Ashland FY25 Analysis: Strategic Moats & Capital Efficiency

Date : 2026-02-22

Reading : 216

Ashland Inc.’s Fiscal Year 2025 results represent a calculated strategic reset rather than a simple cyclical contraction. While the headline $706 million non-cash goodwill impairment dominates the GAAP narrative, HDIN Research identifies a resilient core business where operational efficiency and a pivot toward high-margin Life Sciences are actively defending shareholder value against macro-economic headwinds.

Figure Ashland 2025 innovation in Every Drop

Financial Resilience: Beyond the Accounting Noise

Financial Resilience: Beyond the Accounting Noise

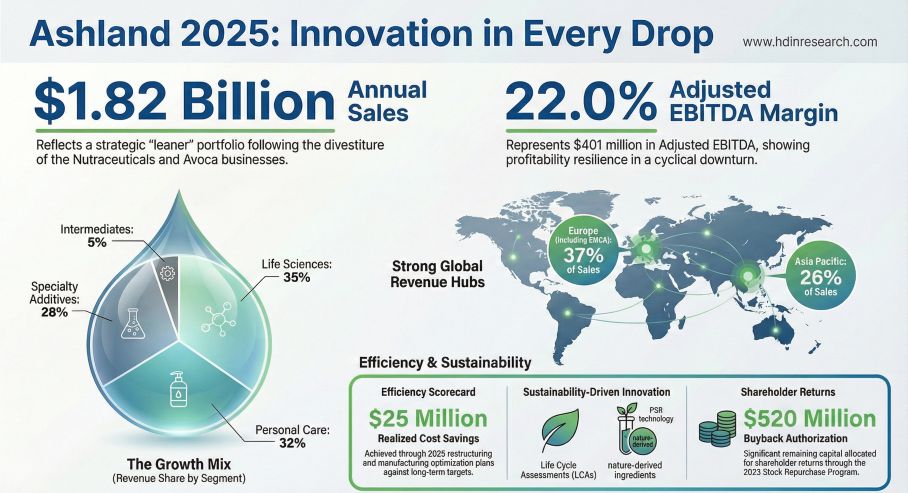

At first glance, the $845 million net loss and a 14% revenue contraction to $1.82 billion suggest significant distress. However, a granular analysis reveals that portfolio optimization—specifically the divestiture of the Nutraceuticals and Avoca businesses—was the primary driver of the revenue compression, rather than a fundamental erosion of market share.

Crucially, Ashland has maintained robust profitability ratios in its remaining core. The Adjusted EBITDA margin stood firm at approximately 22%, underpinned by a proactive "Manufacturing Optimization" plan. This indicates that despite the "kitchen sinking" of legacy asset valuations, the company’s pricing power in premium segments remains intact. The substantial impairment charge serves to cleanse the balance sheet of historical acquisition premiums, aligning asset book values with the current high-interest-rate environment and setting a cleaner baseline for future ROIC (Return on Invested Capital) calculations.

Sector Positioning: The Flight to Quality in Life Sciences

Ashland’s defensive moat is increasingly defined by its dominance in Life Sciences, particularly in pharmaceutical excipients (Cellulosics and PVP).

* Technological Hegemony: Cellulosics and PVP products now contribute 64% of total sales, with Life Sciences accounting for 85% of this high-value mix.

* Margin Expansion: Despite volume pressures, the Life Sciences segment achieved an Adjusted EBITDA margin of 30.1%, expanding from the previous year.

This divergence between volume and margin highlights a critical strategic success: by exiting low-margin commodity lines like standard CMC (carboxymethyl cellulose) and focusing on complex, regulated markets (such as controlled-release drug formulations), Ashland is successfully combating commoditization. Furthermore, the Personal Care segment is leveraging proprietary technologies, such as Zeta Fraction™, to capture demand for bio-degradable and "clean label" ingredients, directly addressing the stringent requirements of the EU’s CSRD and microplastic regulations.

Operational Alpha: The $60M Efficiency Play

Facing heightened geopolitical friction and tariff escalations in 2025, Ashland has accelerated its "Local for Local" manufacturing strategy. With 26% of sales originating from the Asia-Pacific region, the company is aggressively localizing production in China.

This is not merely a defensive maneuver against trade barriers; it is a margin-accretive operational overhaul. The ongoing Manufacturing Optimization Plan is projected to yield between $50 million and $60 million in annual savings. Additionally, the company’s Intermediates (BDO) segment is functioning effectively as a shock absorber. By retaining captive use of 1,4-butanediol, Ashland insulates its downstream high-margin businesses from volatile raw material spot prices, securing supply chain stability.

