Global Polysilicon Industry Navigates Cyclical Bottoms and Geopolitical Reshuffling: HDIN Research Strategic Analysis

Date : 2026-03-05

Reading : 765

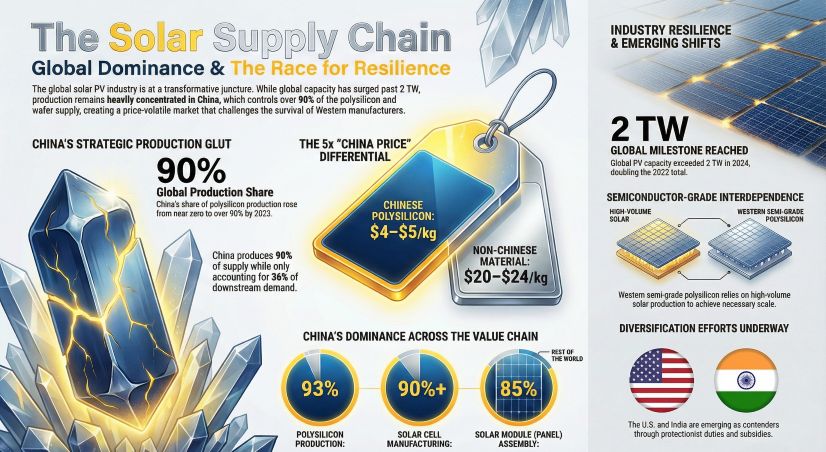

The global polysilicon and photovoltaic (PV) industry is currently navigating a complex intersection of a cyclical market bottom and a significant technological pivot. According to recent market intelligence from HDIN Research, while cumulative global PV installations surpassed the 2TW milestone by the end of 2024, the upstream polysilicon sector is facing unprecedented oversupply and geopolitical pressure.

Figure The Solar Supply Chain

Market Dynamics: Oversupply and the N-Type Transition

Market Dynamics: Oversupply and the N-Type Transition

The industry enters 2026 with a severe supply-demand imbalance. Global module production capacity reached 1.5TW per year, far exceeding annual deployment rates. This has led to high inventory levels, with polysilicon stocks at factories estimated at 330,000 tons in early 2026. Consequently, market prices have dropped below the average cost line, reaching lows of approximately 34,700 RMB per ton (including tax), pushing many manufacturers into a loss-making phase.

Despite these challenges, a structural shift toward N-type technology (such as TOPCon and HJT) offers a silver lining. N-type modules now account for 75 percent of the market share. This transition has created a premium for high-purity N-type silicon and dense materials. Furthermore, low-carbon footprint products, such as Fluidized Bed Reactor (FBR) granular silicon, are gaining a green premium in international trade due to policies like the EU's Carbon Border Adjustment Mechanism (CBAM).

Geopolitical Influence and Trade Barriers

Geopolitics is actively reshaping the global supply chain. The United States is considering a Section 232 national security investigation into polysilicon, which could result in a Tariff-Rate Quota (TRQ) system with duties exceeding 100 percent for out-of-quota products. US trade policy is also shifting from origin-based scrutiny to ownership-based review, targeting Chinese-invested production even in Southeast Asia.

Domestically, a major policy shift in China is set to impact global pricing. Starting April 2026, the cancellation of export tax rebates for PV products will increase costs by approximately 9 percent. This is expected to squeeze profit margins for exporters and potentially drive up international prices as manufacturers attempt to transfer these costs to overseas buyers.

The Silicon Base for Future Computing and Space Infrastructure

The demand for polysilicon is extending beyond traditional energy applications. The rise of AI, 5G, and advanced data centers is driving the market for semiconductor-grade silicon (11N purity). High-purity silicon is also essential for space-based computing and satellite networks, such as Elon Musk's Starlink. These applications require extreme radiation resistance and reliability, necessitating a move toward 11N-13N grade electronic silicon. This high-end segment is expected to reach 18.3 billion USD in revenue by 2029.

Strategic Table: Global Polysilicon Industry Key Metrics and Outlook

Corporate Strategies and Regional Positioning

Industry leaders are adopting distinct survival strategies. Tongwei continues to leverage its massive scale (over 900,000 tons capacity) to maintain a vertically integrated cost advantage. GCL Tech is doubling down on its granular silicon technology to capture the green premium in high-end markets. Meanwhile, international firms like Wacker Chemie are pivoting toward the specialties strategy, focusing on ultra-pure semiconductor-grade silicon to avoid the price wars of the solar-grade market.

