2025 lnfusion MedTech Giants: Strategic Pivots, Capital Allocation, and the Reshaping of Industry Moats

Date : 2026-02-23

Reading : 124

The 2025 fiscal year marks a definitive transition for global MedTech leaders. Facing a confluence of cyclical headwinds—ranging from geopolitical tariff escalations to severe supply chain disruptions and relentless pricing pressures—industry giants such as Becton Dickinson (BD), Baxter International, and ICU Medical are aggressively pivoting. Analysis by HDIN Research reveals that these corporations are systematically shedding low-margin legacy assets, radically restructuring their capital allocation, and doubling down on AI-driven connected care to redefine their strategic moats.

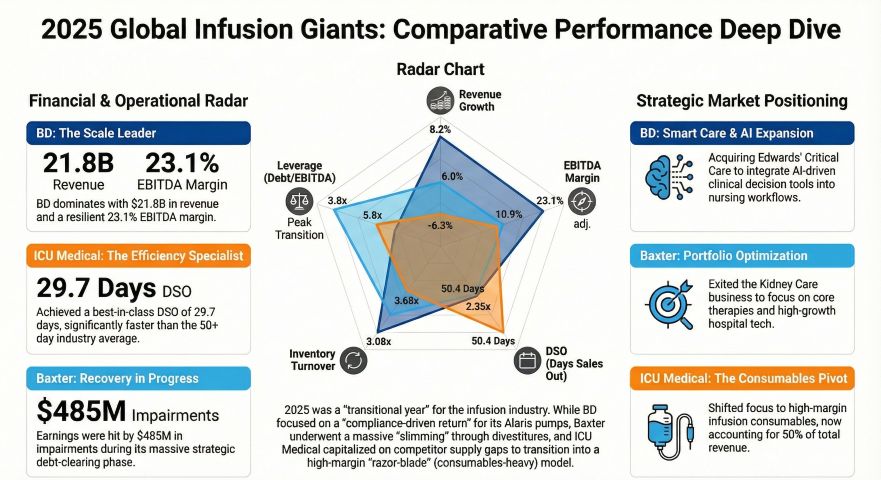

Figure 2025 Global lnfusion Giants Comparative Performance Deep Dive

Navigating Cyclical Headwinds and Supply Chain Vulnerabilities

Navigating Cyclical Headwinds and Supply Chain Vulnerabilities

Macroeconomic volatility has exposed the structural vulnerabilities of traditional MedTech supply chains. The 2025 cycle was defined by severe operational disruptions, notably Hurricane Helene’s impact on Baxter’s North Carolina facilities, which triggered nationwide IV solution shortages. This event served as a catalyst, forcing the industry to transition from “just-in-time” efficiency to “resilience-first” operational models.

Furthermore, geopolitical trade barriers and policy-driven cost pressures have severely compressed gross margins. The implementation of "Liberation Day" reciprocal tariffs by the U.S. has directly impacted players heavily reliant on Latin American manufacturing footprints, such as ICU Medical and BD, pushing import duties from Costa Rica and Mexico to alarming new baselines. Concurrently, Volume-Based Procurement (VBP) in the Chinese market has decimated the pricing power of legacy consumables. In response, these giants are no longer passively absorbing costs; they are executing strategic withdrawals. Baxter’s complete exit from the commoditized IV solutions market in China is a prime example of sacrificing low-quality revenue to preserve underlying profitability.