HDIN Viewpoint

At HDIN Research, we view fiscal year 2025 as a definitive "clearing of the decks" for Ashland. The company has effectively traded revenue volume for profit quality.

The critical metric for investors in 2026 will not be top-line expansion, but Capital Allocation Efficiency. With a net leverage ratio of 2.8x (well below the 4.0x covenant limit) and a $103 million tax refund bolstering liquidity, Ashland is well-positioned to continue its shareholder return program through buybacks and dividends. If the company can deliver on its guidance of 1-5% organic volume growth while realizing the projected manufacturing savings, it will have successfully navigated the transition from a diversified chemical supplier to a specialized, high-multiple ingredients franchise.

Presentation Download

For a comprehensive breakdown of Ashland’s segment performance, SWOT analysis, and detailed financial modeling, please click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Ashland 2025 innovation in Every Drop

Financial Resilience: Beyond the Accounting NoiseAt first glance, the $845 million net loss and a 14% revenue contraction to $1.82 billion suggest significant distress. However, a granular analysis reveals that portfolio optimization—specifically the divestiture of the Nutraceuticals and Avoca businesses—was the primary driver of the revenue compression, rather than a fundamental erosion of market share.

Crucially, Ashland has maintained robust profitability ratios in its remaining core. The Adjusted EBITDA margin stood firm at approximately 22%, underpinned by a proactive "Manufacturing Optimization" plan. This indicates that despite the "kitchen sinking" of legacy asset valuations, the company’s pricing power in premium segments remains intact. The substantial impairment charge serves to cleanse the balance sheet of historical acquisition premiums, aligning asset book values with the current high-interest-rate environment and setting a cleaner baseline for future ROIC (Return on Invested Capital) calculations.

Sector Positioning: The Flight to Quality in Life Sciences

Ashland’s defensive moat is increasingly defined by its dominance in Life Sciences, particularly in pharmaceutical excipients (Cellulosics and PVP).

* Technological Hegemony: Cellulosics and PVP products now contribute 64% of total sales, with Life Sciences accounting for 85% of this high-value mix.

* Margin Expansion: Despite volume pressures, the Life Sciences segment achieved an Adjusted EBITDA margin of 30.1%, expanding from the previous year.

This divergence between volume and margin highlights a critical strategic success: by exiting low-margin commodity lines like standard CMC (carboxymethyl cellulose) and focusing on complex, regulated markets (such as controlled-release drug formulations), Ashland is successfully combating commoditization. Furthermore, the Personal Care segment is leveraging proprietary technologies, such as Zeta Fraction™, to capture demand for bio-degradable and "clean label" ingredients, directly addressing the stringent requirements of the EU’s CSRD and microplastic regulations.

Operational Alpha: The $60M Efficiency Play

Facing heightened geopolitical friction and tariff escalations in 2025, Ashland has accelerated its "Local for Local" manufacturing strategy. With 26% of sales originating from the Asia-Pacific region, the company is aggressively localizing production in China.

This is not merely a defensive maneuver against trade barriers; it is a margin-accretive operational overhaul. The ongoing Manufacturing Optimization Plan is projected to yield between $50 million and $60 million in annual savings. Additionally, the company’s Intermediates (BDO) segment is functioning effectively as a shock absorber. By retaining captive use of 1,4-butanediol, Ashland insulates its downstream high-margin businesses from volatile raw material spot prices, securing supply chain stability.

HDIN Viewpoint

At HDIN Research, we view fiscal year 2025 as a definitive "clearing of the decks" for Ashland. The company has effectively traded revenue volume for profit quality.

The critical metric for investors in 2026 will not be top-line expansion, but Capital Allocation Efficiency. With a net leverage ratio of 2.8x (well below the 4.0x covenant limit) and a $103 million tax refund bolstering liquidity, Ashland is well-positioned to continue its shareholder return program through buybacks and dividends. If the company can deliver on its guidance of 1-5% organic volume growth while realizing the projected manufacturing savings, it will have successfully navigated the transition from a diversified chemical supplier to a specialized, high-multiple ingredients franchise.

Presentation Download

For a comprehensive breakdown of Ashland’s segment performance, SWOT analysis, and detailed financial modeling, please click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com