2025 MedTech Giants: Strategic Moats & Market Outlook

Date : 2026-02-23

Reading : 567

The 2025 fiscal year marks a watershed moment for global medical device titans. The era of pure hardware arms races has concluded, replaced by a sophisticated battle for clinical workflow integration and digital ecosystems. Based on an exhaustive analysis of 2025 annual filings, HDIN Research reveals that Siemens Healthineers (SHL), GE HealthCare (GEHC), and Philips are rapidly diverging in their capital allocation efficiency and strategic positioning. While macroeconomic volatility and cyclical headwinds persist, operational efficiency, AI-driven synergies, and resilient supply chains are dictating market leadership.

Financial Health & Capital Allocation Efficiency

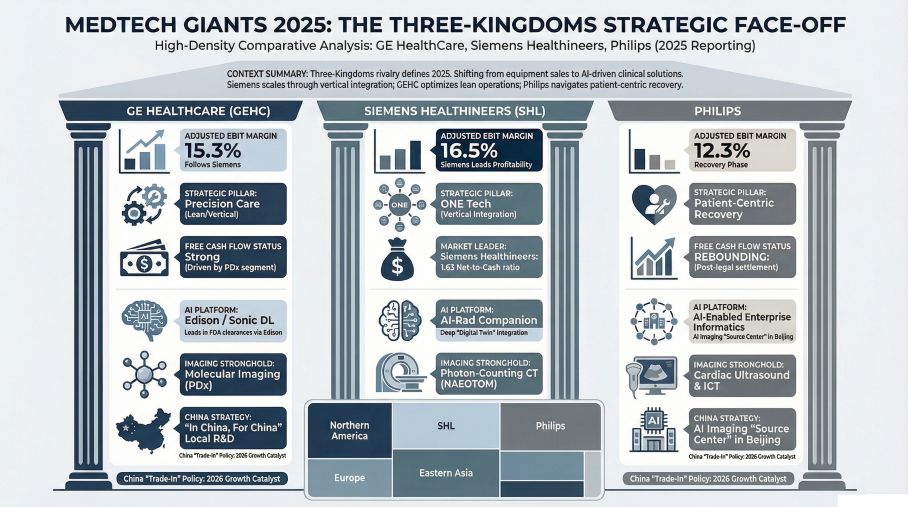

A granular teardown of profitability and cash flow metrics reveals stark contrasts in how these giants are generating shareholder value in a high-cost environment.

* Siemens Healthineers: The Robust Cash Engine: SHL has proven to be an exceptionally resilient cash generator. HDIN Research highlights its impressive net-to-cash conversion ratio of 1.63—meaning every euro of net profit translates to 1.63 euros of operating cash flow. This liquidity fuels aggressive R&D capital allocation (8.4% of revenue), specifically targeting deep-tech vertical integration such as photon-counting CT detectors and semiconductor manufacturing facilities.

* GE HealthCare: Lean Operations and High ROE: Operating post-spinoff with a highly streamlined structure, GEHC boasts the highest revenue per employee ($381,900) among the three. Through aggressive lean management systems and high leverage efficiency, GEHC achieved a stellar Return on Equity (ROE) of 20.1%. Its capital allocation strategy heavily favors software M&A (e.g., MIM Software) and active share buybacks, padding earnings per share (EPS) while aggressively capturing the digital software moat.

* Philips: Turnaround and Rebuilding: Philips remains in a critical transitional phase. While heavily burdened by non-recurring legal settlements (a €1.025 billion payout in 2025 related to the Respironics recall), the company's core operations are slowly stabilizing. Its current capital allocation prioritizes resolving legal headwinds, streamlining operations to recover free cash flow, and maintaining dividend stability rather than aggressive hardware expansion.

Strategic Moats & Sector Positioning

Beyond overlapping strengths in medical imaging, the true competitive moats of 2025 are being built in adjacent, highly synergistic business units that insulate these companies from cyclical shocks.

* GEHC's Drug-Device Synergy: GEHC leverages its Pharmaceutical Diagnostics (PDx) division as a high-margin cash engine (30.1% EBIT margin). By coupling radiopharmaceuticals with advanced molecular imaging (PET/CT), GEHC locks hospitals into a recurring revenue model. This "consumables plus equipment" moat effectively cushions the company against localized pricing shocks, such as Volume-Based Procurement (VBP) programs.

* Siemens' Diagnostic-to-Therapeutic Loop: SHL has masterfully utilized its Varian acquisition to create an end-to-end oncology ecosystem. By integrating market-leading diagnostic imaging with Varian’s radiation therapy platforms, SHL has built a closed-loop "Patient Twinning" framework. Because global cancer center infrastructure requires decades-long lifecycles, this segment possesses extreme resistance to short-term deglobalization and tariff fluctuations.

* Philips' Precision Intervention & Informatics: Philips has consciously pivoted away from volume-based low-end competition, moving its strategic weight toward premium Image-Guided Therapy (IGT). Backed by its world-class Azurion platform and leading Enterprise Informatics architecture, Philips holds a dominant global position in cardiovascular interventions, embedding its ecosystem deeply within top-tier hospitals' surgical workflows.

Cyclical Headwinds & Greater China Localization

Navigating the "post-anti-corruption" era and localized procurement policies in Greater China serves as the ultimate stress test for global MedTech agility.

* Siemens has captured early momentum by leveraging China’s "tiered hospital system" and large-scale equipment renewal programs, stabilizing its top-line faster than its peers.

* GEHC is executing a "boundless innovation" strategy, heavily pivoting to localized manufacturing (over 30 facilities outside the US, heavily anchored in China) to defend its premium positioning against fierce domestic alternatives.