Capital Allocation Efficiency: The "Slim Down" Era

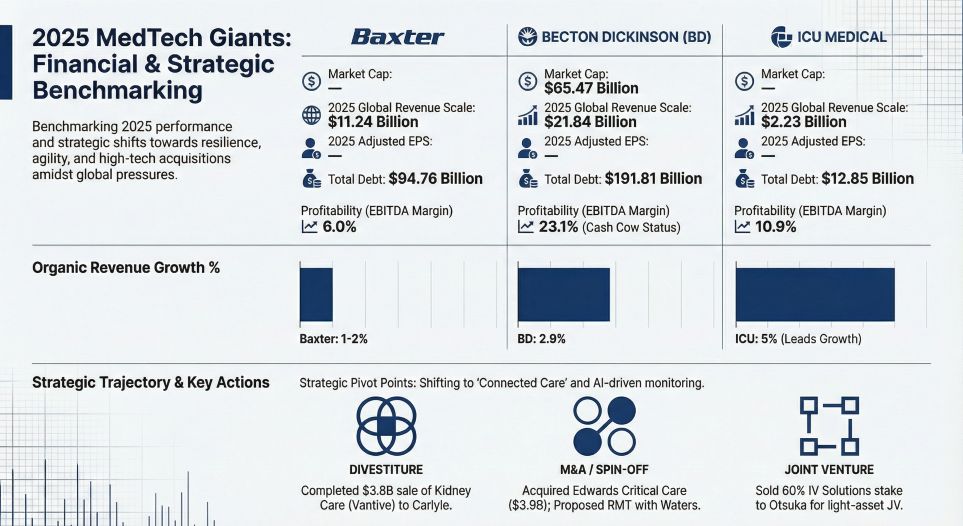

In 2025, the strategic consensus among top-tier MedTech firms can be summarized as: slim down, deleverage, and smarten up. Capital allocation efficiency has taken precedence over sheer revenue expansion, resulting in a wave of high-profile divestitures.

Instead of deploying capital toward capacity expansion for commoditized products, these firms are shedding heavy manufacturing risks. Baxter finalized the spin-off of its Vantive (Kidney Care) business, utilizing the multi-billion-dollar proceeds to aggressively deleverage its balance sheet, targeting a rigorous 3.0x net leverage ratio by 2026. BD initiated a Reverse Morris Trust transaction to separate its Biosciences division, isolating cyclical volatility to focus on its core medical consumables. ICU Medical, grappling with the debt load from its Smiths Medical integration, transferred a 60% controlling stake in its low-margin IV solutions business to a joint venture with Otsuka. This masterstroke allows ICU Medical to transition into an asset-light entity, sharing raw material inflation risks while retaining lucrative distribution rights.

Redefining Strategic Moats: From Hardware to AI-Driven Ecosystems

As the growth ceiling for basic plastics and standard IV solutions crashes, MedTech leaders are constructing new competitive moats anchored in digital integration and the highly profitable "razor-blade" commercial model.

Hardware is no longer the end product; it is the trojan horse for recurring software and specialty consumable revenues. BD’s acquisition of Edwards Lifesciences' Advanced Patient Monitoring business exemplifies this, injecting AI-driven clinical decision tools directly into its existing hospital networks to command premium pricing. ICU Medical has aggressively leveraged its new Plum Duo™ precision infusion pumps to lock hospital networks into long-term utilization of its high-margin, proprietary oncology and airway consumables. Meanwhile, Baxter is pivoting its hospital enterprise strategy toward completely integrated digital workflows, utilizing Smart Bed systems and connected care ecosystems to raise the switching costs for hospital networks.

HDIN Viewpoint

HDIN Research concludes that 2025 is the definitive "Year of Transformation" for the medical device sector. The era of generating alpha through mass-market, low-barrier plastics is definitively over. As inflation outpaces the fixed-price contracts of Group Purchasing Organizations (GPOs), corporate survival now hinges on portfolio agility. We believe that the true valuation metric for MedTech giants in the upcoming 2026 cycle will not be their top-line equipment installations, but rather the proportion of their software-integrated service revenue and the geographic elasticity of their tariff-hedged supply chains. Companies that fail to optimize their capital allocation toward niche, high-barrier connected care will find themselves permanently trapped beneath the industry's tightening margin ceiling.

