Carl Zeiss Meditec Sacrifices Short-Term Margins to Build a 50% Recurring Revenue Moat

Date : 2026-02-21

Reading : 245

In the current medical technology landscape, where high interest rates are stifling hospital capital expenditure, Carl Zeiss Meditec (AFX) is executing a high-stakes transformation. HDIN Research’s deep dive into the FY2024/25 financial filings reveals that the company is decisively moving away from a pure "heavy equipment" sales model. By accepting a temporary compression in net income, Zeiss is buying its way into a "Razor-and-Blade" ecosystem that is far more resilient to global economic volatility.

Figure ZEISS Meditec 202425 The Medical Device Growth Model

The "So What": Structuring for Resilience Over Immediate Profit

The "So What": Structuring for Resilience Over Immediate Profit

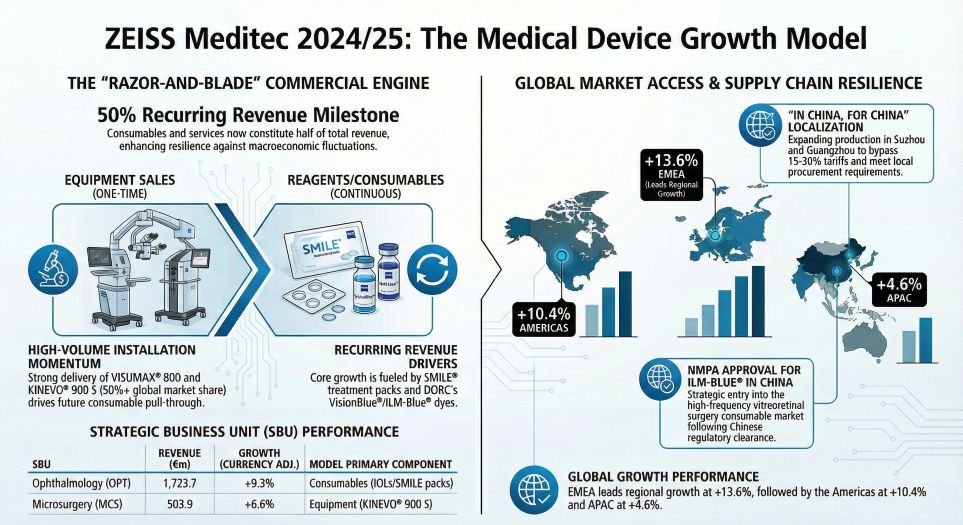

While the headline revenue growth of 7.8% (reaching €2.23 billion) signals stability, the strategic story lies in the margin compression. EBITA margins dipped to 11.6%, and Earnings Per Share (EPS) fell from €2.01 to €1.61.

However, this is not a sign of operational failure, but of strategic capital allocation. The acquisition of DORC (Dutch Ophthalmic Research Center) has fundamentally altered the company’s revenue quality. By integrating DORC’s retina surgical disposables (such as the EVA NEXUS platform and proprietary dyes), Zeiss has pushed its recurring revenue share to approximately 50%.

This is a critical defensive maneuver. In a market where hospitals are delaying purchases of expensive microscopes due to financing costs, Zeiss is securing a steady stream of consumable income that is "procedure-dependent" rather than "budget-dependent."

China Strategy: The "High-Low" Hedge Against VBP

The Asia-Pacific region remains the company's growth engine, contributing 44.5% of total revenue. However, the Chinese market presents a dual threat: Volume-Based Procurement (VBP) eroding unit prices, and aggressive geopolitical tariffs (ranging from 15% to 30%) impacting cross-border margins.

HDIN Research identifies a two-pronged "High-Low" strategy Zeiss is employing to counter these headwinds:

* The Volume Game: While VBP crushes margins on standard consumables, Zeiss is using its localized manufacturing ("In China, for China") to maintain volume leadership and dilute fixed costs.

* The Premium Defense: To protect profitability, the company is aggressively pushing Premium Intraocular Lenses (IOLs) and the new VISUMAX® 800 refractive laser system. These high-end segments largely sit outside the most punishing VBP tiers, allowing Zeiss to maintain a pricing premium based on clinical outcomes rather than commoditized specs.

