Solar Junction Box Market Projected to Reach USD 2.0 Billion by 2026 as Photovoltaic Installations Accelerate

Date : 2026-02-13

Reading : 81

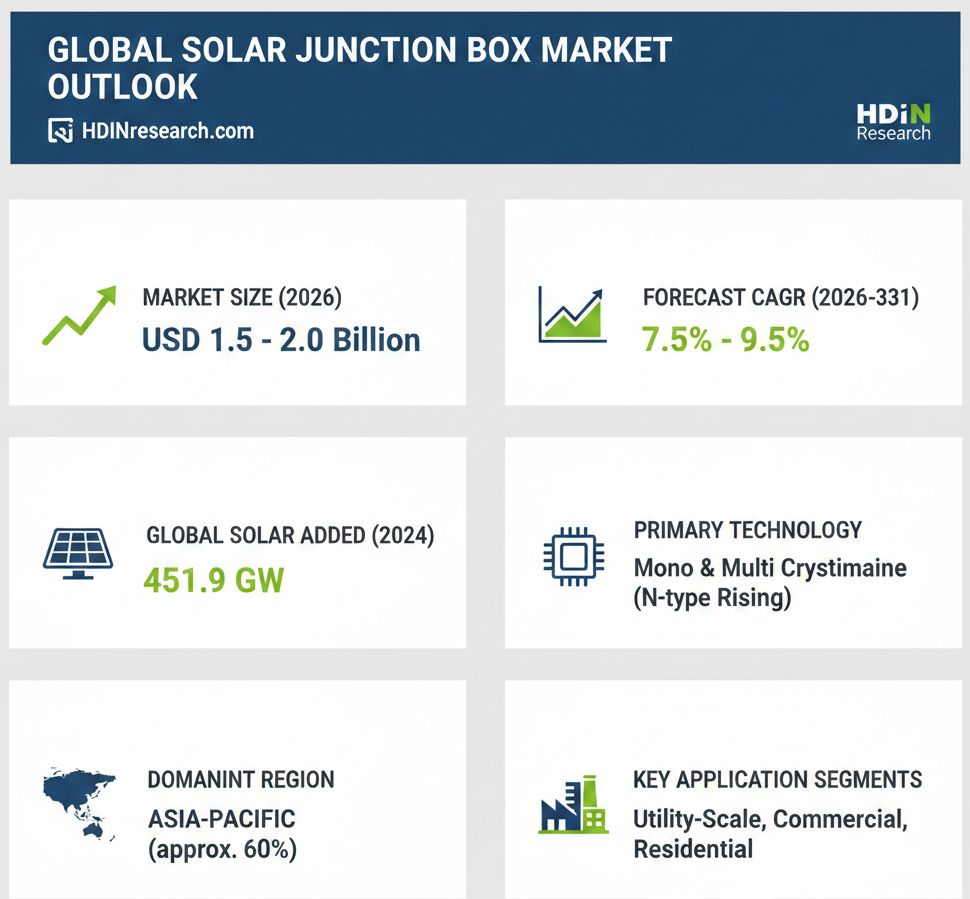

HDIN Research has released a comprehensive new market study titled "Solar Junction Box Global Market Insights 2026," offering an in-depth analysis of the industry landscape, technological trends, and growth forecasts through 2031. The report identifies the solar junction box sector as a critical component of the global energy transition, with market valuation expected to range between USD 1.5 billion and USD 2.0 billion by 2026.

As the photovoltaic (PV) industry experiences unprecedented expansion, the demand for reliable electrical connection and protection devices has surged. The market is projected to expand at a compound annual growth rate (CAGR) of 7.5% to 9.5% from 2026 through 2031. This growth trajectory is intrinsically linked to the massive deployment of solar capacity worldwide, which saw approximately 451.9 GW of new installations commissioned in 2024 alone.

The research highlights that the Asia-Pacific region continues to dominate the global market, largely driven by China's commanding position in both solar manufacturing and installation. In 2024, China accounted for nearly 60% of global solar capacity additions, installing up to 357.3 GW. Significant momentum was also observed in India, which added 31.9 GW, overtaking Japan to become the fourth-largest solar market globally. Meanwhile, the North American and European markets remain vital, with the United States adding 38.3 GW and Europe installing 71.4 GW in 2024.

