Cumene Market Analysis 2026 - Phenol & Acetone Industry Chain Series Report (1)

Date : 2026-01-23

Reading : 571

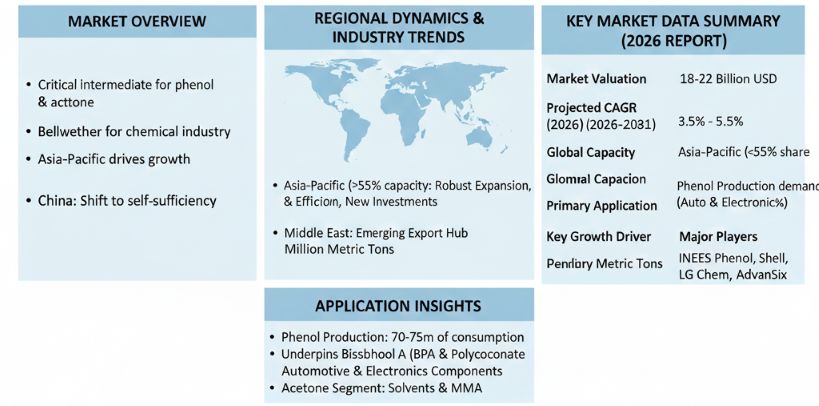

HDIN Research, an independent market consulting firm, has released its latest in-depth analysis titled "Cumene Market Insights 2026." The report outlines a fundamental transformation in the global petrochemical intermediate sector, valuing the global cumene market between 18 and 22 billion USD in 2026. The industry is projected to maintain a compound annual growth rate (CAGR) of 3.5% to 5.5% through 2031, driven primarily by aggressive industrialization in the Asia-Pacific region.

Market Overview

Cumene, a critical intermediate primarily used to produce phenol and acetone, serves as a bellwether for the broader chemical industry due to its extensive downstream applications in automotive, construction, and electronics sectors. The 2026 report highlights a clear divergence in global market dynamics: while mature markets in Europe and North America focus on rationalization and efficiency, Asia-Pacific has emerged as the undisputed engine of growth.

According to HDIN Research, global production capacity currently stands at approximately 24 million metric tons. The market is witnessing a historic shift in supply gravity. China has transitioned from a major importer to a self-sufficient powerhouse with a production capacity exceeding 8.7 million tons, fundamentally altering global trade flows.

Regional Dynamics and Industry Trends

The report details a "two-speed" market evolution. In Europe, high energy costs and competitive pressures have led to significant structural rationalization. Notable industry shifts include the permanent closure of several high-cost facilities, such as INEOS Phenol's Gladbeck plant and Mitsui Chemicals' Ichihara plant. These closures reflect a strategic pivot in mature markets toward integrated, high-efficiency operations to sustain margins.

Conversely, the Asia-Pacific region, led by China and India, is experiencing robust expansion. New investments, such as Haldia Petrochemicals' capacity increases in India and massive integrated refining projects in China, are driving regional growth. The region now accounts for over 55% of global capacity. The report also identifies the Middle East as an emerging production hub, leveraging advantaged feedstock availability to serve export markets.

Application Insights

Phenol production remains the dominant driver, accounting for approximately 70-75% of global cumene consumption. This demand is underpinned by the bisphenol A (BPA) and polycarbonate chains, which are essential for the production of lightweight automotive components and electronic housing materials. The acetone segment continues to grow steadily, supported by demand from solvents and methyl methacrylate (MMA) applications.

Figure Key Market Data Summary of Cumene

Future Outlook

HDIN Research forecasts that the next five years will be defined by the optimization of value chains. As Chinese capacity fully comes online, global trade patterns will shift from long-haul inter-regional shipments to localized supply networks. Furthermore, the industry is expected to see increased investment in process technologies that improve energy efficiency and yield, balancing the need for economic competitiveness with emerging sustainability goals.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We assist clients in navigating complex industrial landscapes through data-driven insights.

Media Contact:

HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

Market Overview

Cumene, a critical intermediate primarily used to produce phenol and acetone, serves as a bellwether for the broader chemical industry due to its extensive downstream applications in automotive, construction, and electronics sectors. The 2026 report highlights a clear divergence in global market dynamics: while mature markets in Europe and North America focus on rationalization and efficiency, Asia-Pacific has emerged as the undisputed engine of growth.

According to HDIN Research, global production capacity currently stands at approximately 24 million metric tons. The market is witnessing a historic shift in supply gravity. China has transitioned from a major importer to a self-sufficient powerhouse with a production capacity exceeding 8.7 million tons, fundamentally altering global trade flows.

Regional Dynamics and Industry Trends

The report details a "two-speed" market evolution. In Europe, high energy costs and competitive pressures have led to significant structural rationalization. Notable industry shifts include the permanent closure of several high-cost facilities, such as INEOS Phenol's Gladbeck plant and Mitsui Chemicals' Ichihara plant. These closures reflect a strategic pivot in mature markets toward integrated, high-efficiency operations to sustain margins.

Conversely, the Asia-Pacific region, led by China and India, is experiencing robust expansion. New investments, such as Haldia Petrochemicals' capacity increases in India and massive integrated refining projects in China, are driving regional growth. The region now accounts for over 55% of global capacity. The report also identifies the Middle East as an emerging production hub, leveraging advantaged feedstock availability to serve export markets.

Application Insights

Phenol production remains the dominant driver, accounting for approximately 70-75% of global cumene consumption. This demand is underpinned by the bisphenol A (BPA) and polycarbonate chains, which are essential for the production of lightweight automotive components and electronic housing materials. The acetone segment continues to grow steadily, supported by demand from solvents and methyl methacrylate (MMA) applications.

Figure Key Market Data Summary of Cumene

Future Outlook

HDIN Research forecasts that the next five years will be defined by the optimization of value chains. As Chinese capacity fully comes online, global trade patterns will shift from long-haul inter-regional shipments to localized supply networks. Furthermore, the industry is expected to see increased investment in process technologies that improve energy efficiency and yield, balancing the need for economic competitiveness with emerging sustainability goals.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We assist clients in navigating complex industrial landscapes through data-driven insights.

Media Contact:

HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com