Strategic Shifts and Margin Expansion: Unpacking Blue Bird’s FY2025 Electrification Dominance

Date : 2026-02-24

Reading : 115

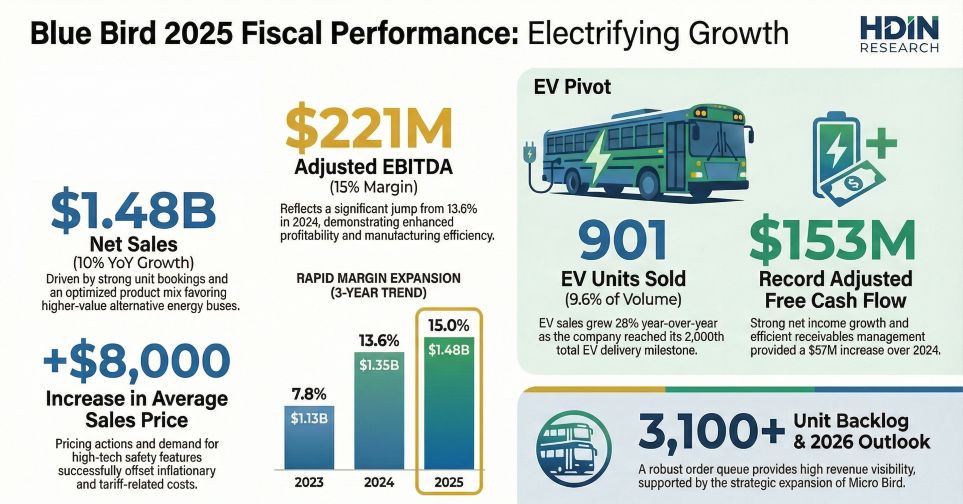

In FY2025, Blue Bird Corporation successfully cemented its transition from a traditional industrial manufacturer to a green-tech mobility powerhouse. While the headline figures show a robust 9.9% year-over-year increase in total net sales to $1.48 billion, the underlying strategic implication is far more profound: alternative-powered vehicles now account for a dominant 53.9% of total revenue ($798.4 million). Driven by aggressive product mix optimization, disciplined pricing power, and a rapid shift toward integrated ecosystem services, Blue Bird has effectively decoupled its profitability from traditional manufacturing bottlenecks, establishing a highly resilient growth model.

Figure Blue Bird 2025 Fiscal Performance Electrifying Growth

Financial Health: Pricing Power and Capital Allocation Efficiency

Financial Health: Pricing Power and Capital Allocation Efficiency

Blue Bird’s FY2025 financial performance highlights a masterclass in margin protection and Capital Allocation Efficiency. The company’s Adjusted EBITDA surged to $221.3 million, achieving a 15.0% margin—a striking recovery from 7.8% in FY2023. Furthermore, overall gross margins expanded from 19.0% to 20.5%.

The "So What" behind these numbers lies in the company's defensive pricing strategy. By institutionalizing "Price Escalation Provisions" in long-term contracts, Blue Bird successfully transferred the dual pressures of raw material inflation and recent import tariffs directly to the end-user. This drove a 6.0% increase in the Average Selling Price (ASP).

Simultaneously, Blue Bird generated $153.3 million in Free Cash Flow (FCF) and ended the year in a net cash position ($229.3 million in cash versus $91.3 million in long-term debt). This fortress balance sheet ensures ultimate capital flexibility. Even as the new 2025 administration reviews the $80 million Department of Energy (DOE) MESC grant, Blue Bird possesses the internal liquidity to independently fund its $160 million factory retrofit, ensuring its manufacturing roadmap remains uninterrupted.

Redefining Sector Positioning Through Strategic Moats

Blue Bird currently commands a staggering 64% cumulative market share (2015-2025) in the U.S. alternative-powered school bus market. However, the company is no longer just selling buses; it is building formidable Strategic Moats through deep-rooted technological partnerships and business model innovation.

* Multi-Faceted Powertrain Alliances: Rather than insourcing all R&D, Blue Bird leverages exclusive, long-term partnerships with Cummins/Accelera for electric vehicles (EVs) and Ford/Roush for propane and gasoline engines. This allows them to offer best-in-class, vertically integrated chassis designs that competitors struggle to replicate.

* The Fleet-as-a-Service (FaaS) Pivot: Through its Clean Bus Solutions (CBS) joint venture, Blue Bird is actively shifting its Sector Positioning from a one-off hardware vendor to an integrated mobility ecosystem provider. By offering financing, charging infrastructure, and lifecycle maintenance, the company is laying the groundwork for high-margin, recurring subscription revenues.

* Commercial Market Expansion: The September 2025 operational launch of the Micro Bird facility in Plattsburgh, NY, signals Blue Bird’s strategic entry into the lucrative Class 5-6 commercial step-van market, effectively diversifying its revenue base beyond the cyclical school district procurement cycles.

Navigating Cyclical Headwinds and Policy Dependencies

The rapid adoption of electric school buses remains heavily tethered to federal incentives, particularly the EPA’s $5 billion Clean School Bus Program (CSBP), which has already fueled over 1,400 orders for Blue Bird. Potential delays or reviews of EPA and DOE funding under the new administration introduce distinct policy risks.

