Global Industrial Gas Market Analysis: Strategic Pivots and the Rise of High-Value Segments

Date : 2026-02-24

Reading : 737

In 2025, the industrial gas industry, often referred to as the blood of modern industry, is undergoing a profound transformation. Market data from the first three quarters of 2025 reveals a dual-track growth pattern where global giants are pivoting toward high-margin technology segments while regional players in Asia are accelerating their presence through integrated service models.

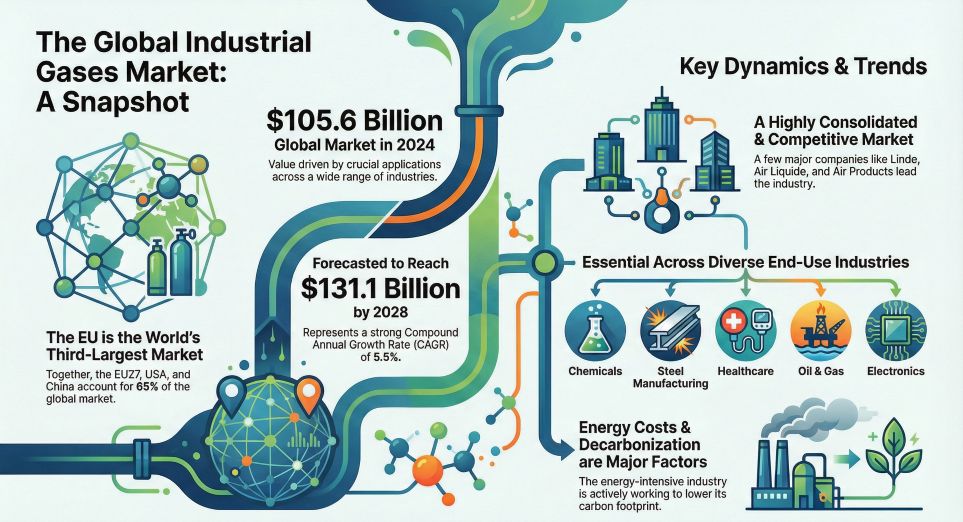

Figure Global Industrial Gases Outlook

The global market remains characterized by a high degree of oligopoly, with the top three players—Linde, Air Liquide, and Air Products—controlling approximately 70 percent of the total market value. However, the focus of these leaders has shifted from traditional volume expansion to high-value areas such as electronics materials, medical gases, and green hydrogen.

The global market remains characterized by a high degree of oligopoly, with the top three players—Linde, Air Liquide, and Air Products—controlling approximately 70 percent of the total market value. However, the focus of these leaders has shifted from traditional volume expansion to high-value areas such as electronics materials, medical gases, and green hydrogen.

Linde Plc reported strong financial resilience in the first nine months of 2025, with sales reaching 25.22 billion USD and an adjusted operating margin of 29.7 percent. This performance was driven by disciplined pricing management and a robust project backlog of approximately 10 billion USD. Similarly, Air Liquide is executing its ADVANCE strategy, investing heavily in the semiconductor hubs of Dresden, Singapore, and the United States. Its revenue for the same period stood at 20.32 billion EUR, with a significant 3.5 percent comparable growth in the Americas.

While global giants maintain their grip on developed markets, domestic leaders in China and India are leveraging localized advantages and faster construction cycles. Chinese firms such as Hangyang and JinHong Gas are utilizing an equipment + gas integrated model to break into the semiconductor supply chain. Hangyang reported a 10.39 percent increase in revenue for the first three quarters of 2025, reaching 11.43 billion RMB, as its gas service business now accounts for over 60 percent of its total revenue.

The competitive landscape is being reshaped by the AI boom, which has triggered a surge in demand for ultra-high-purity carrier gases and precursor materials required for advanced chip nodes. Additionally, the global drive toward decarbonization is positioning hydrogen as a core strategic pillar, with billions of euros being funneled into green and blue hydrogen projects.

Despite positive growth, the industry faces significant challenges. Electricity remains the single largest cost for atmospheric gas production, often exceeding 70 percent of total production costs. While giants use energy pass-through clauses in long-term contracts to mitigate risk, smaller merchant suppliers are more vulnerable to price spikes. Geopolitical tensions and supply chain fragmentation also pose risks to the procurement of rare gases like Helium and Neon.

