SK Innovation Transforms into Asia-Pacific Energy Titan: 2025 Strategic Outlook on Batteries and Green Transition

Date : 2026-01-18

Reading : 3251

HDIN Research, a leading independent market consulting firm, has released a comprehensive analysis of SK Innovation following its aggressive restructuring and strategic pivot in 2025. The report highlights the company's transformation into the largest private comprehensive energy company in the Asia-Pacific region, driven by the mega-merger with SK E&S and a diversified battery technology roadmap aimed at overcoming the current electric vehicle (EV) demand slowdown.

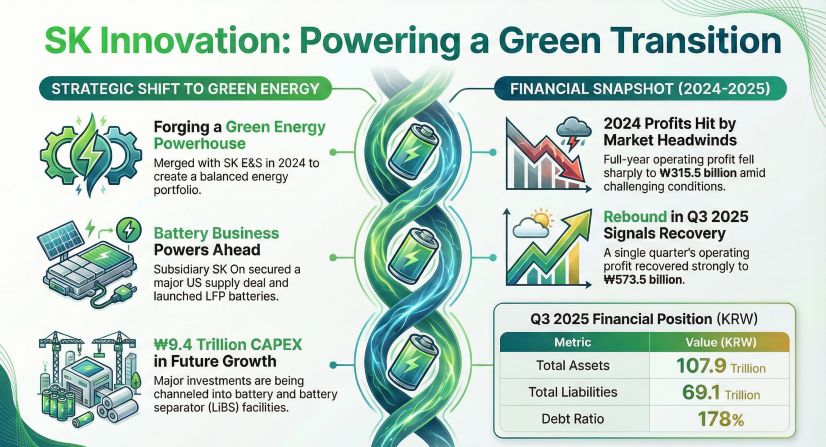

According to HDIN Research analysts, SK Innovation has successfully restructured its portfolio to balance traditional cash-generating assets with future growth engines. The completion of the merger with SK E&S on November 1, 2024, and the subsequent consolidation of SK On with SK Enmove in November 2025, represents a decisive move to stabilize financial structures while funding the transition to green energy.

Figure SK Innovation Powering a Green Transition

Strategic Mergers and Asset Restructuring

The integration of SK E&S has fortified SK Innovation's value chain, combining upstream LNG development, power generation, and city gas supply with its existing refining prowess. As of the third quarter of 2025, the consolidated assets of the company stand at approximately 107.9 trillion KRW.

HDIN Research analysis indicates that while the petroleum business remains the primary revenue driver, contributing 58% of total revenue, the merged entity now possesses a robust LNG value chain (14% of revenue) that serves as a financial buffer. This structure is designed to support the capital-intensive battery division (SK On), which currently accounts for 9% of revenue but holds 58% of the group's tangible and intangible assets, reflecting the massive investment in future capabilities.

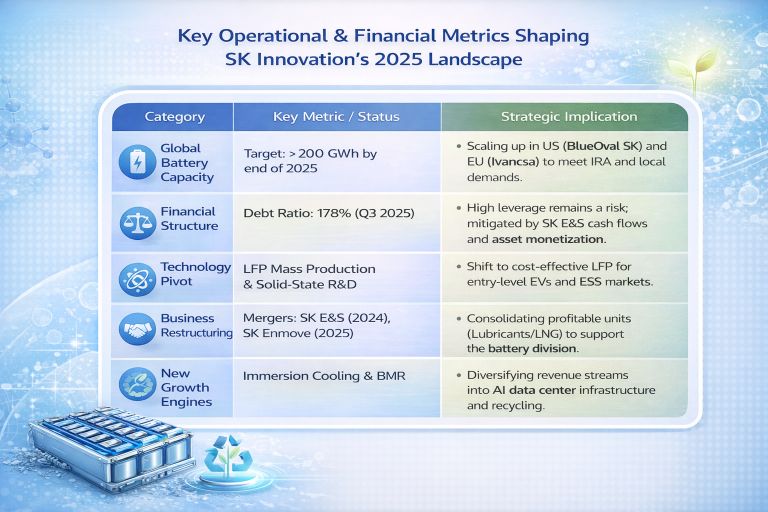

SK On: 2025 Capacity Targets and Technology Roadmap

Despite the global "Chasm" in EV adoption, SK Innovation maintains an aggressive expansion strategy for its battery subsidiary, SK On. The company has set a global production capacity target of over 200 GWh by the end of 2025. The breakdown of this projected capacity includes approximately 78 GWh in China, 59 GWh in the United States, 48 GWh in Europe, and 7 GWh in Korea.

To mitigate the risks associated with slowing EV demand, SK On is executing a dual-track strategy:

1. Product Diversification: The company has successfully achieved mass production and supply of LFP (Lithium Iron Phosphate) batteries, marking a critical expansion from its traditional high-nickel ternary dominance into more cost-competitive chemistries.

2. Market Expansion: Leveraging its LFP technology, SK On is aggressively entering the Energy Storage System (ESS) market, particularly in North America, to offset volatility in the automotive sector.

