Entegris 2025 Deep Dive: The 2nm Yield Gatekeeper & Financial Pivot

Date : 2026-02-17

Reading : 427

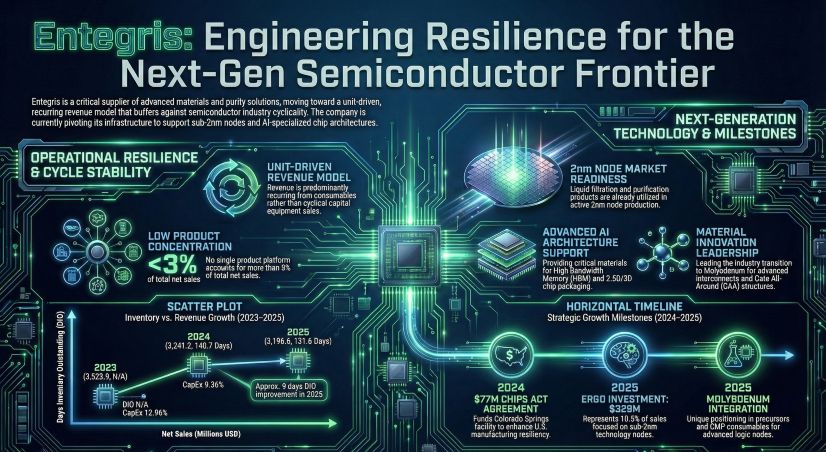

While Entegris (ENTG) reported a slight revenue contraction of 1% to $3.19 billion in FY2025, the headline numbers obscure a critical transformation in the semiconductor supply chain. The "So What" for investors and industry observers is not the cyclical revenue pause, but the structural increase in Content per Wafer driven by the transition to 2nm process nodes and High Bandwidth Memory (HBM). As the industry moves toward Gate-All-Around (GAA) architectures, Entegris is evolving from a materials supplier into a critical "Yield Insurance" provider, where its micro-contamination control becomes the primary defense against yield loss in increasingly complex fabrication environments.

Figure Entegrig Engineering Resilience for the Next-Gen Semiconductor Frontier

Financial Resilience: Unlocking "Accounting Alpha"

Financial Resilience: Unlocking "Accounting Alpha"

The FY2025 financial landscape for Entegris was characterized by high depreciation expenses and restructuring efforts, which compressed gross margins to 44.4%. However, a detailed accounting analysis reveals a significant profitability lever for FY2026.

Starting in early 2026, Entegris implemented a strategic adjustment to the estimated useful lives of its manufacturing equipment (extending from 5-10 years to 5-14 years). HDIN Research analysis indicates this change is projected to reduce depreciation expenses by approximately $72.9 million in 2026. Consequently, this creates a direct "accounting alpha," potentially boosting gross profit by an estimated $52.4 million without a requisite increase in sales volume.

Furthermore, the company’s capital allocation strategy remains disciplined. Despite a high leverage profile following the CMC Materials acquisition, Entegris paid down $300 million in debt in FY2025, bringing total debt to $3.75 billion. With $695 million in operating cash flow, the company retains sufficient liquidity to service debt while funding the $250 million CapEx projected for 2026.

The 2nm Imperative: Why Material Purity Wins

The strategic moat for Entegris is deepening as chipmakers approach the 2nm frontier. At these angstrom-level dimensions, the introduction of new interconnect materials, such as Molybdenum, requires highly specific deposition and etching chemistries.

* Unit-Driven Growth: Unlike capital equipment suppliers who rely on fab expansions, Entegris’s revenue is "unit-driven." Every wafer processed at 2nm requires significantly more filtration, CMP consumables, and advanced precursors than legacy nodes.

* Yield Protection: With the Materials Solutions (MS) and Advanced Purity Solutions (APS) divisions working in tandem, Entegris has locked itself into the technical roadmaps of major foundries. The company’s 2nm liquid filtration solutions are already in production, directly addressing the "Time to Yield" challenges that define profitability for chipmakers.

* AI & HBM Tailwinds: The explosion in AI workloads has created a secondary growth engine. High Bandwidth Memory (HBM) requires complex vertical stacking, driving demand for Entegris’s CMP slurries and cleaning chemistries.

Risk Radar: Geopolitics and Concentration

Despite the technological upside, the risk profile remains elevated due to supply chain concentration.

* China Exposure: China accounted for 21% of FY2025 net sales. With expanding U.S. export controls and China’s push for localized supply chains, this revenue stream faces long-term structural pressure.

* Customer Dependency: TSMC represents 16% of net sales. While this validates Entegris’s technology leadership, it also exposes the company to the specific capex cycles of a single dominant player.

