2025 Global Biopharma Landscape: Navigating Patent Cliffs Through Strategic Moats, GLP-1 Duopoly and AI Integration

Date : 2026-02-23

Reading : 383

Global pharmaceutical giants are navigating a critical inflection point in 2025. Based on an exhaustive audit of the top 11 biopharma conglomerates, HDIN Research reveals a definitive structural transformation: a departure from broad-based diversification toward hyper-focused strategic moats. Propelled by the impending 2026 patent cliff, industry leaders are aggressively optimizing capital allocation efficiency, embedding artificial intelligence (AI) into clinical infrastructure, and leveraging the unprecedented cardiometabolic boom to secure long-term sector positioning.

Capital Allocation Efficiency: The Bifurcation of Corporate Strategy

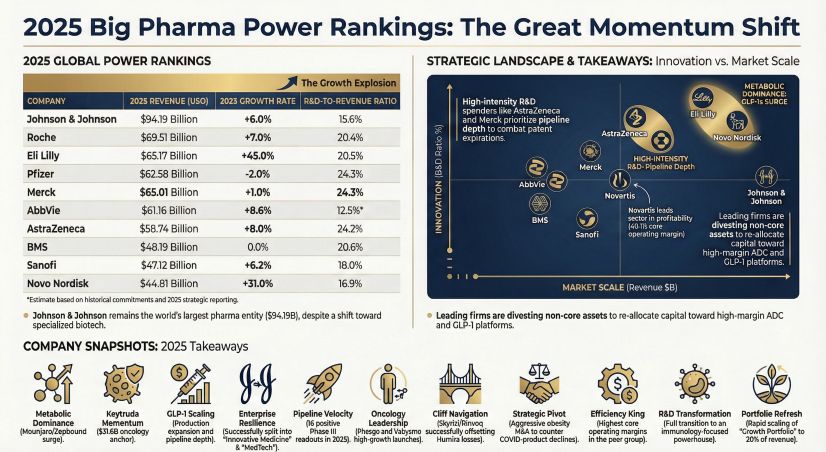

In 2025, capital allocation strategies have sharply bifurcated, reflecting a mandate for capital efficiency over sheer scale. Organizations are actively shedding legacy constraints to fund high-risk, high-margin innovation.

On one end of the spectrum, companies are executing ruthless strategic spin-offs. Following the divestiture of its consumer health division Kenvue, Johnson & Johnson (J&J) announced the planned separation of its DePuy Synthes orthopaedics business to transition into a pure-play "Innovative Medicine" and "MedTech" entity. Similarly, Sanofi offloaded a 50% stake in its Opella consumer healthcare unit, generating roughly €10 billion to fuel its R&D-driven immunology ambitions.

Conversely, companies like Novartis, Pfizer, and Roche are leveraging targeted M&A to rapidly construct technological moats. Pfizer’s strategic acquisition of Metsera—securing ten ultra-long-acting obesity assets—exemplifies the urgency to buy into high-growth therapeutic vectors, while Novartis utilized high-frequency mid-cap acquisitions to densely populate its core pipelines.

Sector Positioning: The GLP-1 Duopoly and Oncology Fortress

The revenue dynamics of 2025 are unequivocally defined by the "Cardiometabolic Duopoly." Eli Lilly and Novo Nordisk have transformed from industry stalwarts into unprecedented growth engines. Eli Lilly led the cohort with a staggering 45% year-over-year revenue surge, driven by its Mounjaro and Zepbound franchises, which now constitute 56% of its total revenue. Novo Nordisk maintained its volume dominance, capturing a 43% global share of the GLP-1 market and a 59.6% share in branded obesity medications.

The strategic implication is profound: cardiometabolic therapies are displacing legacy segments as the primary driver of incremental market value. Meanwhile, in the oncology sector, Merck’s Keytruda remains a formidable fortress, generating over $31.6 billion in sales. However, as the immuno-oncology (IO) landscape becomes increasingly congested, players like AstraZeneca and J&J are deploying massive R&D budgets ($14.2 billion and $14.7 billion, respectively) into next-generation modalities like Antibody-Drug Conjugates (ADCs) and bispecifics to defend their sector positioning.

