High-Temperature Superconductivity Market Enters Commercial Explosion Phase in 2026: Fusion and AI Power the Surge

Date : 2026-01-15

Reading : 1744

HDIN Research, a leading independent market consulting firm, has released its latest comprehensive analysis on the High-Temperature Superconductivity (HTS) industry. The report indicates that the global HTS market has successfully transitioned from laboratory demonstration to large-scale commercial application, marking the beginning of a golden era driven by controlled nuclear fusion and next-generation AI data centers.

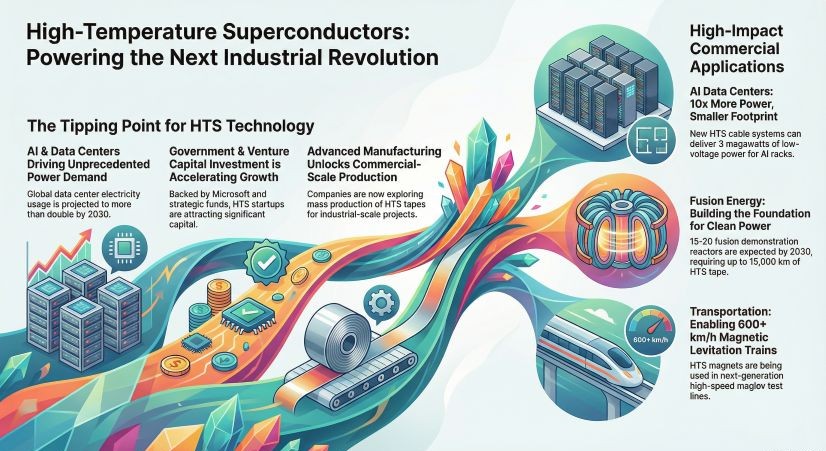

Figure HTS Powering the Industrial Revolution

From Scientific Theory to Industrial Reality

According to HDIN Research, the industry has overcome the historical "MacMillan Limit" and successfully moved from liquid helium to liquid nitrogen operating temperatures. Second-generation (2G) REBCO (Rare Earth Barium Copper Oxide) tapes have emerged as the dominant technological route, surpassing first-generation BSCCO materials due to superior mechanical properties and performance in high magnetic fields.

The report highlights that the industry is currently undergoing a "1 to 10" commercial explosion. In 2025, the sector witnessed a pivotal turning point where competition shifted from theoretical parameters to factory yield and delivery scale. Leading manufacturers have broken the 1,000-kilometer annual production barrier for 12mm wide tapes, signaling the maturity of mass production capabilities.

The Dual Engines of Growth: Nuclear Fusion and AI Data Centers

HDIN Research identifies controlled nuclear fusion as the single largest driver of the HTS market. The demand for compact tokamak devices, which require magnetic fields exceeding 20 Tesla, has created a voracious appetite for high-performance superconducting tapes.

Simultaneously, the boom in generative AI has opened a new, critical market. Modern data centers face severe power density and thermal management challenges. HTS cables, capable of transmitting power with zero resistance and requiring 20 times less space than traditional copper cabling, are reshaping data center infrastructure. The report notes that commercial pilots by companies like VEIR and LS Cable are validating the return on investment for superconducting power solutions in constrained urban environments.

