Global Crop Protection Industry at a Strategic Crossroads: Asset Transformation, Digitalization, and Biopesticides Redefine Future Growth

Date : 2026-01-23

Reading : 507

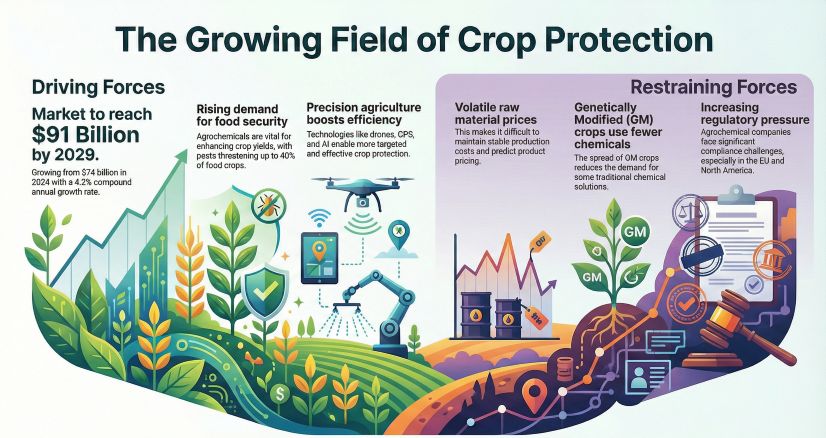

The global crop protection industry is currently navigating a profound structural transformation, moving rapidly from a volume-driven model to one defined by high-value services, regulatory compliance, and technological integration. According to a series of recent industry depth reports, the global market is projected to grow from approximately $79 billion in 2024 to nearly $118.5 billion by 2031, driven not just by demand, but by a fundamental reinvention of how crop protection is developed, manufactured, and delivered.

Industry analysts highlight three critical pillars reshaping the sector: a strategic pivot from heavy to light assets, the explosive growth of biopesticides driven by regulatory pressure, and the comprehensive digitalization of the value chain.

Figure The Growing Field of Crop Protection

From "Heavy Assets" to "Global Registrations"

A major trend identified in the reports is the shift in asset strategy among leading agrochemical companies. Historically, the industry prioritized heavy capital expenditure on expanding manufacturing capacity. Today, however, companies are pivoting toward an "Asset-Light" model that prioritizes global registrations and market access over brick-and-mortar expansion.

Companies like Rainbow Agro (Runfeng) are exemplifying this shift by focusing resources on acquiring high-barrier registrations in target countries, thereby securing market initiative and higher profit margins. Simultaneously, multinational giants like Bayer and FMC are optimizing their portfolios by divesting non-strategic assets to enhance flexibility and profitability. To mitigate supply chain risks, many firms are adopting "Backward Integration" strategies—controlling the production of key intermediates while keeping the broader business model agile.

The Rise of Biopesticides: A Structural Substitution

The era of relying solely on chemical pesticides is ending, driven by strict regulations such as the EU’s "Farm to Fork" strategy and increasingly stringent Maximum Residue Limits (MRLs) in export markets. The reports indicate that the biopesticides market is expected to grow at a CAGR of 13.7%, reaching $28.7 billion by 2028.

This shift is not a simple one-for-one replacement but a structural evolution toward Integrated Pest Management (IPM). Modern biotechnology, including genomic screening and nano-formulation technologies, has overcome historical issues with biopesticides, such as instability and slow action. Biopesticides are now critical tools for resistance management and pre-harvest applications to ensure zero-residue compliance.

Digitalization: The "Brain" of Modern Agriculture

Digital technology and Artificial Intelligence (AI) are rapidly becoming the nervous system of the crop protection industry, offering cost reduction and efficiency gains across the entire value chain:

* R&D: AI-driven molecular design (such as Bayer’s CropKey) and virtual screening are shortening the development cycle of new active ingredients from years to months.

* Manufacturing: Smart factories utilizing data monitoring are reducing production costs by up to 15%.

* Application: The combination of AI and mechanization—specifically drones and variable rate technology (VRT)—is transforming "spraying" into a precision service. Platforms like Syngenta’s Cropwise and FMC’s Arc™ farm intelligence allow for targeted application, significantly reducing chemical usage while maintaining yield.

