Kraft Heinz vs. UTZ 2025 Analysis: The Strategic Divergence of Price vs. Volume

Date : 2026-02-18

Reading : 501

The 2025 fiscal year reveals a sharp strategic bifurcation in the packaged food sector. While Kraft Heinz (KHC) retreats into a defensive crouch—sacrificing volume to protect margins via price hikes—Utz Brands (UTZ) is executing an aggressive "land grab," leveraging negative net pricing to drive volume growth in a hyper-promotional environment. This analysis unpacks the financial realities behind KHC’s massive impairment charges and Utz’s leveraged expansion.

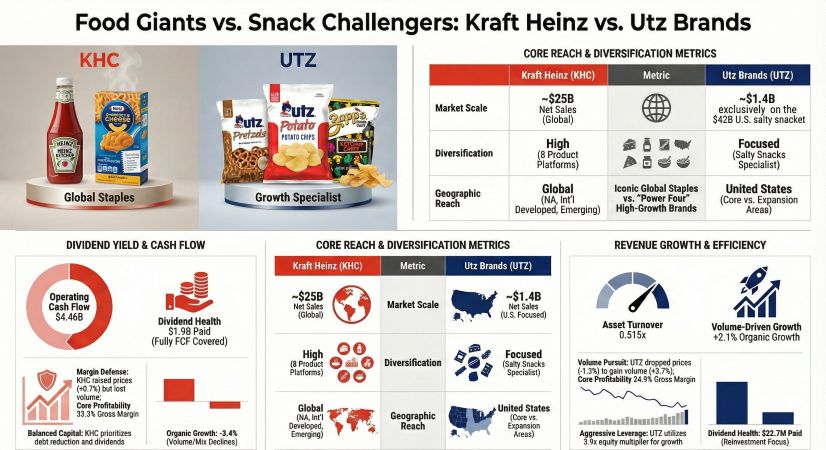

Figure Food Giants vs Snack Challengers Kraft Heinz vs Utz Brands

Financial Structures: The "Accounting Mirage" vs. Leveraged Growth

Financial Structures: The "Accounting Mirage" vs. Leveraged Growth

A superficial glance at the 2025 financials paints a misleading picture. KHC reported a negative Return on Equity (ROE) of -14.0%, while Utz posted a positive, albeit thin, ROE. However, HDIN Research’s forensic analysis reveals the deeper capital dynamics at play.

* KHC’s Value Trap or Opportunity? KHC’s net loss is largely an accounting artifact driven by a colossal $9.3 billion non-cash impairment charge against goodwill and intangible assets. When stripped of this noise, KHC remains a cash-generating machine, producing $4.46 billion in Operating Cash Flow. The "So What" for investors is that the company’s ability to cover its dividend remains intact, making this a narrative of valuation repair rather than insolvency.

* Utz’s Leverage Engine: Conversely, Utz’s returns are structurally driven by high financial leverage (Equity Multiplier of 3.91x) and superior asset turnover (0.515x compared to KHC’s 0.305x). While Utz is profitable on paper, its Free Cash Flow (FCF) conversion is weak—only $9.4 million FCF against $112.2 million in operating cash flow—due to heavy Capital Expenditures ($102.8 million) required to modernize its manufacturing footprint.

The Core Conflict: Pricing Power vs. Market Share

The most critical divergence lies in how each company navigated the inflationary environment of 2025.

Kraft Heinz: The Defensive Price Hikes

KHC prioritized gross margin protection over market share. The company achieved a 0.7% price increase but suffered a 4.1% decline in Volume/Mix. In North America, the trade-off was even more severe, with volume dropping 5.0%. Management explicitly acknowledged that these pricing actions have eroded market share, particularly as retailers like Walmart exert pressure for rollbacks. KHC is effectively shrinking its footprint to maintain profitability.

Utz Brands: The Offensive Volume Play

Utz flipped the script. In a sector facing volume headwinds, Utz delivered a 3.7% increase in Volume/Mix, driven by a 1.3% decline in Net Price Realization. By increasing promotional activity in a price-sensitive market, Utz is actively taking shelf space from competitors. This strategy is proving highly effective in "Expansion Geographies," where retail sales surged 7.8%, validating their counter-cyclical approach to pricing.

Operational Moats: AI Efficiency vs. The DSD Advantage

Both companies are digging deep moats, but with different tools.

* KHC’s Tech Pivot: Facing supply chain rigidities, KHC is banking on "Agile Pods" and AI solutions (like the KHAI assistant) to drive productivity. The goal is to offset the "unfavorable cost leverage" caused by declining volumes through internal efficiencies rather than commercial expansion.

