Magnesium Market: Supply Chain Fragility and Technical Bottlenecks Persist Despite Pricing Sweet Spot

Date : 2026-01-26

Reading : 634

HDIN Research, a leading independent market consulting firm, has released its latest comprehensive analysis on the global magnesium industry. The report highlights a critical paradox in the 2025 market landscape: while the magnesium-to-aluminum price ratio has hit a historic low, creating an ideal economic window for material substitution, the industry remains constrained by severe geopolitical supply risks and unresolved physical limitations in high-end applications.

According to HDIN Research analysts, the global magnesium market is currently navigating a period of high supply concentration intertwined with a forced green transition. While downstream demand in the automotive sector is accelerating due to lightweighting trends, the hype surrounding emerging sectors like humanoid robots warrants a cautious approach due to technical immaturity.

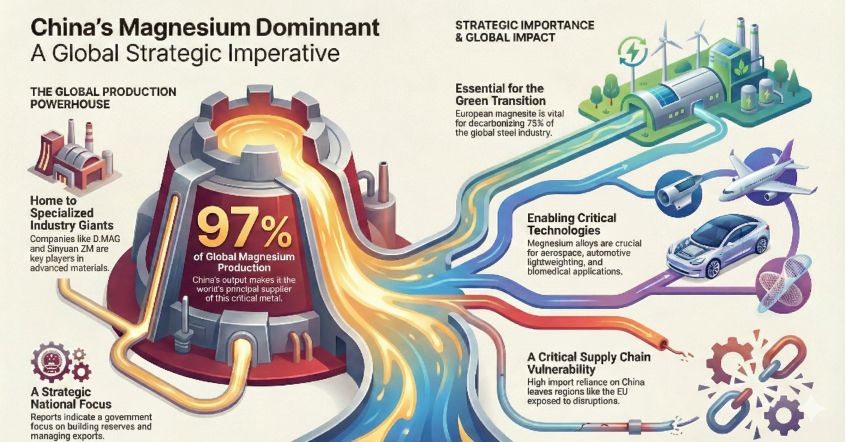

Figure China's Magnesium Dominant

The Supply Chain Dilemma: Extreme Concentration and Western Vulnerability

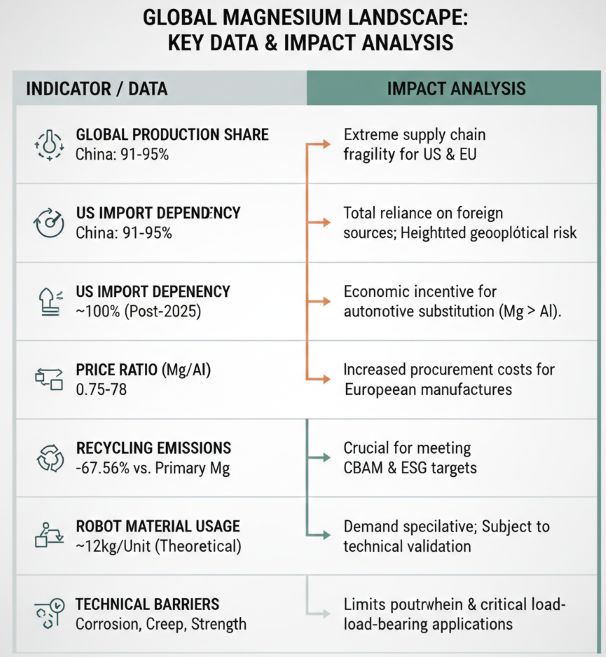

The global supply of primary magnesium remains heavily skewed. China continues to dominate the sector, controlling between 91% and 95% of global production, with the Yulin region in Shaanxi province alone accounting for nearly two-thirds of this output. This concentration presents a significant strategic vulnerability for Western markets.

The fragility of the Western supply chain was starkly illustrated in late 2025. Following equipment failures and financial struggles, US Magnesium, formerly the only primary producer in the United States, filed for bankruptcy protection. This development has left the US market effectively 100% dependent on imports.

In response, Western nations have classified magnesium as a critical strategic mineral. The European Union’s Critical Raw Materials Act (CRMA) and US initiatives attempt to foster decoupling. However, HDIN Research analysis indicates that building independent supply chains faces steep economic hurdles. The operating costs in Western regions, driven by labor and energy prices, result in production costs significantly higher than China’s coal-based Pidgeon Process. Furthermore, trade barriers, such as the US anti-dumping duties of 108.26% on Chinese pure magnesium, have created a synthetic price floor, forcing downstream manufacturers to pay a significant premium for security.

The Green Transition: Decarbonization as a Barrier to Entry

Environmental compliance has become the new trade barrier. The traditional Pidgeon Process used in China is energy-intensive and carbon-heavy. With the impending European Carbon Border Adjustment Mechanism (CBAM), high-carbon magnesium faces the risk of losing its cost advantage in the EU market.

This pressure is driving a technological shift toward Vertical Retort technology and recycling. The recycled magnesium market is emerging as a strategic defensive tool. Secondary magnesium production generates approximately 67.56% fewer greenhouse gas emissions compared to primary production. Companies like Magontec are leveraging this by expanding recycling capacities in Europe, offering a low-carbon alternative that bypasses the volatility of primary extraction.

