2025 Industrial Financial Analysis: Divergent Moats & Strategic Pivots

Date : 2026-02-21

Reading : 222

The era of the sprawling industrial conglomerate is officially dissolving. Based on a comprehensive cross-sectional diagnosis of the 2024-2025 fiscal years, HDIN Research has identified a decisive structural shift among global industrial titans. The latest financial data from Honeywell, Emerson, Powell Industries, Rockwell Automation, and Woodward reveals a market bifurcating into two distinct value creation models: "Pure-Play" software-defined automation and high-barrier "Niche" hardware infrastructure.

While aggregate revenues across the sector reflect a complex macroeconomic environment—characterized by fluctuating PMIs and supply chain regionalization—the "So What" lies in the source of profitability. Capital is no longer rewarding generalist scale; it is chasing specific strategic moats, from AI-driven data center electrification to 40-year aerospace lifecycles.

Figure 2025 Industrial Giants: The Performance Leaderboard

The Great "Pure-Play" Transformation

The Great "Pure-Play" Transformation

The most significant strategic development of 2025 is the aggressive portfolio restructuring by industry leaders seeking to eliminate the "conglomerate discount."

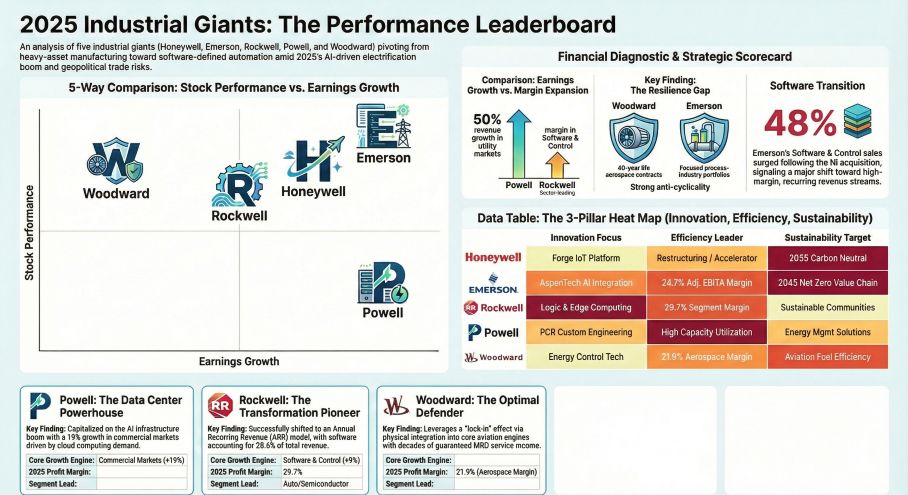

Honeywell has initiated a historic pivot by announcing the spin-off of its Advanced Materials and Aerospace businesses to become a focused automation entity. Similarly, Emerson has completed its transformation into a "pure-play" automation powerhouse. By divesting its climate technologies (Copeland) and aggressively acquiring National Instruments (now Test & Measurement) and a majority stake in AspenTech, Emerson has structurally elevated its gross margin ceiling (reaching 50.8%).

HDIN Research notes that this is not merely financial engineering but a fundamental operational shift. Emerson and Rockwell Automation are effectively converting from hardware vendors to industrial software providers, prioritizing Annual Recurring Revenue (ARR) over volume-based hardware sales. Rockwell’s "Software & Control" segment, boasting margins near 30%, exemplifies this push to decouple earnings from cyclical manufacturing downturns.

The "AI Hardware" Boom: Operating Leverage in Action

While software captures headlines, Powell Industries demonstrates that the physical infrastructure required to power AI offers superior short-term operating leverage.

Powell has successfully capitalized on the capital expenditure cycles of the Data Center and LNG sectors. With a 50% surge in Utility revenue and a backlog sitting at historic highs ($1.4 billion), Powell has achieved the group's most impressive margin expansion. This growth is driven by a "hardware overflow" effect—AI requires massive power density, and Powell’s custom electrical control rooms are the critical bottleneck. Unlike the software players, Powell’s valuation is currently driven by classic industrial operating leverage: utilizing fixed capacity to deliver outsized net income growth (up 21%) on rising volume.

The Unassailable Moat: Aerospace Physics vs. Software Code

In our comparative moat analysis, Woodward emerges as the most defensively positioned entity against inflation and recession risks.

While Rockwell utilizes a high switching-cost moat through its Logix/FactoryTalk ecosystem, Woodward relies on a "Sole Source" regulatory moat. HDIN Research emphasizes that Woodward’s position on platforms like the CFM LEAP and Pratt & Whitney GTF engines grants it pricing power that fully offsets inflation. Unlike software, which can be disrupted by digital transformation, Woodward’s fuel systems are integrated into the physics of the engine and certified by the FAA, locking in revenue for 40-year lifecycles. This makes Woodward’s cash flow profile uniquely uncorrelated to the broader manufacturing PMI.