* Utz’s Distribution Fortress: Utz’s competitive advantage remains its Direct Store Delivery (DSD) network, comprising approximately 2,500 routes. This high-touch model allows Utz to execute store-level merchandising and inventory management with a precision that warehouse-delivered competitors cannot match. This infrastructure is the backbone supporting their expansion into new territories like California and the Midwest.

HDIN Viewpoint

At HDIN Research, we classify these two entities into distinct investment narratives based on the 2025 data.

Our Institutional Perspective:

1. KHC is a "Value Repair" Story: The market has priced in the $9.3 billion impairment. The real risk for KHC is not the balance sheet, but the limits of pricing power. With organic sales down 3.4%, the company must transition from price-led growth to volume stabilization, or risk permanent brand erosion in the face of private label competition.

2. Utz is a "Share Reaper": Utz is correctly identifying the current cycle as a land-grab opportunity. By sacrificing short-term pricing for long-term customer acquisition, they are building a larger base for future monetization. However, the risk lies in their liquidity; with FCF tight and net leverage around 3.4x-3.6x, execution on their productivity initiatives is non-negotiable.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Food Giants vs Snack Challengers Kraft Heinz vs Utz Brands

Financial Structures: The "Accounting Mirage" vs. Leveraged GrowthA superficial glance at the 2025 financials paints a misleading picture. KHC reported a negative Return on Equity (ROE) of -14.0%, while Utz posted a positive, albeit thin, ROE. However, HDIN Research’s forensic analysis reveals the deeper capital dynamics at play.

* KHC’s Value Trap or Opportunity? KHC’s net loss is largely an accounting artifact driven by a colossal $9.3 billion non-cash impairment charge against goodwill and intangible assets. When stripped of this noise, KHC remains a cash-generating machine, producing $4.46 billion in Operating Cash Flow. The "So What" for investors is that the company’s ability to cover its dividend remains intact, making this a narrative of valuation repair rather than insolvency.

* Utz’s Leverage Engine: Conversely, Utz’s returns are structurally driven by high financial leverage (Equity Multiplier of 3.91x) and superior asset turnover (0.515x compared to KHC’s 0.305x). While Utz is profitable on paper, its Free Cash Flow (FCF) conversion is weak—only $9.4 million FCF against $112.2 million in operating cash flow—due to heavy Capital Expenditures ($102.8 million) required to modernize its manufacturing footprint.

The Core Conflict: Pricing Power vs. Market Share

The most critical divergence lies in how each company navigated the inflationary environment of 2025.

Kraft Heinz: The Defensive Price Hikes

KHC prioritized gross margin protection over market share. The company achieved a 0.7% price increase but suffered a 4.1% decline in Volume/Mix. In North America, the trade-off was even more severe, with volume dropping 5.0%. Management explicitly acknowledged that these pricing actions have eroded market share, particularly as retailers like Walmart exert pressure for rollbacks. KHC is effectively shrinking its footprint to maintain profitability.

Utz Brands: The Offensive Volume Play

Utz flipped the script. In a sector facing volume headwinds, Utz delivered a 3.7% increase in Volume/Mix, driven by a 1.3% decline in Net Price Realization. By increasing promotional activity in a price-sensitive market, Utz is actively taking shelf space from competitors. This strategy is proving highly effective in "Expansion Geographies," where retail sales surged 7.8%, validating their counter-cyclical approach to pricing.

Operational Moats: AI Efficiency vs. The DSD Advantage

Both companies are digging deep moats, but with different tools.

* KHC’s Tech Pivot: Facing supply chain rigidities, KHC is banking on "Agile Pods" and AI solutions (like the KHAI assistant) to drive productivity. The goal is to offset the "unfavorable cost leverage" caused by declining volumes through internal efficiencies rather than commercial expansion.

* Utz’s Distribution Fortress: Utz’s competitive advantage remains its Direct Store Delivery (DSD) network, comprising approximately 2,500 routes. This high-touch model allows Utz to execute store-level merchandising and inventory management with a precision that warehouse-delivered competitors cannot match. This infrastructure is the backbone supporting their expansion into new territories like California and the Midwest.

HDIN Viewpoint

At HDIN Research, we classify these two entities into distinct investment narratives based on the 2025 data.

Our Institutional Perspective:

1. KHC is a "Value Repair" Story: The market has priced in the $9.3 billion impairment. The real risk for KHC is not the balance sheet, but the limits of pricing power. With organic sales down 3.4%, the company must transition from price-led growth to volume stabilization, or risk permanent brand erosion in the face of private label competition.

2. Utz is a "Share Reaper": Utz is correctly identifying the current cycle as a land-grab opportunity. By sacrificing short-term pricing for long-term customer acquisition, they are building a larger base for future monetization. However, the risk lies in their liquidity; with FCF tight and net leverage around 3.4x-3.6x, execution on their productivity initiatives is non-negotiable.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com