However, Blue Bird has proactively structured its operations to weather these Cyclical Headwinds. The company has not over-indexed purely on EVs; its proprietary propane-powered models currently run 90% cleaner than existing EPA standards, pre-emptively meeting stringent 2027 emissions regulations. This provides cash-strapped school districts with a highly attractive Total Cost of Ownership (TCO) alternative if federal EV subsidies recede. Additionally, by locking in 65% of its procurement volume under long-term supplier contracts, Blue Bird has heavily insulated its supply chain against geopolitical and macroeconomic shocks.

HDIN Viewpoint

HDIN Research views Blue Bird as a fundamentally de-risked asset poised for a potential valuation re-rating. The market currently prices the company as a specialized heavy-duty manufacturer, yet its financial profile is rapidly mirroring that of a high-margin green-tech firm.

Two primary catalysts will drive future shareholder value: First, as EV penetration scales (901 units sold in FY25, +28% YoY) and the high-margin parts division (50.3% gross margin) expands, we anticipate consolidated gross margins breaking the 25% threshold. Second, the planned termination and buyout of the company's legacy pension plan in FY2026 will eradicate a major long-term balance sheet overhang, further clarifying free cash flow visibility. Blue Bird's ability to monetize its FaaS ecosystem while dominating the alternative energy transition makes it a premium asset in the commercial EV landscape.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Blue Bird 2025 Fiscal Performance Electrifying Growth

Financial Health: Pricing Power and Capital Allocation EfficiencyBlue Bird’s FY2025 financial performance highlights a masterclass in margin protection and Capital Allocation Efficiency. The company’s Adjusted EBITDA surged to $221.3 million, achieving a 15.0% margin—a striking recovery from 7.8% in FY2023. Furthermore, overall gross margins expanded from 19.0% to 20.5%.

The "So What" behind these numbers lies in the company's defensive pricing strategy. By institutionalizing "Price Escalation Provisions" in long-term contracts, Blue Bird successfully transferred the dual pressures of raw material inflation and recent import tariffs directly to the end-user. This drove a 6.0% increase in the Average Selling Price (ASP).

Simultaneously, Blue Bird generated $153.3 million in Free Cash Flow (FCF) and ended the year in a net cash position ($229.3 million in cash versus $91.3 million in long-term debt). This fortress balance sheet ensures ultimate capital flexibility. Even as the new 2025 administration reviews the $80 million Department of Energy (DOE) MESC grant, Blue Bird possesses the internal liquidity to independently fund its $160 million factory retrofit, ensuring its manufacturing roadmap remains uninterrupted.

Redefining Sector Positioning Through Strategic Moats

Blue Bird currently commands a staggering 64% cumulative market share (2015-2025) in the U.S. alternative-powered school bus market. However, the company is no longer just selling buses; it is building formidable Strategic Moats through deep-rooted technological partnerships and business model innovation.

* Multi-Faceted Powertrain Alliances: Rather than insourcing all R&D, Blue Bird leverages exclusive, long-term partnerships with Cummins/Accelera for electric vehicles (EVs) and Ford/Roush for propane and gasoline engines. This allows them to offer best-in-class, vertically integrated chassis designs that competitors struggle to replicate.

* The Fleet-as-a-Service (FaaS) Pivot: Through its Clean Bus Solutions (CBS) joint venture, Blue Bird is actively shifting its Sector Positioning from a one-off hardware vendor to an integrated mobility ecosystem provider. By offering financing, charging infrastructure, and lifecycle maintenance, the company is laying the groundwork for high-margin, recurring subscription revenues.

* Commercial Market Expansion: The September 2025 operational launch of the Micro Bird facility in Plattsburgh, NY, signals Blue Bird’s strategic entry into the lucrative Class 5-6 commercial step-van market, effectively diversifying its revenue base beyond the cyclical school district procurement cycles.

Navigating Cyclical Headwinds and Policy Dependencies

The rapid adoption of electric school buses remains heavily tethered to federal incentives, particularly the EPA’s $5 billion Clean School Bus Program (CSBP), which has already fueled over 1,400 orders for Blue Bird. Potential delays or reviews of EPA and DOE funding under the new administration introduce distinct policy risks.

However, Blue Bird has proactively structured its operations to weather these Cyclical Headwinds. The company has not over-indexed purely on EVs; its proprietary propane-powered models currently run 90% cleaner than existing EPA standards, pre-emptively meeting stringent 2027 emissions regulations. This provides cash-strapped school districts with a highly attractive Total Cost of Ownership (TCO) alternative if federal EV subsidies recede. Additionally, by locking in 65% of its procurement volume under long-term supplier contracts, Blue Bird has heavily insulated its supply chain against geopolitical and macroeconomic shocks.

HDIN Viewpoint

HDIN Research views Blue Bird as a fundamentally de-risked asset poised for a potential valuation re-rating. The market currently prices the company as a specialized heavy-duty manufacturer, yet its financial profile is rapidly mirroring that of a high-margin green-tech firm.

Two primary catalysts will drive future shareholder value: First, as EV penetration scales (901 units sold in FY25, +28% YoY) and the high-margin parts division (50.3% gross margin) expands, we anticipate consolidated gross margins breaking the 25% threshold. Second, the planned termination and buyout of the company's legacy pension plan in FY2026 will eradicate a major long-term balance sheet overhang, further clarifying free cash flow visibility. Blue Bird's ability to monetize its FaaS ecosystem while dominating the alternative energy transition makes it a premium asset in the commercial EV landscape.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com