In the United States, despite the Inflation Reduction Act (IRA) offering subsidies of 3 USD per kg for polysilicon, domestic capacity remains limited at around 50,000 tons, which is insufficient to meet the 50GW+ domestic demand. This gap forces a continued reliance on imports while local production ramps up under high protective barriers.

Analyst Recommendations

For enterprises and government agencies, the focus must shift from pure volume to technological reliability and carbon transparency. HDIN Research suggests that manufacturers accelerate their overseas expansion into regions like the Middle East or North America to mitigate trade risks. Furthermore, the convergence of AI, space technology, and PV energy suggests that the high-purity silicon segment will become a vital strategic asset in the next decade.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure The Solar Supply Chain

Market Dynamics: Oversupply and the N-Type TransitionThe industry enters 2026 with a severe supply-demand imbalance. Global module production capacity reached 1.5TW per year, far exceeding annual deployment rates. This has led to high inventory levels, with polysilicon stocks at factories estimated at 330,000 tons in early 2026. Consequently, market prices have dropped below the average cost line, reaching lows of approximately 34,700 RMB per ton (including tax), pushing many manufacturers into a loss-making phase.

Despite these challenges, a structural shift toward N-type technology (such as TOPCon and HJT) offers a silver lining. N-type modules now account for 75 percent of the market share. This transition has created a premium for high-purity N-type silicon and dense materials. Furthermore, low-carbon footprint products, such as Fluidized Bed Reactor (FBR) granular silicon, are gaining a green premium in international trade due to policies like the EU's Carbon Border Adjustment Mechanism (CBAM).

Geopolitical Influence and Trade Barriers

Geopolitics is actively reshaping the global supply chain. The United States is considering a Section 232 national security investigation into polysilicon, which could result in a Tariff-Rate Quota (TRQ) system with duties exceeding 100 percent for out-of-quota products. US trade policy is also shifting from origin-based scrutiny to ownership-based review, targeting Chinese-invested production even in Southeast Asia.

Domestically, a major policy shift in China is set to impact global pricing. Starting April 2026, the cancellation of export tax rebates for PV products will increase costs by approximately 9 percent. This is expected to squeeze profit margins for exporters and potentially drive up international prices as manufacturers attempt to transfer these costs to overseas buyers.

The Silicon Base for Future Computing and Space Infrastructure

The demand for polysilicon is extending beyond traditional energy applications. The rise of AI, 5G, and advanced data centers is driving the market for semiconductor-grade silicon (11N purity). High-purity silicon is also essential for space-based computing and satellite networks, such as Elon Musk's Starlink. These applications require extreme radiation resistance and reliability, necessitating a move toward 11N-13N grade electronic silicon. This high-end segment is expected to reach 18.3 billion USD in revenue by 2029.

Strategic Table: Global Polysilicon Industry Key Metrics and Outlook

| Key Indicator | Data and Trend Analysis |

|---|---|

| 2024 Global PV Installation | Surpassed 2 TW cumulative installed capacity |

| N-Type Technology Share | 75% of total market |

| Polysilicon Inventory (2026) | Approximately 330,000 tons |

| China Polysilicon Capacity | 93% global share (2.1 million tons) |

| Export Tax Rebate Change | 9% cost increase (effective April 2026) |

| US Section 232 Impact | Potential 100%+ tariffs on excess imports |

| Electronic Grade Silicon Value | Projected USD 18.3 billion by 2029 |

| Granular Silicon Advantage | 41 kg CO₂e/kg carbon footprint vs. 81 kg for standard |

Corporate Strategies and Regional Positioning

Industry leaders are adopting distinct survival strategies. Tongwei continues to leverage its massive scale (over 900,000 tons capacity) to maintain a vertically integrated cost advantage. GCL Tech is doubling down on its granular silicon technology to capture the green premium in high-end markets. Meanwhile, international firms like Wacker Chemie are pivoting toward the specialties strategy, focusing on ultra-pure semiconductor-grade silicon to avoid the price wars of the solar-grade market.

In the United States, despite the Inflation Reduction Act (IRA) offering subsidies of 3 USD per kg for polysilicon, domestic capacity remains limited at around 50,000 tons, which is insufficient to meet the 50GW+ domestic demand. This gap forces a continued reliance on imports while local production ramps up under high protective barriers.

Analyst Recommendations

For enterprises and government agencies, the focus must shift from pure volume to technological reliability and carbon transparency. HDIN Research suggests that manufacturers accelerate their overseas expansion into regions like the Middle East or North America to mitigate trade risks. Furthermore, the convergence of AI, space technology, and PV energy suggests that the high-purity silicon segment will become a vital strategic asset in the next decade.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com