphasizes a realistic view of the technological gap. HDIN Research analysts concur with industry deep-dive data suggesting that the FP16 computing power of the Huawei Ascend 910B is approximately one-eighth that of NVIDIA's H200. Furthermore, significant disparities remain in HBM memory capacity and bandwidth, which are critical for training large-scale models.

NVIDIA continues to defend its moat through a "CUDA Everywhere" strategy and an aggressive one-year architecture update cycle (Blackwell to Rubin). AMD is countering by targeting the "Memory Wall" challenge with larger memory capacities, such as the MI355X equipped with 288GB HBM3e.

Future Outlook: From Brute Force to Market Forking

Looking ahead, HDIN Research predicts a bifurcation in the market. The training sector will likely remain concentrated around top-tier GPUs like Blackwell. However, the inference market is expected to fragment as cost and efficiency drive the adoption of custom ASICs (such as TPUs) and high-performance Ethernet standards. By 2028, ASICs are projected to capture approximately 45% of the inference market share.

For Chinese vendors, the path forward involves leveraging local advantages in "AI Sovereignty" and focusing on system-level interconnect technologies to mitigate single-chip performance deficits. While the road remains challenging due to the hard computing power gap, opportunities exist in localized services and specific vertical applications.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. HDIN Research helps clients navigate complex industrial landscapes through rigorous data analysis and strategic insights.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com

The report identifies that the current AI computing market is driven by a structural cycle where model complexity and computing demand reshape the underlying architecture approximately every two years. This cycle has created a distinct market characteristic: high-end concentration in the training sector and low-end differentiation in the inference sector.

Financial Divergence: The Profitability Gap

The analysis highlights a stark contrast in financial health and capital efficiency between established global giants and emerging Chinese vendors. While international leaders benefit from massive economies of scale, Chinese firms are characterized by high R&D intensity and long return cycles.

HDIN Research has summarized the key financial and operational metrics for the 2024-2025 period in the following table:

Accounting Analysis: High R&D Intensity vs. Inventory Risks

The report sheds light on the accounting nuances of the sector. Chinese vendors exhibit exceptionally high R&D-to-revenue ratios, with Cambricon allocating 91.30% of revenue to R&D in 2024, and Moore Threads reaching extreme ratios during its early expansion. This high-intensity expenditure reflects the industry's heavy investment nature.

Conversely, international giants face inventory risks tied to geopolitical shifts. NVIDIA recorded a $4.5 billion inventory provision in fiscal 2025 due to export policy changes affecting its H20 products. Similarly, AMD recorded approximately $800 million in inventory charges related to export controls on its MI308 data center GPUs.

Strategic Analysis: The "1/8th" Performance Reality

While domestic Chinese vendors have made significant strides in establishing a "Sovereign AI" foundation, the report emphasizes a realistic view of the technological gap. HDIN Research analysts concur with industry deep-dive data suggesting that the FP16 computing power of the Huawei Ascend 910B is approximately one-eighth that of NVIDIA's H200. Furthermore, significant disparities remain in HBM memory capacity and bandwidth, which are critical for training large-scale models.

NVIDIA continues to defend its moat through a "CUDA Everywhere" strategy and an aggressive one-year architecture update cycle (Blackwell to Rubin). AMD is countering by targeting the "Memory Wall" challenge with larger memory capacities, such as the MI355X equipped with 288GB HBM3e.

Future Outlook: From Brute Force to Market Forking

Looking ahead, HDIN Research predicts a bifurcation in the market. The training sector will likely remain concentrated around top-tier GPUs like Blackwell. However, the inference market is expected to fragment as cost and efficiency drive the adoption of custom ASICs (such as TPUs) and high-performance Ethernet standards. By 2028, ASICs are projected to capture approximately 45% of the inference market share.

For Chinese vendors, the path forward involves leveraging local advantages in "AI Sovereignty" and focusing on system-level interconnect technologies to mitigate single-chip performance deficits. While the road remains challenging due to the hard computing power gap, opportunities exist in localized services and specific vertical applications.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. HDIN Research helps clients navigate complex industrial landscapes through rigorous data analysis and strategic insights.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com