2025 Global Agricultural Machinery Strategic Review: Algorithms, Asset Restructuring, and Cyclical Resilience

Date : 2026-02-23

Reading : 149

In 2025, the global agricultural machinery sector navigated a severe cyclical winter, characterized by depressed farm net incomes, elevated interest rates, and geopolitical tariff frictions. However, beneath the surface of declining high-horsepower equipment volumes, a profound structural transformation is accelerating. Based on the latest annual report analysis by HDIN Research, industry giants—Deere & Company, AGCO, CLAAS, and The Toro Company—are aggressively pivoting their strategic moats from "steel and horsepower" to "algorithms and connectivity." Operational efficiency, aggressive capital reallocation, and niche sector positioning have become the primary levers to defend double-digit Return on Equity (ROE) amidst macro headwinds.

Figure 2025 Agricultural & Landscaping Machinery: The Great Divergence

Cyclical Headwinds and Capital Allocation Efficiency

Cyclical Headwinds and Capital Allocation Efficiency

The 2025 financial landscape vividly illustrates the decoupling of unit volumes from underlying financial health. While top-line revenues faced systemic pressure, disciplined capital allocation efficiency provided a critical safety cushion.

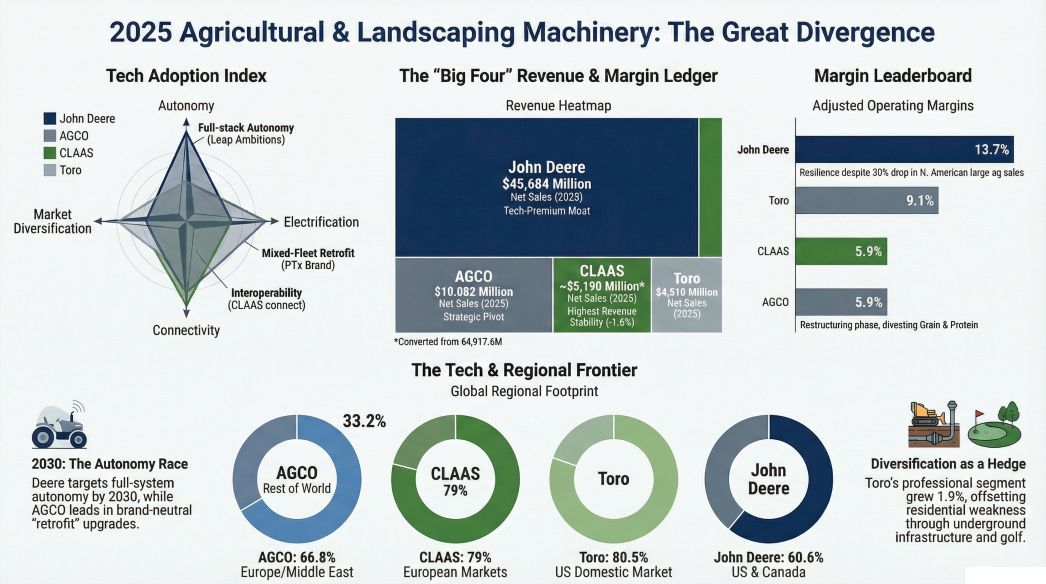

Deere & Company confronted a 17% revenue contraction in its Production and Precision Ag (PPA) segment, exacerbated by a $600 million direct hit from new U.S. import tariffs and a 30% sales plunge in North America. So what? Deere countered this margin erosion through extreme financial leverage (equity multiplier of 4.37) and geographic hedging—a 22% sales surge in Brazil effectively offset North American losses, allowing the company to sustain a robust 20.6% ROE and generate $6.1 billion in free cash flow (FCF).

Conversely, The Toro Company showcased premier asset turnover (1.28), driving its ROE to 21.0%. Toro's exceptional FCF conversion rate of 145.6% underscores high earnings quality, empowering the firm to execute nearly $300 million in share repurchases despite a 14% volume drop in its residential segment.

Strategic Moats: The Transition from Hardware to Algorithms

The core competitive arena has irrevocably shifted toward software-as-a-service (SaaS) and autonomous architecture. The 2025 data reveals highly divergent, yet equally calculated, technology roadmaps.

* Deere’s Vertical Tech Premium: Deere maintained an industry-leading absolute R&D spend of $2.3 billion (5.1% of sales), defending its closed-loop ecosystem. Its "Leap Ambitions" strategy prioritizes fully autonomous farming by 2030, utilizing machine learning (e.g., See & Spray™ technology) to transform hardware sales into recurring, high-margin software subscriptions.

* AGCO’s Strategic Slimming and Retrofit Pivot: AGCO executed the most dramatic balance sheet restructuring of the year, divesting its low-margin Grain & Protein (G&P) business for $700 million. This capital was immediately redirected to its PTx brand. AGCO’s strategic moat is now "brand-agnostic retrofitting"—allowing farmers to upgrade existing mixed-fleet assets with advanced precision technology without purchasing new tractors. This lower-barrier entry strategy is highly defensive during periods of constrained capital expenditure.

* CLAAS’s R&D Intensity: As a privately held European entity, CLAAS exhibited the highest R&D intensity at 6.5%. Unburdened by short-term shareholder dividend pressures, CLAAS is heavily investing in alternative powertrains (e.g., the TORION 537e electric loader) and interoperable digital ecosystems like *CLAAS connect*.

Sector Positioning: Niche Safe Havens and Cost Defenses

To combat the agricultural downcycle, strategic sector positioning proved vital. The Toro Company successfully insulated its balance sheet by leaning into its Professional Segment, which grew 1.9% against the broader industry trend. By capitalizing on underground construction (Ditch Witch) and acquiring Tornado Infrastructure Equipment, Toro effectively used infrastructure supercycles to hedge against residential and agricultural volatility. Furthermore, Toro's AMP (Amplifying Maximum Productivity) initiative is structurally optimizing its supply chain, targeting $125 million in annualized savings by 2027 to ensure maximum operating leverage when demand rebounds.

