Uranium Market to Hit Critical Demand Tipping Point in 2027, Reports HDIN Research

Date : 2026-01-27

Reading : 5237

HDIN Research, an independent market consulting firm, has released a comprehensive analysis of the global natural uranium market, identifying 2027 as a pivotal year for the industry. The report details a convergence of factors including the maturation of nuclear construction cycles, a structural shift in fuel enrichment processes, and the rising energy demands of artificial intelligence, all contributing to a projected surge in uranium consumption.

According to HDIN Research, the market is currently pricing in a transition from linear demand growth to an accelerated release phase. This shift is driven by the completion of reactor projects initiated around 2018 and the depletion of secondary supplies that have historically acted as a market buffer.

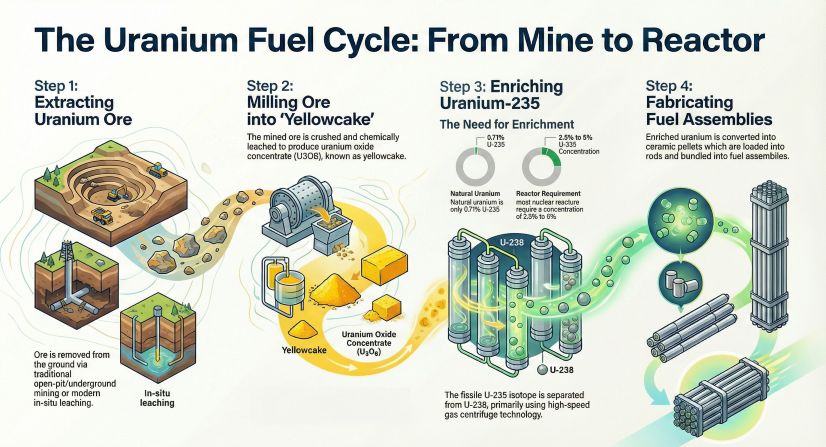

Figure The Uranium Fuel Cycle From Mine to Reactor

The Nine-Year Lag and The Initial Core Effect

HDIN Research analysis highlights that the construction of nuclear reactors involves a complex cycle spanning 7 to 11 years. Data indicates that global nuclear construction capacity bottomed out in 2018 before beginning a gradual recovery. Based on average construction timelines, projects that broke ground during this recovery period are scheduled for completion around 2027.

The report emphasizes the "Initial Core" phenomenon as a primary driver for the 2027 demand spike. A standard 1GW pressurized water reactor requires approximately 400 tons of natural uranium for its initial startup, compared to only 175-200 tons for annual refueling. Consequently, the wave of new reactors coming online in 2027 will generate a front-loaded demand pulse significantly larger than the actual increase in power generation capacity.

Figure Key Drivers of Uranium Demand Acceleration (2027 Forecast)

Geopolitical Reshaping and Supply Chain Constraints

The HDIN Research report further explores how the conflict in Ukraine has fundamentally altered the nuclear fuel supply chain. The industry is witnessing a shift from globalization to regional security. With Western nations reducing reliance on Russian enrichment capacity, local enrichment plants have shifted from "underfeeding" to "overfeeding" operations. This operational change increases the consumption of natural uranium feedstock to compensate for limited enrichment work units (SWU), effectively turning a former source of secondary supply into a new source of demand.

Furthermore, logistics have become a critical variable. The Trans-Caspian International Transport Route (TITR) has emerged as a vital alternative for Kazakh uranium to reach Western markets, bypassing Russian territory, though this adds complexity and cost to the supply chain.

AI and the Future of Baseload Power

Beyond traditional grid demand, HDIN Research identifies the technology sector as an emerging catalyst. Artificial Intelligence data centers require 24/7 stable baseload power, a requirement that intermittent renewables cannot meet without massive storage. Nuclear energy is increasingly viewed as the only scalable low-carbon solution for these needs. Tech giants are entering long-term power purchase agreements, with timelines often targeting 2026-2030, further tightening the projected market balance in 2027.

While Generation IV reactors and Small Modular Reactors (SMRs) represent the future of the industry, HDIN Research notes that these technologies will not alleviate the immediate uranium shortage. In fact, advanced designs may initially increase demand for specific fuel types like HALEU, placing additional stress on the enrichment sector.