Financial Health: The Cost of the Moat

The transformation has come with a price tag. For the first time, Zeiss Meditec is in a net debt position, driven by the €985 million+ capital deployment for DORC. The resulting interest expenses on internal loans (approx. €400 million at 3.66%) and Purchase Price Allocation (PPA) amortization are currently weighing on the Return on Equity (ROE), which has adjusted to ~6.6%.

Despite these pressures, the company’s structural integrity remains robust with an equity ratio of 62.5% and free cash flow rebounding to €203 million. This suggests that the leverage is a calculated, temporary bridge to a more profitable future state.

HDIN Viewpoint: From Hardware to "Digital Workflow"

At HDIN Research, we view FY2025 as a transition year that masks the long-term potential of the Zeiss portfolio. The market is underestimating the value of the ZEISS Workflows initiative. By connecting diagnosis, surgery, and follow-up through a unified digital ecosystem, Zeiss is increasing the "switching costs" for clinics.

The risk profile has shifted from "market demand" to "execution." The company’s ability to integrate DORC’s sales force and navigate the complex US-China tariff landscape without further margin erosion will determine if the EBITA margin can return to the targeted 16-20% range in the medium term.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure ZEISS Meditec 202425 The Medical Device Growth Model

The "So What": Structuring for Resilience Over Immediate ProfitWhile the headline revenue growth of 7.8% (reaching €2.23 billion) signals stability, the strategic story lies in the margin compression. EBITA margins dipped to 11.6%, and Earnings Per Share (EPS) fell from €2.01 to €1.61.

However, this is not a sign of operational failure, but of strategic capital allocation. The acquisition of DORC (Dutch Ophthalmic Research Center) has fundamentally altered the company’s revenue quality. By integrating DORC’s retina surgical disposables (such as the EVA NEXUS platform and proprietary dyes), Zeiss has pushed its recurring revenue share to approximately 50%.

This is a critical defensive maneuver. In a market where hospitals are delaying purchases of expensive microscopes due to financing costs, Zeiss is securing a steady stream of consumable income that is "procedure-dependent" rather than "budget-dependent."

China Strategy: The "High-Low" Hedge Against VBP

The Asia-Pacific region remains the company's growth engine, contributing 44.5% of total revenue. However, the Chinese market presents a dual threat: Volume-Based Procurement (VBP) eroding unit prices, and aggressive geopolitical tariffs (ranging from 15% to 30%) impacting cross-border margins.

HDIN Research identifies a two-pronged "High-Low" strategy Zeiss is employing to counter these headwinds:

* The Volume Game: While VBP crushes margins on standard consumables, Zeiss is using its localized manufacturing ("In China, for China") to maintain volume leadership and dilute fixed costs.

* The Premium Defense: To protect profitability, the company is aggressively pushing Premium Intraocular Lenses (IOLs) and the new VISUMAX® 800 refractive laser system. These high-end segments largely sit outside the most punishing VBP tiers, allowing Zeiss to maintain a pricing premium based on clinical outcomes rather than commoditized specs.

Financial Health: The Cost of the Moat

The transformation has come with a price tag. For the first time, Zeiss Meditec is in a net debt position, driven by the €985 million+ capital deployment for DORC. The resulting interest expenses on internal loans (approx. €400 million at 3.66%) and Purchase Price Allocation (PPA) amortization are currently weighing on the Return on Equity (ROE), which has adjusted to ~6.6%.

Despite these pressures, the company’s structural integrity remains robust with an equity ratio of 62.5% and free cash flow rebounding to €203 million. This suggests that the leverage is a calculated, temporary bridge to a more profitable future state.

HDIN Viewpoint: From Hardware to "Digital Workflow"

At HDIN Research, we view FY2025 as a transition year that masks the long-term potential of the Zeiss portfolio. The market is underestimating the value of the ZEISS Workflows initiative. By connecting diagnosis, surgery, and follow-up through a unified digital ecosystem, Zeiss is increasing the "switching costs" for clinics.

The risk profile has shifted from "market demand" to "execution." The company’s ability to integrate DORC’s sales force and navigate the complex US-China tariff landscape without further margin erosion will determine if the EBITA margin can return to the targeted 16-20% range in the medium term.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com