* Philips is shifting its gravity toward high-end R&D, establishing its Greater China R&D headquarters in Beijing to cultivate an AI innovation hub that addresses the specific efficiency pain points of elite hospitals.

HDIN Viewpoint: The Next Frontier

From the perspective of HDIN Research, the 2025 data confirms a definitive industry pivot: hardware is no longer the sole growth driver; it is merely the vessel for high-margin software, consumables, and recurring services. We assess that Siemens Healthineers is structurally positioned to dominate the long-term deep-tech frontier. GEHC remains the most aggressive and financially optimized player, maximizing near-term shareholder returns through pharmaceutical synergies and digital acquisitions. Meanwhile, Philips represents a calculated value-recovery play, provided it can successfully navigate its ongoing legal and consumer-sentiment headwinds. Looking ahead to 2026, AI integration will transition fully from "clinical lab concepts" to "enterprise-wide workflow automation," fundamentally rewriting the competitive hierarchy of the global MedTech sector.

Figure MedTech Giants 2025: The Three-Kingdoms Strategic Face-off

Presentation Download

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Financial Health & Capital Allocation Efficiency

A granular teardown of profitability and cash flow metrics reveals stark contrasts in how these giants are generating shareholder value in a high-cost environment.

* Siemens Healthineers: The Robust Cash Engine: SHL has proven to be an exceptionally resilient cash generator. HDIN Research highlights its impressive net-to-cash conversion ratio of 1.63—meaning every euro of net profit translates to 1.63 euros of operating cash flow. This liquidity fuels aggressive R&D capital allocation (8.4% of revenue), specifically targeting deep-tech vertical integration such as photon-counting CT detectors and semiconductor manufacturing facilities.

* GE HealthCare: Lean Operations and High ROE: Operating post-spinoff with a highly streamlined structure, GEHC boasts the highest revenue per employee ($381,900) among the three. Through aggressive lean management systems and high leverage efficiency, GEHC achieved a stellar Return on Equity (ROE) of 20.1%. Its capital allocation strategy heavily favors software M&A (e.g., MIM Software) and active share buybacks, padding earnings per share (EPS) while aggressively capturing the digital software moat.

* Philips: Turnaround and Rebuilding: Philips remains in a critical transitional phase. While heavily burdened by non-recurring legal settlements (a €1.025 billion payout in 2025 related to the Respironics recall), the company's core operations are slowly stabilizing. Its current capital allocation prioritizes resolving legal headwinds, streamlining operations to recover free cash flow, and maintaining dividend stability rather than aggressive hardware expansion.

Strategic Moats & Sector Positioning

Beyond overlapping strengths in medical imaging, the true competitive moats of 2025 are being built in adjacent, highly synergistic business units that insulate these companies from cyclical shocks.

* GEHC's Drug-Device Synergy: GEHC leverages its Pharmaceutical Diagnostics (PDx) division as a high-margin cash engine (30.1% EBIT margin). By coupling radiopharmaceuticals with advanced molecular imaging (PET/CT), GEHC locks hospitals into a recurring revenue model. This "consumables plus equipment" moat effectively cushions the company against localized pricing shocks, such as Volume-Based Procurement (VBP) programs.

* Siemens' Diagnostic-to-Therapeutic Loop: SHL has masterfully utilized its Varian acquisition to create an end-to-end oncology ecosystem. By integrating market-leading diagnostic imaging with Varian’s radiation therapy platforms, SHL has built a closed-loop "Patient Twinning" framework. Because global cancer center infrastructure requires decades-long lifecycles, this segment possesses extreme resistance to short-term deglobalization and tariff fluctuations.

* Philips' Precision Intervention & Informatics: Philips has consciously pivoted away from volume-based low-end competition, moving its strategic weight toward premium Image-Guided Therapy (IGT). Backed by its world-class Azurion platform and leading Enterprise Informatics architecture, Philips holds a dominant global position in cardiovascular interventions, embedding its ecosystem deeply within top-tier hospitals' surgical workflows.

Cyclical Headwinds & Greater China Localization

Navigating the "post-anti-corruption" era and localized procurement policies in Greater China serves as the ultimate stress test for global MedTech agility.

* Siemens has captured early momentum by leveraging China’s "tiered hospital system" and large-scale equipment renewal programs, stabilizing its top-line faster than its peers.

* GEHC is executing a "boundless innovation" strategy, heavily pivoting to localized manufacturing (over 30 facilities outside the US, heavily anchored in China) to defend its premium positioning against fierce domestic alternatives.

* Philips is shifting its gravity toward high-end R&D, establishing its Greater China R&D headquarters in Beijing to cultivate an AI innovation hub that addresses the specific efficiency pain points of elite hospitals.

HDIN Viewpoint: The Next Frontier

From the perspective of HDIN Research, the 2025 data confirms a definitive industry pivot: hardware is no longer the sole growth driver; it is merely the vessel for high-margin software, consumables, and recurring services. We assess that Siemens Healthineers is structurally positioned to dominate the long-term deep-tech frontier. GEHC remains the most aggressive and financially optimized player, maximizing near-term shareholder returns through pharmaceutical synergies and digital acquisitions. Meanwhile, Philips represents a calculated value-recovery play, provided it can successfully navigate its ongoing legal and consumer-sentiment headwinds. Looking ahead to 2026, AI integration will transition fully from "clinical lab concepts" to "enterprise-wide workflow automation," fundamentally rewriting the competitive hierarchy of the global MedTech sector.

Figure MedTech Giants 2025: The Three-Kingdoms Strategic Face-off

Presentation DownloadClick the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com