Similarly, CLAAS demonstrated remarkable top-line resilience, with revenues dipping a mere 1.6%. The strategic implication here lies in its end-market exposure: while grain prices plummeted, stable dairy and meat prices sustained capital investments from CLAAS’s core livestock farming client base, proving the value of diversified agricultural exposure.

HDIN Viewpoint: The Destocking Race and 2026 Outlook

HDIN Research concludes that the trajectory of the 2026-2027 recovery will be dictated by the speed of channel destocking. Currently, Toro is leading the industry out of the inventory quagmire, having successfully reduced its golf and turf product inventories below 2024 levels. In contrast, Deere faces friction from a bloated late-model used equipment market, forcing higher sales incentives that pressure price realization. AGCO remains in a high-pressure phase, having slashed production hours by 12.1% to artificially match weak terminal demand.

For institutional investors and strategic planners, the takeaway is clear: the next upcycle will not reward pure manufacturing scale. The highest premiums will flow to enterprises that have successfully monetized agricultural data (Deere), monopolized the mixed-fleet retrofit aftermarket (AGCO), or structurally diversified into non-ag infrastructure (Toro).

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Agricultural & Landscaping Machinery: The Great Divergence

Cyclical Headwinds and Capital Allocation EfficiencyThe 2025 financial landscape vividly illustrates the decoupling of unit volumes from underlying financial health. While top-line revenues faced systemic pressure, disciplined capital allocation efficiency provided a critical safety cushion.

Deere & Company confronted a 17% revenue contraction in its Production and Precision Ag (PPA) segment, exacerbated by a $600 million direct hit from new U.S. import tariffs and a 30% sales plunge in North America. So what? Deere countered this margin erosion through extreme financial leverage (equity multiplier of 4.37) and geographic hedging—a 22% sales surge in Brazil effectively offset North American losses, allowing the company to sustain a robust 20.6% ROE and generate $6.1 billion in free cash flow (FCF).

Conversely, The Toro Company showcased premier asset turnover (1.28), driving its ROE to 21.0%. Toro's exceptional FCF conversion rate of 145.6% underscores high earnings quality, empowering the firm to execute nearly $300 million in share repurchases despite a 14% volume drop in its residential segment.

Strategic Moats: The Transition from Hardware to Algorithms

The core competitive arena has irrevocably shifted toward software-as-a-service (SaaS) and autonomous architecture. The 2025 data reveals highly divergent, yet equally calculated, technology roadmaps.

* Deere’s Vertical Tech Premium: Deere maintained an industry-leading absolute R&D spend of $2.3 billion (5.1% of sales), defending its closed-loop ecosystem. Its "Leap Ambitions" strategy prioritizes fully autonomous farming by 2030, utilizing machine learning (e.g., See & Spray™ technology) to transform hardware sales into recurring, high-margin software subscriptions.

* AGCO’s Strategic Slimming and Retrofit Pivot: AGCO executed the most dramatic balance sheet restructuring of the year, divesting its low-margin Grain & Protein (G&P) business for $700 million. This capital was immediately redirected to its PTx brand. AGCO’s strategic moat is now "brand-agnostic retrofitting"—allowing farmers to upgrade existing mixed-fleet assets with advanced precision technology without purchasing new tractors. This lower-barrier entry strategy is highly defensive during periods of constrained capital expenditure.

* CLAAS’s R&D Intensity: As a privately held European entity, CLAAS exhibited the highest R&D intensity at 6.5%. Unburdened by short-term shareholder dividend pressures, CLAAS is heavily investing in alternative powertrains (e.g., the TORION 537e electric loader) and interoperable digital ecosystems like *CLAAS connect*.

Sector Positioning: Niche Safe Havens and Cost Defenses

To combat the agricultural downcycle, strategic sector positioning proved vital. The Toro Company successfully insulated its balance sheet by leaning into its Professional Segment, which grew 1.9% against the broader industry trend. By capitalizing on underground construction (Ditch Witch) and acquiring Tornado Infrastructure Equipment, Toro effectively used infrastructure supercycles to hedge against residential and agricultural volatility. Furthermore, Toro's AMP (Amplifying Maximum Productivity) initiative is structurally optimizing its supply chain, targeting $125 million in annualized savings by 2027 to ensure maximum operating leverage when demand rebounds.

Similarly, CLAAS demonstrated remarkable top-line resilience, with revenues dipping a mere 1.6%. The strategic implication here lies in its end-market exposure: while grain prices plummeted, stable dairy and meat prices sustained capital investments from CLAAS’s core livestock farming client base, proving the value of diversified agricultural exposure.

HDIN Viewpoint: The Destocking Race and 2026 Outlook

HDIN Research concludes that the trajectory of the 2026-2027 recovery will be dictated by the speed of channel destocking. Currently, Toro is leading the industry out of the inventory quagmire, having successfully reduced its golf and turf product inventories below 2024 levels. In contrast, Deere faces friction from a bloated late-model used equipment market, forcing higher sales incentives that pressure price realization. AGCO remains in a high-pressure phase, having slashed production hours by 12.1% to artificially match weak terminal demand.

For institutional investors and strategic planners, the takeaway is clear: the next upcycle will not reward pure manufacturing scale. The highest premiums will flow to enterprises that have successfully monetized agricultural data (Deere), monopolized the mixed-fleet retrofit aftermarket (AGCO), or structurally diversified into non-ag infrastructure (Toro).

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com