Samyang Corporation Analysis: Pivoting to High-Value Specialty Materials and AI-Driven Bio-R&D

Date : 2026-01-28

Reading : 283

HDIN Research, an independent market consulting firm, has released a comprehensive analysis of Samyang Corporation's financial and strategic positioning based on its Q3 2025 report. The analysis reveals a conglomerate aggressively transitioning from traditional manufacturing to a technology-intensive powerhouse focused on "Specialty" materials, AI integration, and sustainable practices.

Figure Fueling Growth Samyang's R&D-Driven Transformation

2050 Carbon Neutrality: A Strategic Imperative

2050 Carbon Neutrality: A Strategic Imperative

Samyang Corporation has solidified its commitment to sustainability with a concrete "2050 Net Zero Roadmap." The company aims to reduce greenhouse gas emissions by 40% by 2030 (compared to the 2018 baseline) and mandates a 30% recycled plastic usage rate by the same year.

Key initiatives driving this transition include:

* Energy Transition: Expanding solar power facilities and converting boilers to LNG in subsidiaries like Samyang Packaging.

* Waste Heat Recovery: Implementing systems to utilize waste heat for industrial processes, reducing fossil fuel reliance.

* Circular Economy: Commercializing high-purity Recycled PET (R-Chip) via Samyang Eco-Tech and developing label-free, lightweight packaging to minimize waste at the source.

R&D Transformation: AI Meets Biology

A standout feature of Samyang's strategy is the integration of Artificial Intelligence (AI) into its R&D framework. The "Bioconvergence Research Institute" has established a specialized "Metabolic Pathway Design PG" utilizing AI algorithms to design microbial strains.

This "System Metabolic Engineering" approach enables:

* Molecular Design: Using AI to simulate thousands of metabolic pathways to optimize the production of high-value bio-materials.

* Cost Efficiency: Reducing the "sunk costs" of new material development by shortening R&D cycles.

* Product Innovation: Focusing on high-margin applications in food ingredients (Allulose), personal care, and pharmaceuticals.

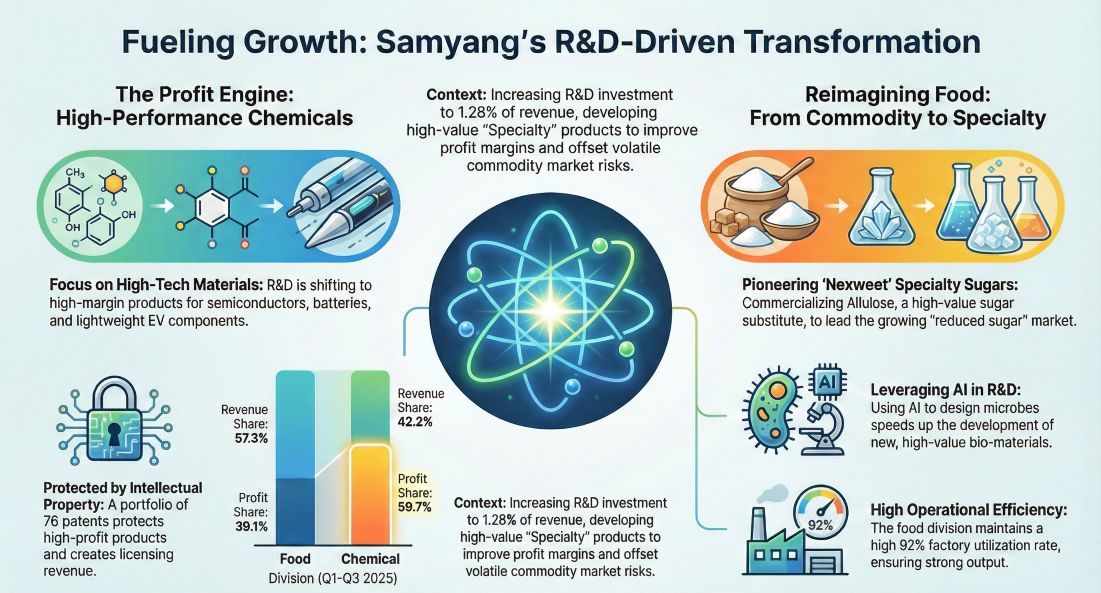

Specialty Materials: The New Profit Engine

The financial analysis indicates that R&D investment is reshaping Samyang's profit structure. Despite accounting for only 1.28% of revenue, R&D spending has enabled a shift toward high-margin specialty products.