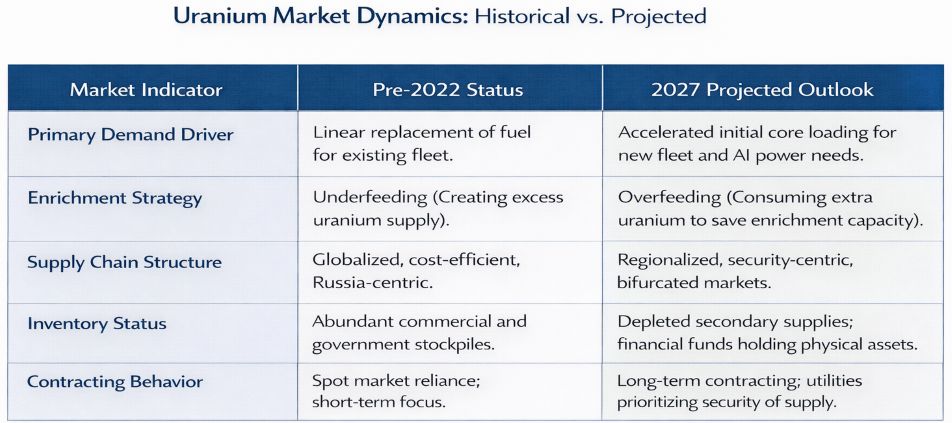

Figure Market Dynamics: Historical vs. Projected

Conclusion and Outlook

The analysis concludes that the era of low uranium prices driven by inventory liquidation is over. With the depletion of secondary supplies expected to accelerate through 2035, and a distinct lack of investment in new mining capacity between 2014 and 2020, the supply-side response is lagging. HDIN Research advises market participants to closely monitor the 2027 window, where the confluence of new reactor startups, enrichment overfeeding, and supply rigidity is likely to create significant price volatility.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. HDIN Research assists clients in navigating complex industrial landscapes through data-driven insights and rigorous methodology.

Media Contact:

Company Name: HDIN Research

Contact Person: Sales Department

Email: sales@hdinresearch.com

Website: www.hdinresearch.com

According to HDIN Research, the market is currently pricing in a transition from linear demand growth to an accelerated release phase. This shift is driven by the completion of reactor projects initiated around 2018 and the depletion of secondary supplies that have historically acted as a market buffer.

Figure The Uranium Fuel Cycle From Mine to Reactor

The Nine-Year Lag and The Initial Core Effect

HDIN Research analysis highlights that the construction of nuclear reactors involves a complex cycle spanning 7 to 11 years. Data indicates that global nuclear construction capacity bottomed out in 2018 before beginning a gradual recovery. Based on average construction timelines, projects that broke ground during this recovery period are scheduled for completion around 2027.

The report emphasizes the "Initial Core" phenomenon as a primary driver for the 2027 demand spike. A standard 1GW pressurized water reactor requires approximately 400 tons of natural uranium for its initial startup, compared to only 175-200 tons for annual refueling. Consequently, the wave of new reactors coming online in 2027 will generate a front-loaded demand pulse significantly larger than the actual increase in power generation capacity.

Figure Key Drivers of Uranium Demand Acceleration (2027 Forecast)

Geopolitical Reshaping and Supply Chain Constraints

The HDIN Research report further explores how the conflict in Ukraine has fundamentally altered the nuclear fuel supply chain. The industry is witnessing a shift from globalization to regional security. With Western nations reducing reliance on Russian enrichment capacity, local enrichment plants have shifted from "underfeeding" to "overfeeding" operations. This operational change increases the consumption of natural uranium feedstock to compensate for limited enrichment work units (SWU), effectively turning a former source of secondary supply into a new source of demand.

Furthermore, logistics have become a critical variable. The Trans-Caspian International Transport Route (TITR) has emerged as a vital alternative for Kazakh uranium to reach Western markets, bypassing Russian territory, though this adds complexity and cost to the supply chain.

AI and the Future of Baseload Power

Beyond traditional grid demand, HDIN Research identifies the technology sector as an emerging catalyst. Artificial Intelligence data centers require 24/7 stable baseload power, a requirement that intermittent renewables cannot meet without massive storage. Nuclear energy is increasingly viewed as the only scalable low-carbon solution for these needs. Tech giants are entering long-term power purchase agreements, with timelines often targeting 2026-2030, further tightening the projected market balance in 2027.

While Generation IV reactors and Small Modular Reactors (SMRs) represent the future of the industry, HDIN Research notes that these technologies will not alleviate the immediate uranium shortage. In fact, advanced designs may initially increase demand for specific fuel types like HALEU, placing additional stress on the enrichment sector.

Figure Market Dynamics: Historical vs. Projected

Conclusion and Outlook

The analysis concludes that the era of low uranium prices driven by inventory liquidation is over. With the depletion of secondary supplies expected to accelerate through 2035, and a distinct lack of investment in new mining capacity between 2014 and 2020, the supply-side response is lagging. HDIN Research advises market participants to closely monitor the 2027 window, where the confluence of new reactor startups, enrichment overfeeding, and supply rigidity is likely to create significant price volatility.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. HDIN Research assists clients in navigating complex industrial landscapes through data-driven insights and rigorous methodology.

Media Contact:

Company Name: HDIN Research

Contact Person: Sales Department

Email: sales@hdinresearch.com

Website: www.hdinresearch.com