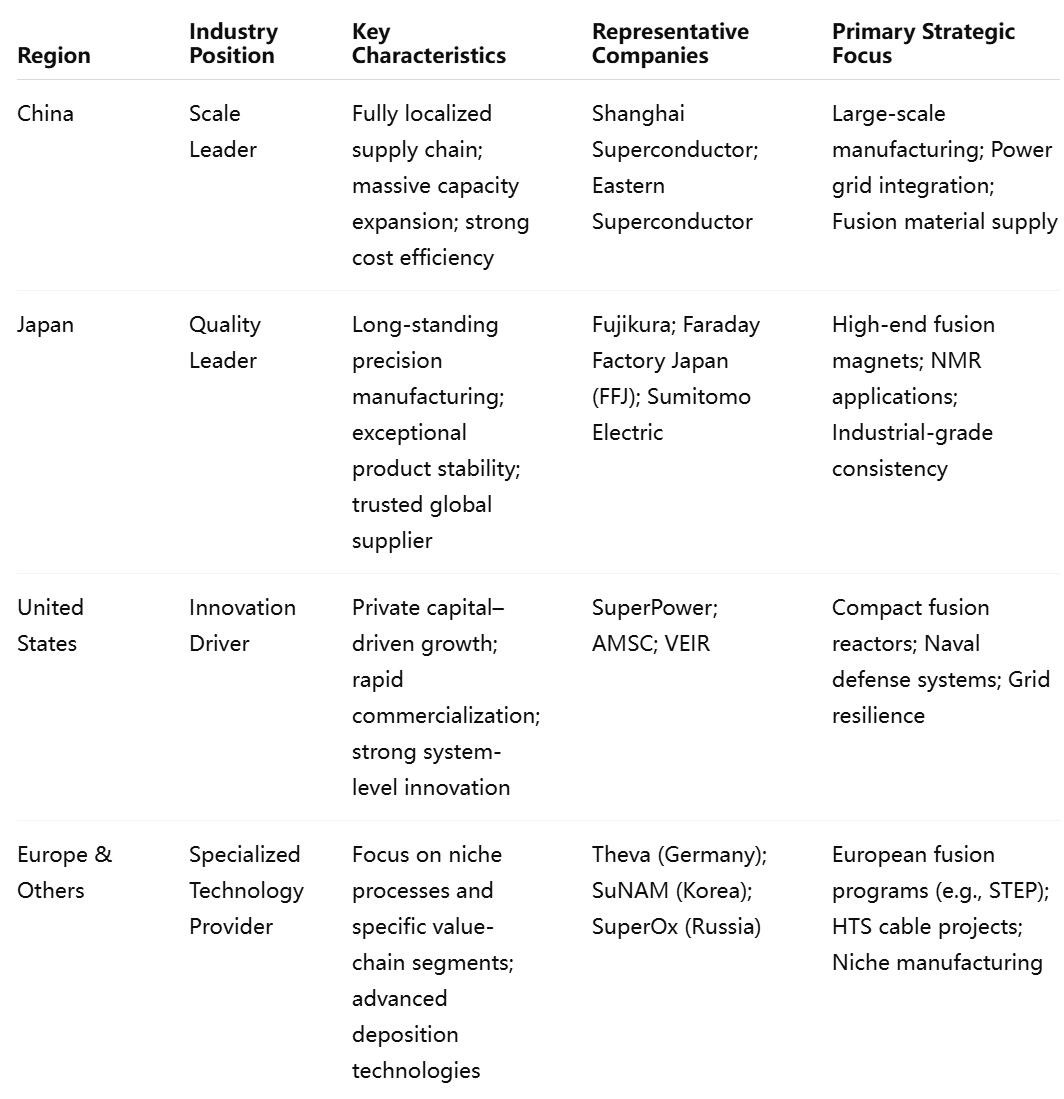

Global Competition Landscape

The analysis by HDIN Research reveals a distinct tiered structure in the global supply chain. China and Japan have established themselves as the manufacturing powerhouses of the industry, leading in capacity and yield. The United States maintains a strong position in disruptive innovation and capital-driven commercialization, particularly in the fusion sector.

The following table summarizes the competitive positions of key global regions:

Company Performance and Financial Outlook

The report provides a deep dive into corporate performance, noting a significant shift in financial health across the sector. 2025 is viewed as the "Year of Commercialization" where top-tier players like Shanghai Superconductor achieved profitability, driven by soaring demand and improved yields.

Japanese giants like Fujikura are aggressively expanding capacity, aiming to quadruple production by 2027 to meet the requirements of projects like the UK's STEP fusion reactor. Meanwhile, companies such as Lianchuang Opto in China have successfully monetized industrial applications, delivering megawatt-level superconducting induction heaters that significantly reduce energy consumption in metal processing.

Future Outlook

HDIN Research predicts that the cost of 2G HTS tapes will continue to decline as production scales up, further accelerating adoption in power grids and maglev transportation. The convergence of energy security needs (fusion) and digital transformation (AI) provides a dual-pillar support system that insulates the industry from single-market volatility.

Please click to watch the YouTube video of the report presentation.

For more information, please visit www.hdinresearch.com or contact sales@hdinresearch.com.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Figure HTS Powering the Industrial Revolution

From Scientific Theory to Industrial Reality

According to HDIN Research, the industry has overcome the historical "MacMillan Limit" and successfully moved from liquid helium to liquid nitrogen operating temperatures. Second-generation (2G) REBCO (Rare Earth Barium Copper Oxide) tapes have emerged as the dominant technological route, surpassing first-generation BSCCO materials due to superior mechanical properties and performance in high magnetic fields.

The report highlights that the industry is currently undergoing a "1 to 10" commercial explosion. In 2025, the sector witnessed a pivotal turning point where competition shifted from theoretical parameters to factory yield and delivery scale. Leading manufacturers have broken the 1,000-kilometer annual production barrier for 12mm wide tapes, signaling the maturity of mass production capabilities.

The Dual Engines of Growth: Nuclear Fusion and AI Data Centers

HDIN Research identifies controlled nuclear fusion as the single largest driver of the HTS market. The demand for compact tokamak devices, which require magnetic fields exceeding 20 Tesla, has created a voracious appetite for high-performance superconducting tapes.

Simultaneously, the boom in generative AI has opened a new, critical market. Modern data centers face severe power density and thermal management challenges. HTS cables, capable of transmitting power with zero resistance and requiring 20 times less space than traditional copper cabling, are reshaping data center infrastructure. The report notes that commercial pilots by companies like VEIR and LS Cable are validating the return on investment for superconducting power solutions in constrained urban environments.

Global Competition Landscape

The analysis by HDIN Research reveals a distinct tiered structure in the global supply chain. China and Japan have established themselves as the manufacturing powerhouses of the industry, leading in capacity and yield. The United States maintains a strong position in disruptive innovation and capital-driven commercialization, particularly in the fusion sector.

The following table summarizes the competitive positions of key global regions:

Company Performance and Financial Outlook

The report provides a deep dive into corporate performance, noting a significant shift in financial health across the sector. 2025 is viewed as the "Year of Commercialization" where top-tier players like Shanghai Superconductor achieved profitability, driven by soaring demand and improved yields.

Japanese giants like Fujikura are aggressively expanding capacity, aiming to quadruple production by 2027 to meet the requirements of projects like the UK's STEP fusion reactor. Meanwhile, companies such as Lianchuang Opto in China have successfully monetized industrial applications, delivering megawatt-level superconducting induction heaters that significantly reduce energy consumption in metal processing.

Future Outlook

HDIN Research predicts that the cost of 2G HTS tapes will continue to decline as production scales up, further accelerating adoption in power grids and maglev transportation. The convergence of energy security needs (fusion) and digital transformation (AI) provides a dual-pillar support system that insulates the industry from single-market volatility.

Please click to watch the YouTube video of the report presentation.

For more information, please visit www.hdinresearch.com or contact sales@hdinresearch.com.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.