Cyclical Headwinds: Confronting the 2026 Patent Cliff

The industry is simultaneously battling severe cyclical headwinds stemming from the loss of exclusivity (LOE) for flagship blockbuster drugs. The patent cliff is forcing aggressive portfolio iteration. AbbVie’s Humira witnessed a precipitous 49.4% revenue decline due to biosimilar erosion, accelerating the company's pivot to its "growth portfolio" of Skyrizi and Rinvoq.

Companies caught in the transition phase are navigating deep strategic turbulence. Bristol Myers Squibb (BMS) saw its legacy Revlimid portfolio plummet by 49%, while Pfizer absorbed a massive $4.4 billion non-cash impairment, primarily linked to the reevaluation of in-process R&D assets. These financial metrics underscore that without aggressive pipeline acceleration, legacy erosion will rapidly outpace incremental clinical gains.

Technological Moats: AI as R&D Infrastructure

2025 marks the milestone where AI transitioned from a theoretical concept to foundational R&D infrastructure. For pharmaceutical giants, AI integration is no longer a peripheral innovation but a mandatory driver of operational efficiency.

Sanofi leads the cohort in AI-powered execution, claiming that 90% of its current pipeline targets are validated by data and AI systems, effectively doubling its molecular design throughput. AstraZeneca directly embedded multi-modal foundational models into its oncology R&D ecosystem via the acquisition of Modella AI. Furthermore, Roche is demonstrating a unique "Diagnostic + Pharma" dual-engine synergy, utilizing FDA-breakthrough AI computational pathology tools to fundamentally redefine early disease detection and treatment probability.

HDIN Viewpoint

From an institutional perspective, HDIN Research concludes that the biopharma landscape is no longer a game of total asset volume, but of localized agility and pipeline certainty. The impending 2026 LOE wave—particularly impacting molecules like semaglutide in China and Eliquis in Europe—requires proactive regional defense strategies.

Despite centralized procurement (VBP) pricing pressures, Greater China remains an indispensable strategic growth engine. AstraZeneca’s pledge to invest $15 billion in Chinese R&D and manufacturing by 2030, alongside Sanofi’s "Controlled Integration" strategy, highlights the necessity of embedding into local innovation ecosystems rather than operating as mere commercial outposts.

Ultimately, HDIN Research identifies Johnson & Johnson, Eli Lilly, and AstraZeneca as the institutions exhibiting the highest financial resilience and anti-cyclical stability in 2025. The definitive winners of the next decade will be those who successfully synthesize AI-empowered R&D efficiency with ruthless capital allocation to defend their strategic moats.

Figure 2025 Big Pharma Power Rankings The Great Momentum Shift

Click the PDF download link under “Related Topics” to access the presentation of this report.

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Capital Allocation Efficiency: The Bifurcation of Corporate Strategy

In 2025, capital allocation strategies have sharply bifurcated, reflecting a mandate for capital efficiency over sheer scale. Organizations are actively shedding legacy constraints to fund high-risk, high-margin innovation.

On one end of the spectrum, companies are executing ruthless strategic spin-offs. Following the divestiture of its consumer health division Kenvue, Johnson & Johnson (J&J) announced the planned separation of its DePuy Synthes orthopaedics business to transition into a pure-play "Innovative Medicine" and "MedTech" entity. Similarly, Sanofi offloaded a 50% stake in its Opella consumer healthcare unit, generating roughly €10 billion to fuel its R&D-driven immunology ambitions.

Conversely, companies like Novartis, Pfizer, and Roche are leveraging targeted M&A to rapidly construct technological moats. Pfizer’s strategic acquisition of Metsera—securing ten ultra-long-acting obesity assets—exemplifies the urgency to buy into high-growth therapeutic vectors, while Novartis utilized high-frequency mid-cap acquisitions to densely populate its core pipelines.