Figure 2025 MedTech Giants Financial & Strategic Benchmarking

Presentation Download

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global lnfusion Giants Comparative Performance Deep Dive

Navigating Cyclical Headwinds and Supply Chain VulnerabilitiesMacroeconomic volatility has exposed the structural vulnerabilities of traditional MedTech supply chains. The 2025 cycle was defined by severe operational disruptions, notably Hurricane Helene’s impact on Baxter’s North Carolina facilities, which triggered nationwide IV solution shortages. This event served as a catalyst, forcing the industry to transition from “just-in-time” efficiency to “resilience-first” operational models.

Furthermore, geopolitical trade barriers and policy-driven cost pressures have severely compressed gross margins. The implementation of "Liberation Day" reciprocal tariffs by the U.S. has directly impacted players heavily reliant on Latin American manufacturing footprints, such as ICU Medical and BD, pushing import duties from Costa Rica and Mexico to alarming new baselines. Concurrently, Volume-Based Procurement (VBP) in the Chinese market has decimated the pricing power of legacy consumables. In response, these giants are no longer passively absorbing costs; they are executing strategic withdrawals. Baxter’s complete exit from the commoditized IV solutions market in China is a prime example of sacrificing low-quality revenue to preserve underlying profitability.

Capital Allocation Efficiency: The "Slim Down" Era

In 2025, the strategic consensus among top-tier MedTech firms can be summarized as: slim down, deleverage, and smarten up. Capital allocation efficiency has taken precedence over sheer revenue expansion, resulting in a wave of high-profile divestitures.

Instead of deploying capital toward capacity expansion for commoditized products, these firms are shedding heavy manufacturing risks. Baxter finalized the spin-off of its Vantive (Kidney Care) business, utilizing the multi-billion-dollar proceeds to aggressively deleverage its balance sheet, targeting a rigorous 3.0x net leverage ratio by 2026. BD initiated a Reverse Morris Trust transaction to separate its Biosciences division, isolating cyclical volatility to focus on its core medical consumables. ICU Medical, grappling with the debt load from its Smiths Medical integration, transferred a 60% controlling stake in its low-margin IV solutions business to a joint venture with Otsuka. This masterstroke allows ICU Medical to transition into an asset-light entity, sharing raw material inflation risks while retaining lucrative distribution rights.

Redefining Strategic Moats: From Hardware to AI-Driven Ecosystems

As the growth ceiling for basic plastics and standard IV solutions crashes, MedTech leaders are constructing new competitive moats anchored in digital integration and the highly profitable "razor-blade" commercial model.

Hardware is no longer the end product; it is the trojan horse for recurring software and specialty consumable revenues. BD’s acquisition of Edwards Lifesciences' Advanced Patient Monitoring business exemplifies this, injecting AI-driven clinical decision tools directly into its existing hospital networks to command premium pricing. ICU Medical has aggressively leveraged its new Plum Duo™ precision infusion pumps to lock hospital networks into long-term utilization of its high-margin, proprietary oncology and airway consumables. Meanwhile, Baxter is pivoting its hospital enterprise strategy toward completely integrated digital workflows, utilizing Smart Bed systems and connected care ecosystems to raise the switching costs for hospital networks.

HDIN Viewpoint

HDIN Research concludes that 2025 is the definitive "Year of Transformation" for the medical device sector. The era of generating alpha through mass-market, low-barrier plastics is definitively over. As inflation outpaces the fixed-price contracts of Group Purchasing Organizations (GPOs), corporate survival now hinges on portfolio agility. We believe that the true valuation metric for MedTech giants in the upcoming 2026 cycle will not be their top-line equipment installations, but rather the proportion of their software-integrated service revenue and the geographic elasticity of their tariff-hedged supply chains. Companies that fail to optimize their capital allocation toward niche, high-barrier connected care will find themselves permanently trapped beneath the industry's tightening margin ceiling.

Figure 2025 MedTech Giants Financial & Strategic Benchmarking

Presentation DownloadClick the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com