Table Market Summary: Key Players Performance and Strategy (2025)

Conclusion

The industrial gas sector in 2025 is at a crossroads between traditional industrial support and high-tech material solutions. The shift toward TGCM (Total Gas and Chemical Management) services indicates that the most successful firms are moving beyond being commodity suppliers to becoming essential partners in their customers production processes. For enterprise clients and investors, the key winners will be those that can secure stable cash flows through long-term contracts while successfully navigating the technological requirements of the advanced semiconductor and green energy sectors.

Company Name: HDIN Research

Company Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Official Website: www.hdinresearch.com

Contact Email: sales@hdinresearch.com

Figure Global Industrial Gases Outlook

The global market remains characterized by a high degree of oligopoly, with the top three players—Linde, Air Liquide, and Air Products—controlling approximately 70 percent of the total market value. However, the focus of these leaders has shifted from traditional volume expansion to high-value areas such as electronics materials, medical gases, and green hydrogen.Linde Plc reported strong financial resilience in the first nine months of 2025, with sales reaching 25.22 billion USD and an adjusted operating margin of 29.7 percent. This performance was driven by disciplined pricing management and a robust project backlog of approximately 10 billion USD. Similarly, Air Liquide is executing its ADVANCE strategy, investing heavily in the semiconductor hubs of Dresden, Singapore, and the United States. Its revenue for the same period stood at 20.32 billion EUR, with a significant 3.5 percent comparable growth in the Americas.

While global giants maintain their grip on developed markets, domestic leaders in China and India are leveraging localized advantages and faster construction cycles. Chinese firms such as Hangyang and JinHong Gas are utilizing an equipment + gas integrated model to break into the semiconductor supply chain. Hangyang reported a 10.39 percent increase in revenue for the first three quarters of 2025, reaching 11.43 billion RMB, as its gas service business now accounts for over 60 percent of its total revenue.

The competitive landscape is being reshaped by the AI boom, which has triggered a surge in demand for ultra-high-purity carrier gases and precursor materials required for advanced chip nodes. Additionally, the global drive toward decarbonization is positioning hydrogen as a core strategic pillar, with billions of euros being funneled into green and blue hydrogen projects.

Despite positive growth, the industry faces significant challenges. Electricity remains the single largest cost for atmospheric gas production, often exceeding 70 percent of total production costs. While giants use energy pass-through clauses in long-term contracts to mitigate risk, smaller merchant suppliers are more vulnerable to price spikes. Geopolitical tensions and supply chain fragmentation also pose risks to the procurement of rare gases like Helium and Neon.

Table Market Summary: Key Players Performance and Strategy (2025)

| Company Name | 9M 2025 Revenue/Status | Operating Margin/Profitability | Strategic Focus |

|---|---|---|---|

| Linde Plc | 25.22 Billion USD | 29.7% (Adjusted) | Clean energy projects and electronic bulk gases |

| Air Liquide | 20.31 Billion EUR | 22.0% (H1 G&S) | ADVANCE plan; semiconductor carrier gases |

| Air Products | 120.37 Billion USD (FY) | 26.2% (Adjusted) | Core industrial gas; hydrogen (NEOM project) |

| Hangyang Group | 11.43 Billion RMB | 21.18% (H1 Gas Margin) | Equipment + gas model; rare gas indigenization |

| Jinhong Gas | 2.03 Billion RMB | 30.2% (H1 Gross Margin) | Electronic specialty gases; overseas M&A |

| Nippon Sanso | 1.31 Trillion JPY (FYE) | 23.3% (EBITDA) | NS Vision 2026; expanding global electronics |

Conclusion

The industrial gas sector in 2025 is at a crossroads between traditional industrial support and high-tech material solutions. The shift toward TGCM (Total Gas and Chemical Management) services indicates that the most successful firms are moving beyond being commodity suppliers to becoming essential partners in their customers production processes. For enterprise clients and investors, the key winners will be those that can secure stable cash flows through long-term contracts while successfully navigating the technological requirements of the advanced semiconductor and green energy sectors.

Company Name: HDIN Research

Company Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Official Website: www.hdinresearch.com

Contact Email: sales@hdinresearch.com