Sector Positioning: The GLP-1 Duopoly and Oncology Fortress

The revenue dynamics of 2025 are unequivocally defined by the "Cardiometabolic Duopoly." Eli Lilly and Novo Nordisk have transformed from industry stalwarts into unprecedented growth engines. Eli Lilly led the cohort with a staggering 45% year-over-year revenue surge, driven by its Mounjaro and Zepbound franchises, which now constitute 56% of its total revenue. Novo Nordisk maintained its volume dominance, capturing a 43% global share of the GLP-1 market and a 59.6% share in branded obesity medications.

The strategic implication is profound: cardiometabolic therapies are displacing legacy segments as the primary driver of incremental market value. Meanwhile, in the oncology sector, Merck’s Keytruda remains a formidable fortress, generating over $31.6 billion in sales. However, as the immuno-oncology (IO) landscape becomes increasingly congested, players like AstraZeneca and J&J are deploying massive R&D budgets ($14.2 billion and $14.7 billion, respectively) into next-generation modalities like Antibody-Drug Conjugates (ADCs) and bispecifics to defend their sector positioning.

Cyclical Headwinds: Confronting the 2026 Patent Cliff

The industry is simultaneously battling severe cyclical headwinds stemming from the loss of exclusivity (LOE) for flagship blockbuster drugs. The patent cliff is forcing aggressive portfolio iteration. AbbVie’s Humira witnessed a precipitous 49.4% revenue decline due to biosimilar erosion, accelerating the company's pivot to its "growth portfolio" of Skyrizi and Rinvoq.

Companies caught in the transition phase are navigating deep strategic turbulence. Bristol Myers Squibb (BMS) saw its legacy Revlimid portfolio plummet by 49%, while Pfizer absorbed a massive $4.4 billion non-cash impairment, primarily linked to the reevaluation of in-process R&D assets. These financial metrics underscore that without aggressive pipeline acceleration, legacy erosion will rapidly outpace incremental clinical gains.

Technological Moats: AI as R&D Infrastructure

2025 marks the milestone where AI transitioned from a theoretical concept to foundational R&D infrastructure. For pharmaceutical giants, AI integration is no longer a peripheral innovation but a mandatory driver of operational efficiency.

Sanofi leads the cohort in AI-powered execution, claiming that 90% of its current pipeline targets are validated by data and AI systems, effectively doubling its molecular design throughput. AstraZeneca directly embedded multi-modal foundational models into its oncology R&D ecosystem via the acquisition of Modella AI. Furthermore, Roche is demonstrating a unique "Diagnostic + Pharma" dual-engine synergy, utilizing FDA-breakthrough AI computational pathology tools to fundamentally redefine early disease detection and treatment probability.

HDIN Viewpoint

From an institutional perspective, HDIN Research concludes that the biopharma landscape is no longer a game of total asset volume, but of localized agility and pipeline certainty. The impending 2026 LOE wave—particularly impacting molecules like semaglutide in China and Eliquis in Europe—requires proactive regional defense strategies.

Despite centralized procurement (VBP) pricing pressures, Greater China remains an indispensable strategic growth engine. AstraZeneca’s pledge to invest $15 billion in Chinese R&D and manufacturing by 2030, alongside Sanofi’s "Controlled Integration" strategy, highlights the necessity of embedding into local innovation ecosystems rather than operating as mere commercial outposts.

Ultimately, HDIN Research identifies Johnson & Johnson, Eli Lilly, and AstraZeneca as the institutions exhibiting the highest financial resilience and anti-cyclical stability in 2025. The definitive winners of the next decade will be those who successfully synthesize AI-empowered R&D efficiency with ruthless capital allocation to defend their strategic moats.

Figure 2025 Big Pharma Power Rankings The Great Momentum Shift

Click the PDF download link under “Related Topics” to access the presentation of this report.About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com