* Chemical Sector: This division has become the group's profit driver, contributing nearly 60% of total divisional income. Key products include high-premium ion exchange resins for semiconductors and nuclear power, as well as lightweight composite materials for EVs.

* Food Sector: The company is moving away from commodity sugar to functional ingredients. Its "Nexweet" brand, featuring Allulose produced via proprietary enzyme technology, is leading the "sugar reduction" trend in Korea and expanding into global B2B and B2C markets.

Financial Health and Future Outlook

Financially, Samyang Corporation maintains a robust "AA-" credit rating with a stable debt structure. The company's operating profit margin of 5.16% is supported by high capacity utilization rates in both chemical (95%) and food (92%) sectors, driven by the strong demand for these new specialty products.

HDIN Research concludes that Samyang's heavy investment in green technology and AI-driven R&D is effectively offsetting the cyclical risks of raw material prices, positioning it for long-term valuation growth.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Contact: sales@hdinresearch.com

Website: www.hdinresearch.com

Figure Fueling Growth Samyang's R&D-Driven Transformation

2050 Carbon Neutrality: A Strategic ImperativeSamyang Corporation has solidified its commitment to sustainability with a concrete "2050 Net Zero Roadmap." The company aims to reduce greenhouse gas emissions by 40% by 2030 (compared to the 2018 baseline) and mandates a 30% recycled plastic usage rate by the same year.

Key initiatives driving this transition include:

* Energy Transition: Expanding solar power facilities and converting boilers to LNG in subsidiaries like Samyang Packaging.

* Waste Heat Recovery: Implementing systems to utilize waste heat for industrial processes, reducing fossil fuel reliance.

* Circular Economy: Commercializing high-purity Recycled PET (R-Chip) via Samyang Eco-Tech and developing label-free, lightweight packaging to minimize waste at the source.

R&D Transformation: AI Meets Biology

A standout feature of Samyang's strategy is the integration of Artificial Intelligence (AI) into its R&D framework. The "Bioconvergence Research Institute" has established a specialized "Metabolic Pathway Design PG" utilizing AI algorithms to design microbial strains.

This "System Metabolic Engineering" approach enables:

* Molecular Design: Using AI to simulate thousands of metabolic pathways to optimize the production of high-value bio-materials.

* Cost Efficiency: Reducing the "sunk costs" of new material development by shortening R&D cycles.

* Product Innovation: Focusing on high-margin applications in food ingredients (Allulose), personal care, and pharmaceuticals.

Specialty Materials: The New Profit Engine

The financial analysis indicates that R&D investment is reshaping Samyang's profit structure. Despite accounting for only 1.28% of revenue, R&D spending has enabled a shift toward high-margin specialty products.

* Chemical Sector: This division has become the group's profit driver, contributing nearly 60% of total divisional income. Key products include high-premium ion exchange resins for semiconductors and nuclear power, as well as lightweight composite materials for EVs.

* Food Sector: The company is moving away from commodity sugar to functional ingredients. Its "Nexweet" brand, featuring Allulose produced via proprietary enzyme technology, is leading the "sugar reduction" trend in Korea and expanding into global B2B and B2C markets.

Financial Health and Future Outlook

Financially, Samyang Corporation maintains a robust "AA-" credit rating with a stable debt structure. The company's operating profit margin of 5.16% is supported by high capacity utilization rates in both chemical (95%) and food (92%) sectors, driven by the strong demand for these new specialty products.

HDIN Research concludes that Samyang's heavy investment in green technology and AI-driven R&D is effectively offsetting the cyclical risks of raw material prices, positioning it for long-term valuation growth.

Please click to watch the YouTube video of the report presentation.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Contact: sales@hdinresearch.com

Website: www.hdinresearch.com