Applications: The Reality Behind the Robot Hype

The report identifies the automotive sector as the pragmatic driver of demand, particularly for parts like dashboard cross-car beams (CCB) and seat frames. The current magnesium-to-aluminum price ratio, hovering between 0.75 and 0.78, makes magnesium an economically viable alternative for weight reduction in electric vehicles (EVs).

However, HDIN Research advises caution regarding the humanoid robot narrative. While market speculation suggests that humanoid robots could drive million-ton demand surges—based on a theoretical usage of 12kg per unit—commercial reality lags behind. Robot joints require fatigue strength and corrosion resistance that current magnesium alloys struggle to maintain under dynamic, high-frequency loads without expensive surface treatments.

Figure Market Data Summary of Magnesium Market

Analyst Commentary

A senior analyst at HDIN Research commented on the findings:

Investors and manufacturers must look beyond the attractive pricing. While the magnesium-to-aluminum ratio suggests a tipping point for substitution, the industry’s ceiling is currently defined by material science, not economics. The poor corrosion resistance and high-temperature creep of magnesium alloys remain unresolved bottlenecks for critical load-bearing components. Furthermore, the narrative surrounding humanoid robots driving a 'second growth curve' is currently outpacing the technical reality. The immediate opportunity lies in the recycling sector and the gradual penetration of large-scale automotive castings, provided that supply chains can navigate the rising tide of protectionist trade policies.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We help companies navigate complex industrial landscapes through rigorous data verification and objective analysis.

Media Contact

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

According to HDIN Research analysts, the global magnesium market is currently navigating a period of high supply concentration intertwined with a forced green transition. While downstream demand in the automotive sector is accelerating due to lightweighting trends, the hype surrounding emerging sectors like humanoid robots warrants a cautious approach due to technical immaturity.

Figure China's Magnesium Dominant

The Supply Chain Dilemma: Extreme Concentration and Western Vulnerability

The global supply of primary magnesium remains heavily skewed. China continues to dominate the sector, controlling between 91% and 95% of global production, with the Yulin region in Shaanxi province alone accounting for nearly two-thirds of this output. This concentration presents a significant strategic vulnerability for Western markets.

The fragility of the Western supply chain was starkly illustrated in late 2025. Following equipment failures and financial struggles, US Magnesium, formerly the only primary producer in the United States, filed for bankruptcy protection. This development has left the US market effectively 100% dependent on imports.

In response, Western nations have classified magnesium as a critical strategic mineral. The European Union’s Critical Raw Materials Act (CRMA) and US initiatives attempt to foster decoupling. However, HDIN Research analysis indicates that building independent supply chains faces steep economic hurdles. The operating costs in Western regions, driven by labor and energy prices, result in production costs significantly higher than China’s coal-based Pidgeon Process. Furthermore, trade barriers, such as the US anti-dumping duties of 108.26% on Chinese pure magnesium, have created a synthetic price floor, forcing downstream manufacturers to pay a significant premium for security.

The Green Transition: Decarbonization as a Barrier to Entry

Environmental compliance has become the new trade barrier. The traditional Pidgeon Process used in China is energy-intensive and carbon-heavy. With the impending European Carbon Border Adjustment Mechanism (CBAM), high-carbon magnesium faces the risk of losing its cost advantage in the EU market.

This pressure is driving a technological shift toward Vertical Retort technology and recycling. The recycled magnesium market is emerging as a strategic defensive tool. Secondary magnesium production generates approximately 67.56% fewer greenhouse gas emissions compared to primary production. Companies like Magontec are leveraging this by expanding recycling capacities in Europe, offering a low-carbon alternative that bypasses the volatility of primary extraction.

Applications: The Reality Behind the Robot Hype

The report identifies the automotive sector as the pragmatic driver of demand, particularly for parts like dashboard cross-car beams (CCB) and seat frames. The current magnesium-to-aluminum price ratio, hovering between 0.75 and 0.78, makes magnesium an economically viable alternative for weight reduction in electric vehicles (EVs).

However, HDIN Research advises caution regarding the humanoid robot narrative. While market speculation suggests that humanoid robots could drive million-ton demand surges—based on a theoretical usage of 12kg per unit—commercial reality lags behind. Robot joints require fatigue strength and corrosion resistance that current magnesium alloys struggle to maintain under dynamic, high-frequency loads without expensive surface treatments.

Figure Market Data Summary of Magnesium Market

Analyst Commentary

A senior analyst at HDIN Research commented on the findings:

Investors and manufacturers must look beyond the attractive pricing. While the magnesium-to-aluminum ratio suggests a tipping point for substitution, the industry’s ceiling is currently defined by material science, not economics. The poor corrosion resistance and high-temperature creep of magnesium alloys remain unresolved bottlenecks for critical load-bearing components. Furthermore, the narrative surrounding humanoid robots driving a 'second growth curve' is currently outpacing the technical reality. The immediate opportunity lies in the recycling sector and the gradual penetration of large-scale automotive castings, provided that supply chains can navigate the rising tide of protectionist trade policies.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We help companies navigate complex industrial landscapes through rigorous data verification and objective analysis.

Media Contact

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com