Ferrari 2025: How Scarcity Management and Electrification Pivots Are Redefining Luxury Mobility

Date : 2026-02-23

Reading : 199

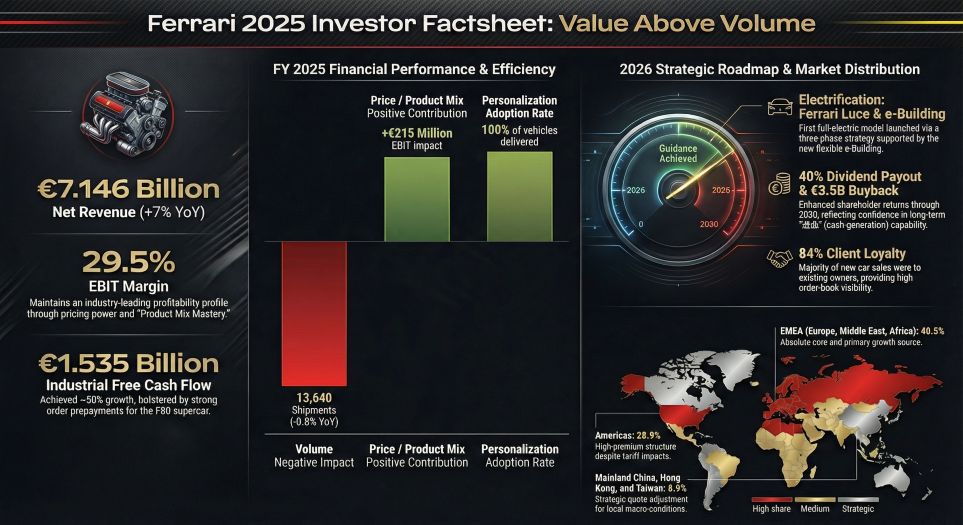

In an era defined by cyclical headwinds and plateauing global luxury consumption, Ferrari N.V.’s 2025 financial results demonstrate an unparalleled strategic moat. Rather than succumbing to macroeconomic pressures, the automaker utilized its "Controlled Volume Strategy" to engineer a masterclass in value generation. Despite a slight 0.8% dip in total unit shipments (13,640 units), operational efficiency, a highly calibrated product mix, and aggressive customization drove an 11.8% surge in operating profit (EBIT). This decoupling from broader market volatility proves that Ferrari’s fundamental logic is rooted not in automotive manufacturing, but in ultra-luxury asset management.

Financial Health & Capital Allocation Efficiency

Ferrari’s 2025 financials reflect a remarkably robust capital allocation efficiency. Net revenues grew by 7.0% to €7.146 billion, but the more critical metric is the disproportionate growth in profitability. EBIT margins expanded to a record 29.5% (€2.11 billion). The strategic implication here is clear: Ferrari is successfully replacing pure volume growth with deep margin extraction.

This profitability is underpinned by a fortress-like cash position. In 2025, the company generated €1.535 billion in Industrial Free Cash Flow. This exceptional cash generation effectively self-funded the €1.014 billion required for intensive R&D and infrastructure expansion (including the new e-Building) while seamlessly covering €1.317 billion in shareholder returns through dividends and share buybacks. The ability to heavily finance future transition risks without diluting shareholder value is a rare hallmark of peak financial health.

Sector Positioning: The Customization Engine and Profit Per Unit

When evaluating sector positioning, Ferrari’s Profit Per Unit (PPU) completely isolates it from both mass-luxury players like Porsche and direct ultra-luxury rivals like Aston Martin. Based on 2025 data, HDIN Research calculates Ferrari’s average PPU at an astounding €154,700.

This margin supremacy is driven by a 100% penetration rate in personalization. Every vehicle delivered in 2025 featured bespoke modifications. Because the marginal cost of exclusive materials (e.g., carbon fiber, tailored leather) is remarkably low compared to the price premium they command, the "Personalization" segment alone injected a €215 million positive impact into the product mix. Furthermore, Ferrari’s scarcity management guarantees extreme residual values in the secondary market, feeding a loyal ecosystem where 84% of 2025 buyers were returning clients.

Strategic Pivots: Navigating the Electrification Horizon

Ferrari is currently executing a high-stakes strategic pivot, balancing its iconic Internal Combustion Engine (ICE) legacy with inevitable environmental regulations. Interestingly, 2025 saw ICE shipments rise to 58% of the total mix (up from 49% in 2024), driven by the massive success of the V12 Purosangue and the 12Cilindri.

