Solar Module Backsheet Market Insights 2026 Analysis and Forecast

Date : 2026-02-13

Reading : 172

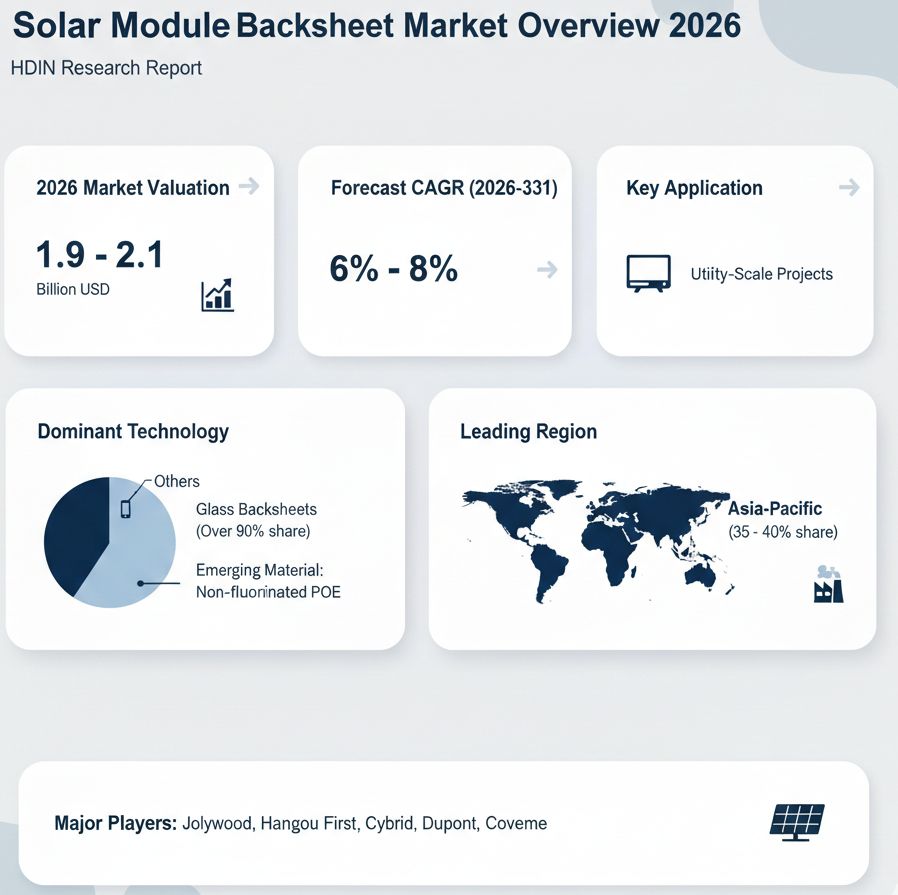

HDIN Research has released its latest comprehensive study titled Solar Module Backsheet Global Market Insights 2026. The report indicates that the global market for solar module backsheets has demonstrated robust growth, reaching a valuation between 1.9 billion and 2.1 billion USD in 2026. As a critical component for the insulation and protection of photovoltaic modules, the backsheet market is projected to maintain a compound annual growth rate (CAGR) of 6 percent to 8 percent through 2031.

The primary driver for this market expansion is the rapid acceleration of global solar photovoltaic installations. According to the report, renewable energy capacity reached record highs recently, with significant contributions from China, the United States, and Europe. Backsheets are essential for ensuring the 25 to 30-year operational lifespan of solar panels by blocking moisture, preventing UV degradation, and providing electrical insulation.

Technological shifts within the industry are reshaping the market landscape. The report highlights that glass backsheets have emerged as the dominant technology, capturing over 90 percent of the market share. This dominance is attributed to the rise of bifacial modules and the superior durability of glass-glass configurations. Additionally, non-fluorinated backsheets, particularly those based on polyolefin elastomers (POE), are seeing rapid adoption due to their compatibility with next-generation N-type solar cells and superior resistance to potential-induced degradation.

Regionally, the Asia-Pacific region commands the largest share of the global market, estimated at 35 to 40 percent. This is largely due to China holding a dominant position in the solar supply chain, accounting for the vast majority of global polysilicon, wafer, cell, and module production. The North American market is also experiencing acceleration, driven by supportive federal policies and a surge in utility-scale projects.

Figure Market Data Summary of Solar Module Backsheet

The competitive landscape is characterized by a mix of specialized solar material manufacturers and diversified chemical giants. Chinese manufacturers such as Jolywood, Hangzhou First, and Cybrid Technologies lead in production volume, leveraging integrated manufacturing capabilities. International players like DuPont, Coveme, and 3M continue to maintain strong positions through advanced material science and premium product offerings.

The competitive landscape is characterized by a mix of specialized solar material manufacturers and diversified chemical giants. Chinese manufacturers such as Jolywood, Hangzhou First, and Cybrid Technologies lead in production volume, leveraging integrated manufacturing capabilities. International players like DuPont, Coveme, and 3M continue to maintain strong positions through advanced material science and premium product offerings.

Despite the positive growth trajectory, the industry faces challenges related to raw material price volatility. Costs for PET films and fluoropolymers significantly influence profitability. Furthermore, the intense price competition in standard product categories is pushing manufacturers to innovate continuously. The report suggests that sustainability is becoming a key differentiator, with increased focus on recyclable backsheet formulations to meet circular economy goals.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. The company aids clients in understanding complex market dynamics and making informed strategic decisions.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com

The primary driver for this market expansion is the rapid acceleration of global solar photovoltaic installations. According to the report, renewable energy capacity reached record highs recently, with significant contributions from China, the United States, and Europe. Backsheets are essential for ensuring the 25 to 30-year operational lifespan of solar panels by blocking moisture, preventing UV degradation, and providing electrical insulation.

Technological shifts within the industry are reshaping the market landscape. The report highlights that glass backsheets have emerged as the dominant technology, capturing over 90 percent of the market share. This dominance is attributed to the rise of bifacial modules and the superior durability of glass-glass configurations. Additionally, non-fluorinated backsheets, particularly those based on polyolefin elastomers (POE), are seeing rapid adoption due to their compatibility with next-generation N-type solar cells and superior resistance to potential-induced degradation.

Regionally, the Asia-Pacific region commands the largest share of the global market, estimated at 35 to 40 percent. This is largely due to China holding a dominant position in the solar supply chain, accounting for the vast majority of global polysilicon, wafer, cell, and module production. The North American market is also experiencing acceleration, driven by supportive federal policies and a surge in utility-scale projects.

Figure Market Data Summary of Solar Module Backsheet

The competitive landscape is characterized by a mix of specialized solar material manufacturers and diversified chemical giants. Chinese manufacturers such as Jolywood, Hangzhou First, and Cybrid Technologies lead in production volume, leveraging integrated manufacturing capabilities. International players like DuPont, Coveme, and 3M continue to maintain strong positions through advanced material science and premium product offerings.Despite the positive growth trajectory, the industry faces challenges related to raw material price volatility. Costs for PET films and fluoropolymers significantly influence profitability. Furthermore, the intense price competition in standard product categories is pushing manufacturers to innovate continuously. The report suggests that sustainability is becoming a key differentiator, with increased focus on recyclable backsheet formulations to meet circular economy goals.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. The company aids clients in understanding complex market dynamics and making informed strategic decisions.

Media Contact

HDIN Research

Email: sales@hdinresearch.com

Website: www.hdinresearch.com