Technological evolution plays a pivotal role in shaping market dynamics. The industry is witnessing a decisive shift toward high-efficiency module designs. Monocrystalline silicon technology now accounts for approximately 98% of global production, with N-type wafers, particularly TOPCon technology, achieving over 70% market share in 2024. This transition requires junction boxes capable of handling higher current ratings and improved thermal management. Additionally, the report notes a growing segment for smart junction boxes equipped with monitoring and diagnostic capabilities, particularly for commercial and residential applications where system optimization is a priority.

The competitive landscape remains fragmented with a mix of high-volume manufacturing leaders and specialized premium suppliers. Chinese manufacturers, such as Jiangsu Tonglin Electric and QC Solar Corporation, hold dominant market shares due to their proximity to module production hubs. International players like Amphenol and Staubli continue to lead in premium segments, offering specialized products that cater to markets requiring advanced features and stringent safety certifications.

Despite the positive outlook, the market faces challenges including intense price competition and manufacturing overcapacity. The commodity nature of standard junction boxes places pressure on margins, driving manufacturers to focus on cost efficiency and automated production. However, the critical role of junction boxes in ensuring system safety and the 25-year reliability required for solar modules continues to drive investment in quality and innovation.

Figure Market Data Summary of Solar Junction Box

The report by HDIN Research provides a granular breakdown of the market by technology, application, and geography, offering stakeholders a clear view of the opportunities and risks in the coming decade. As the world accelerates toward renewable energy targets, the solar junction box market is positioned for sustained development, supported by declining technology costs and strong corporate sustainability commitments.

The report by HDIN Research provides a granular breakdown of the market by technology, application, and geography, offering stakeholders a clear view of the opportunities and risks in the coming decade. As the world accelerates toward renewable energy targets, the solar junction box market is positioned for sustained development, supported by declining technology costs and strong corporate sustainability commitments.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. By leveraging comprehensive data sources and rigorous analytical methodologies, HDIN Research assists businesses in navigating complex industry landscapes and making informed strategic decisions.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com

As the photovoltaic (PV) industry experiences unprecedented expansion, the demand for reliable electrical connection and protection devices has surged. The market is projected to expand at a compound annual growth rate (CAGR) of 7.5% to 9.5% from 2026 through 2031. This growth trajectory is intrinsically linked to the massive deployment of solar capacity worldwide, which saw approximately 451.9 GW of new installations commissioned in 2024 alone.

The research highlights that the Asia-Pacific region continues to dominate the global market, largely driven by China's commanding position in both solar manufacturing and installation. In 2024, China accounted for nearly 60% of global solar capacity additions, installing up to 357.3 GW. Significant momentum was also observed in India, which added 31.9 GW, overtaking Japan to become the fourth-largest solar market globally. Meanwhile, the North American and European markets remain vital, with the United States adding 38.3 GW and Europe installing 71.4 GW in 2024.

Technological evolution plays a pivotal role in shaping market dynamics. The industry is witnessing a decisive shift toward high-efficiency module designs. Monocrystalline silicon technology now accounts for approximately 98% of global production, with N-type wafers, particularly TOPCon technology, achieving over 70% market share in 2024. This transition requires junction boxes capable of handling higher current ratings and improved thermal management. Additionally, the report notes a growing segment for smart junction boxes equipped with monitoring and diagnostic capabilities, particularly for commercial and residential applications where system optimization is a priority.

The competitive landscape remains fragmented with a mix of high-volume manufacturing leaders and specialized premium suppliers. Chinese manufacturers, such as Jiangsu Tonglin Electric and QC Solar Corporation, hold dominant market shares due to their proximity to module production hubs. International players like Amphenol and Staubli continue to lead in premium segments, offering specialized products that cater to markets requiring advanced features and stringent safety certifications.

Despite the positive outlook, the market faces challenges including intense price competition and manufacturing overcapacity. The commodity nature of standard junction boxes places pressure on margins, driving manufacturers to focus on cost efficiency and automated production. However, the critical role of junction boxes in ensuring system safety and the 25-year reliability required for solar modules continues to drive investment in quality and innovation.

Figure Market Data Summary of Solar Junction Box

The report by HDIN Research provides a granular breakdown of the market by technology, application, and geography, offering stakeholders a clear view of the opportunities and risks in the coming decade. As the world accelerates toward renewable energy targets, the solar junction box market is positioned for sustained development, supported by declining technology costs and strong corporate sustainability commitments.About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports. By leveraging comprehensive data sources and rigorous analytical methodologies, HDIN Research assists businesses in navigating complex industry landscapes and making informed strategic decisions.

Media Contact:

Company Name: HDIN Research

Website: www.hdinresearch.com

Email: sales@hdinresearch.com