In the realm of next-generation technology, R&D efforts at the Daejeon R&D Center are focused on commercializing solid-state and semi-solid-state batteries, along with proprietary solid electrolytes. The company is also advancing Cell-to-Pack (CTP) technologies to enhance energy density.

Green Anchor Strategy: Beyond Batteries

The report highlights SK Innovation's "Green Anchor" strategy, which extends beyond battery manufacturing. Key R&D initiatives include:

Carbon Capture Utilization and Storage (CCUS): Developing high-performance separation membranes for CO2 capture.

Battery Metal Recycling (BMR): Commercializing technologies to recover lithium, nickel, and cobalt from spent batteries.

Immersion Cooling: Leveraging its lubricants business to develop specialized fluids for liquid cooling in data centers, directly addressing the thermal management needs of the booming AI server market.

Figure Market Data Summary of SK Innovation

Analyst Commentary

A senior analyst at HDIN Research commented on the outlook:

SK Innovation is executing a high-stakes balancing act. By merging with SK E&S and SK Enmove, the company has effectively utilized its profitable oil and LNG businesses to subsidize the capital-intensive ramp-up of its battery division. While the debt ratio of 178% is significant, the shift toward LFP batteries and the ESS market demonstrates a pragmatic response to the current EV market slowdown. The immediate challenge lies in stabilizing SK On's yield rates at new global facilities and maximizing the benefits from the US Advanced Manufacturing Production Credit (AMPC) to achieve sustained profitability in the battery segment.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We help companies navigate complex industrial landscapes through rigorous data verification and objective analysis.

Media Contact

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

According to HDIN Research analysts, SK Innovation has successfully restructured its portfolio to balance traditional cash-generating assets with future growth engines. The completion of the merger with SK E&S on November 1, 2024, and the subsequent consolidation of SK On with SK Enmove in November 2025, represents a decisive move to stabilize financial structures while funding the transition to green energy.

Figure SK Innovation Powering a Green Transition

Strategic Mergers and Asset Restructuring

The integration of SK E&S has fortified SK Innovation's value chain, combining upstream LNG development, power generation, and city gas supply with its existing refining prowess. As of the third quarter of 2025, the consolidated assets of the company stand at approximately 107.9 trillion KRW.

HDIN Research analysis indicates that while the petroleum business remains the primary revenue driver, contributing 58% of total revenue, the merged entity now possesses a robust LNG value chain (14% of revenue) that serves as a financial buffer. This structure is designed to support the capital-intensive battery division (SK On), which currently accounts for 9% of revenue but holds 58% of the group's tangible and intangible assets, reflecting the massive investment in future capabilities.

SK On: 2025 Capacity Targets and Technology Roadmap

Despite the global "Chasm" in EV adoption, SK Innovation maintains an aggressive expansion strategy for its battery subsidiary, SK On. The company has set a global production capacity target of over 200 GWh by the end of 2025. The breakdown of this projected capacity includes approximately 78 GWh in China, 59 GWh in the United States, 48 GWh in Europe, and 7 GWh in Korea.

To mitigate the risks associated with slowing EV demand, SK On is executing a dual-track strategy:

1. Product Diversification: The company has successfully achieved mass production and supply of LFP (Lithium Iron Phosphate) batteries, marking a critical expansion from its traditional high-nickel ternary dominance into more cost-competitive chemistries.

2. Market Expansion: Leveraging its LFP technology, SK On is aggressively entering the Energy Storage System (ESS) market, particularly in North America, to offset volatility in the automotive sector.

In the realm of next-generation technology, R&D efforts at the Daejeon R&D Center are focused on commercializing solid-state and semi-solid-state batteries, along with proprietary solid electrolytes. The company is also advancing Cell-to-Pack (CTP) technologies to enhance energy density.

Green Anchor Strategy: Beyond Batteries

The report highlights SK Innovation's "Green Anchor" strategy, which extends beyond battery manufacturing. Key R&D initiatives include:

Carbon Capture Utilization and Storage (CCUS): Developing high-performance separation membranes for CO2 capture.

Battery Metal Recycling (BMR): Commercializing technologies to recover lithium, nickel, and cobalt from spent batteries.

Immersion Cooling: Leveraging its lubricants business to develop specialized fluids for liquid cooling in data centers, directly addressing the thermal management needs of the booming AI server market.

Figure Market Data Summary of SK Innovation

Analyst Commentary

A senior analyst at HDIN Research commented on the outlook:

SK Innovation is executing a high-stakes balancing act. By merging with SK E&S and SK Enmove, the company has effectively utilized its profitable oil and LNG businesses to subsidize the capital-intensive ramp-up of its battery division. While the debt ratio of 178% is significant, the shift toward LFP batteries and the ESS market demonstrates a pragmatic response to the current EV market slowdown. The immediate challenge lies in stabilizing SK On's yield rates at new global facilities and maximizing the benefits from the US Advanced Manufacturing Production Credit (AMPC) to achieve sustained profitability in the battery segment.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. We help companies navigate complex industrial landscapes through rigorous data verification and objective analysis.

Media Contact

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com