However, regulatory headwinds are intensifying. Having surpassed the 10,000-unit production threshold, Ferrari has lost its Small Volume Manufacturer (SVM) status in key jurisdictions, exposing it to stricter emissions standards like Euro 7. To secure its future, Ferrari has adopted a "Technology Neutral" infrastructure. The newly operational €1+ billion *e-Building* in Maranello provides the ultimate manufacturing flexibility, allowing ICE, Hybrid, and fully Electric vehicles to be built on the same line. With its first pure EV, the *Ferrari Luce*, already in the launch pipeline, Ferrari is insourcing critical components like high-voltage batteries and e-axles to ensure its electric offerings retain the brand's unmistakable driving dynamics.

HDIN Viewpoint: The Tech-Driven Luxury Paradigm

As an independent market research and consulting firm, HDIN Research views Ferrari not as a traditional automaker, but as a technology-driven luxury platform. The 2025 annual report validates that Ferrari’s true strategic moat lies in monetizing exclusivity.

The company is successfully turning potential brand-diluting risks—such as the EV transition—into avenues for margin expansion. Moreover, their Lifestyle and Brand segment (which surged 22.4% to €820 million in 2025) proves that the brand's cultural cachet can be monetized independently of vehicle delivery cycles. Moving into the 2026-2030 strategic window, Ferrari’s blend of strict supply constraint, aggressive technological insourcing, and impenetrable pricing power forms a commercial fortress that will be exceedingly difficult for competitors to breach.

Figure Ferrari 2025 Investor Factsheet: Value Above Volume

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Financial Health & Capital Allocation Efficiency

Ferrari’s 2025 financials reflect a remarkably robust capital allocation efficiency. Net revenues grew by 7.0% to €7.146 billion, but the more critical metric is the disproportionate growth in profitability. EBIT margins expanded to a record 29.5% (€2.11 billion). The strategic implication here is clear: Ferrari is successfully replacing pure volume growth with deep margin extraction.

This profitability is underpinned by a fortress-like cash position. In 2025, the company generated €1.535 billion in Industrial Free Cash Flow. This exceptional cash generation effectively self-funded the €1.014 billion required for intensive R&D and infrastructure expansion (including the new e-Building) while seamlessly covering €1.317 billion in shareholder returns through dividends and share buybacks. The ability to heavily finance future transition risks without diluting shareholder value is a rare hallmark of peak financial health.

Sector Positioning: The Customization Engine and Profit Per Unit

When evaluating sector positioning, Ferrari’s Profit Per Unit (PPU) completely isolates it from both mass-luxury players like Porsche and direct ultra-luxury rivals like Aston Martin. Based on 2025 data, HDIN Research calculates Ferrari’s average PPU at an astounding €154,700.

This margin supremacy is driven by a 100% penetration rate in personalization. Every vehicle delivered in 2025 featured bespoke modifications. Because the marginal cost of exclusive materials (e.g., carbon fiber, tailored leather) is remarkably low compared to the price premium they command, the "Personalization" segment alone injected a €215 million positive impact into the product mix. Furthermore, Ferrari’s scarcity management guarantees extreme residual values in the secondary market, feeding a loyal ecosystem where 84% of 2025 buyers were returning clients.

Strategic Pivots: Navigating the Electrification Horizon

Ferrari is currently executing a high-stakes strategic pivot, balancing its iconic Internal Combustion Engine (ICE) legacy with inevitable environmental regulations. Interestingly, 2025 saw ICE shipments rise to 58% of the total mix (up from 49% in 2024), driven by the massive success of the V12 Purosangue and the 12Cilindri.

However, regulatory headwinds are intensifying. Having surpassed the 10,000-unit production threshold, Ferrari has lost its Small Volume Manufacturer (SVM) status in key jurisdictions, exposing it to stricter emissions standards like Euro 7. To secure its future, Ferrari has adopted a "Technology Neutral" infrastructure. The newly operational €1+ billion *e-Building* in Maranello provides the ultimate manufacturing flexibility, allowing ICE, Hybrid, and fully Electric vehicles to be built on the same line. With its first pure EV, the *Ferrari Luce*, already in the launch pipeline, Ferrari is insourcing critical components like high-voltage batteries and e-axles to ensure its electric offerings retain the brand's unmistakable driving dynamics.

HDIN Viewpoint: The Tech-Driven Luxury Paradigm

As an independent market research and consulting firm, HDIN Research views Ferrari not as a traditional automaker, but as a technology-driven luxury platform. The 2025 annual report validates that Ferrari’s true strategic moat lies in monetizing exclusivity.

The company is successfully turning potential brand-diluting risks—such as the EV transition—into avenues for margin expansion. Moreover, their Lifestyle and Brand segment (which surged 22.4% to €820 million in 2025) proves that the brand's cultural cachet can be monetized independently of vehicle delivery cycles. Moving into the 2026-2030 strategic window, Ferrari’s blend of strict supply constraint, aggressive technological insourcing, and impenetrable pricing power forms a commercial fortress that will be exceedingly difficult for competitors to breach.

Figure Ferrari 2025 Investor Factsheet: Value Above Volume

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com