HDIN Viewpoint: The Valuation Gap Will Widen

HDIN Research posits that 2026 will be a year of valuation divergence based on capital allocation efficiency:

1. The "Local-for-Local" Imperative: With trade policies and tariffs cited as top risks by Honeywell and Rockwell for 2026, the winners will be those who have completed their supply chain regionalization. Woodward’s localized production strategy effectively hedges against cross-border friction, a model others must emulate.

2. The AI Reality Check: The market is distinguishing between "AI Concept" and "AI Revenue." Emerson (via AspenTech) and Rockwell are successfully monetizing AI through optimization software subscriptions. However, Powell proves that the immediate cash flow opportunity lies in the *electrification hardware* supporting AI, not just the algorithms.

3. Cyclical Resilience: Investors should look beyond top-line growth. Rockwell’s ability to maintain high free cash flow conversion (156%) despite a discrete manufacturing slowdown highlights the superior quality of software-derived earnings compared to pure hardware volume.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report and the full comparative financial datasets.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

While aggregate revenues across the sector reflect a complex macroeconomic environment—characterized by fluctuating PMIs and supply chain regionalization—the "So What" lies in the source of profitability. Capital is no longer rewarding generalist scale; it is chasing specific strategic moats, from AI-driven data center electrification to 40-year aerospace lifecycles.

Figure 2025 Industrial Giants: The Performance Leaderboard

The Great "Pure-Play" TransformationThe most significant strategic development of 2025 is the aggressive portfolio restructuring by industry leaders seeking to eliminate the "conglomerate discount."

Honeywell has initiated a historic pivot by announcing the spin-off of its Advanced Materials and Aerospace businesses to become a focused automation entity. Similarly, Emerson has completed its transformation into a "pure-play" automation powerhouse. By divesting its climate technologies (Copeland) and aggressively acquiring National Instruments (now Test & Measurement) and a majority stake in AspenTech, Emerson has structurally elevated its gross margin ceiling (reaching 50.8%).

HDIN Research notes that this is not merely financial engineering but a fundamental operational shift. Emerson and Rockwell Automation are effectively converting from hardware vendors to industrial software providers, prioritizing Annual Recurring Revenue (ARR) over volume-based hardware sales. Rockwell’s "Software & Control" segment, boasting margins near 30%, exemplifies this push to decouple earnings from cyclical manufacturing downturns.

The "AI Hardware" Boom: Operating Leverage in Action

While software captures headlines, Powell Industries demonstrates that the physical infrastructure required to power AI offers superior short-term operating leverage.

Powell has successfully capitalized on the capital expenditure cycles of the Data Center and LNG sectors. With a 50% surge in Utility revenue and a backlog sitting at historic highs ($1.4 billion), Powell has achieved the group's most impressive margin expansion. This growth is driven by a "hardware overflow" effect—AI requires massive power density, and Powell’s custom electrical control rooms are the critical bottleneck. Unlike the software players, Powell’s valuation is currently driven by classic industrial operating leverage: utilizing fixed capacity to deliver outsized net income growth (up 21%) on rising volume.

The Unassailable Moat: Aerospace Physics vs. Software Code

In our comparative moat analysis, Woodward emerges as the most defensively positioned entity against inflation and recession risks.

While Rockwell utilizes a high switching-cost moat through its Logix/FactoryTalk ecosystem, Woodward relies on a "Sole Source" regulatory moat. HDIN Research emphasizes that Woodward’s position on platforms like the CFM LEAP and Pratt & Whitney GTF engines grants it pricing power that fully offsets inflation. Unlike software, which can be disrupted by digital transformation, Woodward’s fuel systems are integrated into the physics of the engine and certified by the FAA, locking in revenue for 40-year lifecycles. This makes Woodward’s cash flow profile uniquely uncorrelated to the broader manufacturing PMI.

HDIN Viewpoint: The Valuation Gap Will Widen

HDIN Research posits that 2026 will be a year of valuation divergence based on capital allocation efficiency:

1. The "Local-for-Local" Imperative: With trade policies and tariffs cited as top risks by Honeywell and Rockwell for 2026, the winners will be those who have completed their supply chain regionalization. Woodward’s localized production strategy effectively hedges against cross-border friction, a model others must emulate.

2. The AI Reality Check: The market is distinguishing between "AI Concept" and "AI Revenue." Emerson (via AspenTech) and Rockwell are successfully monetizing AI through optimization software subscriptions. However, Powell proves that the immediate cash flow opportunity lies in the *electrification hardware* supporting AI, not just the algorithms.

3. Cyclical Resilience: Investors should look beyond top-line growth. Rockwell’s ability to maintain high free cash flow conversion (156%) despite a discrete manufacturing slowdown highlights the superior quality of software-derived earnings compared to pure hardware volume.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report and the full comparative financial datasets.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com