* Asset Divestiture: The completed divestiture of the Pipeline and Industrial Materials (PIM) business for $263 million signals a clear strategy: shedding non-core assets to focus entirely on the high-margin semiconductor ecosystem.

HDIN Viewpoint: The "Yield Insurance" Premium

At HDIN Research, we believe the market is currently underappreciating the "stickiness" of Entegris’s portfolio. In the 2nm era, purity is no longer a commodity; it is a barrier to entry.

While the DuPont Analysis shows a dip in ROE to roughly 6% due to margin compression and asset turnover declines, we view this as a temporary trough. The combination of the 2026 depreciation accounting benefit, the ramp-up of the Colorado Springs facility (backed by $77 million in CHIPS Act funding), and the stabilizing inventory cycles suggests a margin recovery is imminent. Entegris is effectively positioning itself as a high-beta play on semiconductor complexity, offering "Yield Insurance" that chipmakers cannot afford to forego.

Presentation Download

For a comprehensive breakdown of the financial models, DuPont analysis, and 2nm strategic roadmap discussed in this article, please access the full report presentation.

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Entegrig Engineering Resilience for the Next-Gen Semiconductor Frontier

Financial Resilience: Unlocking "Accounting Alpha"The FY2025 financial landscape for Entegris was characterized by high depreciation expenses and restructuring efforts, which compressed gross margins to 44.4%. However, a detailed accounting analysis reveals a significant profitability lever for FY2026.

Starting in early 2026, Entegris implemented a strategic adjustment to the estimated useful lives of its manufacturing equipment (extending from 5-10 years to 5-14 years). HDIN Research analysis indicates this change is projected to reduce depreciation expenses by approximately $72.9 million in 2026. Consequently, this creates a direct "accounting alpha," potentially boosting gross profit by an estimated $52.4 million without a requisite increase in sales volume.

Furthermore, the company’s capital allocation strategy remains disciplined. Despite a high leverage profile following the CMC Materials acquisition, Entegris paid down $300 million in debt in FY2025, bringing total debt to $3.75 billion. With $695 million in operating cash flow, the company retains sufficient liquidity to service debt while funding the $250 million CapEx projected for 2026.

The 2nm Imperative: Why Material Purity Wins

The strategic moat for Entegris is deepening as chipmakers approach the 2nm frontier. At these angstrom-level dimensions, the introduction of new interconnect materials, such as Molybdenum, requires highly specific deposition and etching chemistries.

* Unit-Driven Growth: Unlike capital equipment suppliers who rely on fab expansions, Entegris’s revenue is "unit-driven." Every wafer processed at 2nm requires significantly more filtration, CMP consumables, and advanced precursors than legacy nodes.

* Yield Protection: With the Materials Solutions (MS) and Advanced Purity Solutions (APS) divisions working in tandem, Entegris has locked itself into the technical roadmaps of major foundries. The company’s 2nm liquid filtration solutions are already in production, directly addressing the "Time to Yield" challenges that define profitability for chipmakers.

* AI & HBM Tailwinds: The explosion in AI workloads has created a secondary growth engine. High Bandwidth Memory (HBM) requires complex vertical stacking, driving demand for Entegris’s CMP slurries and cleaning chemistries.

Risk Radar: Geopolitics and Concentration

Despite the technological upside, the risk profile remains elevated due to supply chain concentration.

* China Exposure: China accounted for 21% of FY2025 net sales. With expanding U.S. export controls and China’s push for localized supply chains, this revenue stream faces long-term structural pressure.

* Customer Dependency: TSMC represents 16% of net sales. While this validates Entegris’s technology leadership, it also exposes the company to the specific capex cycles of a single dominant player.

* Asset Divestiture: The completed divestiture of the Pipeline and Industrial Materials (PIM) business for $263 million signals a clear strategy: shedding non-core assets to focus entirely on the high-margin semiconductor ecosystem.

HDIN Viewpoint: The "Yield Insurance" Premium

At HDIN Research, we believe the market is currently underappreciating the "stickiness" of Entegris’s portfolio. In the 2nm era, purity is no longer a commodity; it is a barrier to entry.

While the DuPont Analysis shows a dip in ROE to roughly 6% due to margin compression and asset turnover declines, we view this as a temporary trough. The combination of the 2026 depreciation accounting benefit, the ramp-up of the Colorado Springs facility (backed by $77 million in CHIPS Act funding), and the stabilizing inventory cycles suggests a margin recovery is imminent. Entegris is effectively positioning itself as a high-beta play on semiconductor complexity, offering "Yield Insurance" that chipmakers cannot afford to forego.

Presentation Download

For a comprehensive breakdown of the financial models, DuPont analysis, and 2nm strategic roadmap discussed in this article, please access the full report presentation.

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com