Global Supply Chain and Competitive Landscape

The global supply chain is undergoing a "de-risking" process. While China remains the world's largest supplier of active ingredients (AIs), India is emerging as a key alternative hub through its PLI (Production Linked Incentive) schemes, attracting high-value custom synthesis manufacturing.

The competitive landscape remains highly concentrated, with the "Big 5" (Syngenta, Bayer, BASF, Corteva, FMC) holding approximately 72% of the global market. However, a "Tier 2" of agile, generic-focused companies is rising, leveraging global distribution networks and efficient manufacturing to challenge established norms.

Future Outlook

Analysts conclude that the winners of the next decade will be companies that successfully integrate "Seed + Crop Protection + Digital Services." As the industry faces a cycle of "de-capacity" and price adjustments, the ability to offer comprehensive, sustainable solutions rather than mere chemical products will determine market leadership.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research is a premier provider of market intelligence and consulting services. We specialize in delivering detailed data and strategic insights to help businesses navigate complex market landscapes.

Media Contact:

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com

Industry analysts highlight three critical pillars reshaping the sector: a strategic pivot from heavy to light assets, the explosive growth of biopesticides driven by regulatory pressure, and the comprehensive digitalization of the value chain.

Figure The Growing Field of Crop Protection

From "Heavy Assets" to "Global Registrations"

A major trend identified in the reports is the shift in asset strategy among leading agrochemical companies. Historically, the industry prioritized heavy capital expenditure on expanding manufacturing capacity. Today, however, companies are pivoting toward an "Asset-Light" model that prioritizes global registrations and market access over brick-and-mortar expansion.

Companies like Rainbow Agro (Runfeng) are exemplifying this shift by focusing resources on acquiring high-barrier registrations in target countries, thereby securing market initiative and higher profit margins. Simultaneously, multinational giants like Bayer and FMC are optimizing their portfolios by divesting non-strategic assets to enhance flexibility and profitability. To mitigate supply chain risks, many firms are adopting "Backward Integration" strategies—controlling the production of key intermediates while keeping the broader business model agile.

The Rise of Biopesticides: A Structural Substitution

The era of relying solely on chemical pesticides is ending, driven by strict regulations such as the EU’s "Farm to Fork" strategy and increasingly stringent Maximum Residue Limits (MRLs) in export markets. The reports indicate that the biopesticides market is expected to grow at a CAGR of 13.7%, reaching $28.7 billion by 2028.

This shift is not a simple one-for-one replacement but a structural evolution toward Integrated Pest Management (IPM). Modern biotechnology, including genomic screening and nano-formulation technologies, has overcome historical issues with biopesticides, such as instability and slow action. Biopesticides are now critical tools for resistance management and pre-harvest applications to ensure zero-residue compliance.

Digitalization: The "Brain" of Modern Agriculture

Digital technology and Artificial Intelligence (AI) are rapidly becoming the nervous system of the crop protection industry, offering cost reduction and efficiency gains across the entire value chain:

* R&D: AI-driven molecular design (such as Bayer’s CropKey) and virtual screening are shortening the development cycle of new active ingredients from years to months.

* Manufacturing: Smart factories utilizing data monitoring are reducing production costs by up to 15%.

* Application: The combination of AI and mechanization—specifically drones and variable rate technology (VRT)—is transforming "spraying" into a precision service. Platforms like Syngenta’s Cropwise and FMC’s Arc™ farm intelligence allow for targeted application, significantly reducing chemical usage while maintaining yield.

Global Supply Chain and Competitive Landscape

The global supply chain is undergoing a "de-risking" process. While China remains the world's largest supplier of active ingredients (AIs), India is emerging as a key alternative hub through its PLI (Production Linked Incentive) schemes, attracting high-value custom synthesis manufacturing.

The competitive landscape remains highly concentrated, with the "Big 5" (Syngenta, Bayer, BASF, Corteva, FMC) holding approximately 72% of the global market. However, a "Tier 2" of agile, generic-focused companies is rising, leveraging global distribution networks and efficient manufacturing to challenge established norms.

Future Outlook

Analysts conclude that the winners of the next decade will be companies that successfully integrate "Seed + Crop Protection + Digital Services." As the industry faces a cycle of "de-capacity" and price adjustments, the ability to offer comprehensive, sustainable solutions rather than mere chemical products will determine market leadership.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research is a premier provider of market intelligence and consulting services. We specialize in delivering detailed data and strategic insights to help businesses navigate complex market landscapes.

Media Contact:

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com