Isopropyl Alcohol Market - Phenol & Acetone Industry Chain Series Report (7)

Date : 2026-01-27

Reading : 559

HDIN Research, a leading independent market consulting firm, has released its 2026 Isopropyl Alcohol (IPA) Market Insights report. The comprehensive study reveals that the global IPA market has successfully transitioned past the volatility of the COVID-19 pandemic, finding a new equilibrium driven by pharmaceutical stability and surging demand from the semiconductor sector.

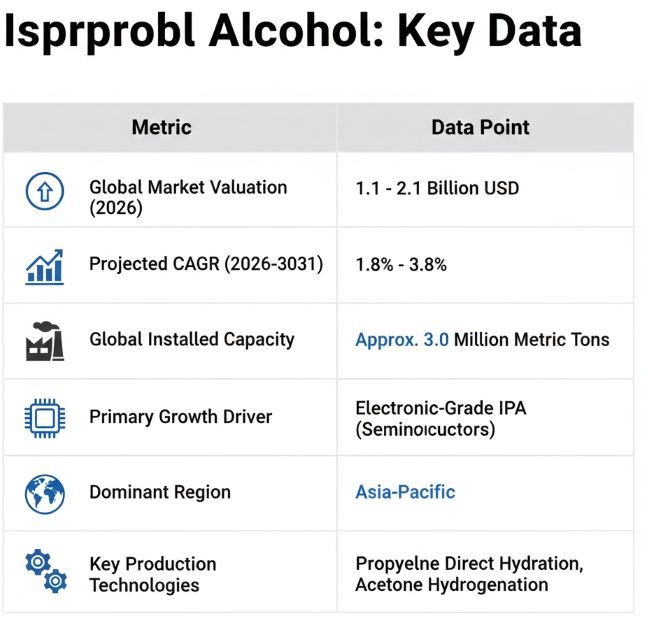

According to HDIN Research data, the global market valuation for 2026 is estimated between 1.1 and 2.1 billion USD, with a projected compound annual growth rate (CAGR) of 1.8% to 3.8% through 2031. The report highlights that while global production capacity has stabilized at approximately 3.0 million metric tons, the industry is witnessing a distinct divergence between commodity industrial-grade markets and the high-margin electronic-grade segment.

A Structural Shift in Demand

The analysis indicates that the unprecedented demand for hand sanitizers seen earlier in the decade has normalized, leading to structural overcapacity in certain regions, particularly China, where utilization rates currently hover between 50% and 60%. However, the market is finding renewed momentum in high-technology applications.

Electronic-grade IPA, with purity levels of 99.99% or higher, has emerged as the critical growth engine. As global semiconductor manufacturing expands through strategic initiatives in Asia, North America, and Europe, the demand for ultra-high purity solvents for wafer cleaning and processing is outpacing general industrial growth. This segment commands significant price premiums and has become the primary focus for specialized producers like Tokuyama.

Regional Dynamics and Production Technologies

Asia-Pacific remains the dominant force in the global landscape, serving as both the largest production hub and consumption market. The region is characterized by a mix of technologies, with Chinese producers favoring Acetone Hydrogenation due to feedstock economics, while North American and European producers predominantly utilize Propylene Direct Hydration.

The report notes that while China maintains the largest single-country capacity exceeding 800,000 metric tons, recent market pressures have led to capacity rationalization. In contrast, producers in Japan, South Korea, and Taiwan are aggressively expanding capabilities in high-purity grades to support local chip fabrication ecosystems.

North America and Europe continue to operate as mature markets with over 550,000 and 600,000 metric tons of capacity respectively. These regions are increasingly focused on supply security and downstream integration with pharmaceutical and automotive industries.

Figure Key Market Data of IPA

Competitive Landscape

The global market features a concentrated field of major integrated petrochemical players and specialized regional manufacturers. Key participants identified in the report include ExxonMobil, Shell, INEOS, LG Chem, and specialized high-purity producers such as Tokuyama.

HDIN Research highlights that competitive advantage is increasingly defined by vertical integration and the technical capability to meet parts-per-trillion impurity specifications required by modern nanometer-scale semiconductor manufacturing.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. The firm assists clients in navigating complex industry shifts through data-driven insights and strategic intelligence.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com

According to HDIN Research data, the global market valuation for 2026 is estimated between 1.1 and 2.1 billion USD, with a projected compound annual growth rate (CAGR) of 1.8% to 3.8% through 2031. The report highlights that while global production capacity has stabilized at approximately 3.0 million metric tons, the industry is witnessing a distinct divergence between commodity industrial-grade markets and the high-margin electronic-grade segment.

A Structural Shift in Demand

The analysis indicates that the unprecedented demand for hand sanitizers seen earlier in the decade has normalized, leading to structural overcapacity in certain regions, particularly China, where utilization rates currently hover between 50% and 60%. However, the market is finding renewed momentum in high-technology applications.

Electronic-grade IPA, with purity levels of 99.99% or higher, has emerged as the critical growth engine. As global semiconductor manufacturing expands through strategic initiatives in Asia, North America, and Europe, the demand for ultra-high purity solvents for wafer cleaning and processing is outpacing general industrial growth. This segment commands significant price premiums and has become the primary focus for specialized producers like Tokuyama.

Regional Dynamics and Production Technologies

Asia-Pacific remains the dominant force in the global landscape, serving as both the largest production hub and consumption market. The region is characterized by a mix of technologies, with Chinese producers favoring Acetone Hydrogenation due to feedstock economics, while North American and European producers predominantly utilize Propylene Direct Hydration.

The report notes that while China maintains the largest single-country capacity exceeding 800,000 metric tons, recent market pressures have led to capacity rationalization. In contrast, producers in Japan, South Korea, and Taiwan are aggressively expanding capabilities in high-purity grades to support local chip fabrication ecosystems.

North America and Europe continue to operate as mature markets with over 550,000 and 600,000 metric tons of capacity respectively. These regions are increasingly focused on supply security and downstream integration with pharmaceutical and automotive industries.

Figure Key Market Data of IPA

Competitive Landscape

The global market features a concentrated field of major integrated petrochemical players and specialized regional manufacturers. Key participants identified in the report include ExxonMobil, Shell, INEOS, LG Chem, and specialized high-purity producers such as Tokuyama.

HDIN Research highlights that competitive advantage is increasingly defined by vertical integration and the technical capability to meet parts-per-trillion impurity specifications required by modern nanometer-scale semiconductor manufacturing.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. The firm assists clients in navigating complex industry shifts through data-driven insights and strategic intelligence.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com