ITW vs ESAB 2025: Strategic Moats and Capital Efficiency

Date : 2026-02-24

Reading : 102

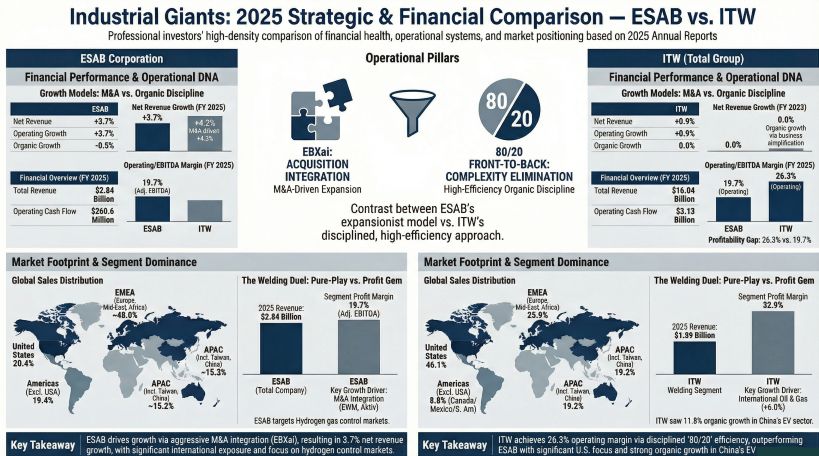

In the complex macro environment of fiscal 2025, industrial titans Illinois Tool Works (ITW) and ESAB Corporation charted starkly divergent paths to value creation. According to the latest proprietary analysis by HDIN Research, the narrative extends far beyond ESAB’s 3.7% revenue growth versus ITW’s 0.9% uptick. The true differentiator lies in their strategic moats: ITW’s rigorous complexity reduction versus ESAB’s aggressive, M&A-driven technological pivot.

Figure Industrial Giants 2025 Strategic & Financial Comparison - ESAB VS ITW

Capital Allocation Efficiency & Growth Engines

Capital Allocation Efficiency & Growth Engines

In 2025, the growth engines of both organizations highlighted entirely different capital allocation philosophies. ITW deployed its proprietary "80/20 Front-to-Back" framework to systematically prune underperforming product lines. While this product line simplification (PLS) suppressed organic top-line momentum, it fortified capital allocation efficiency, securing a formidable 26.3% operating margin. ITW essentially sacrificed low-yield volume for structural profitability, allowing its internal cash cow—the Welding division—to generate a staggering 32.9% operating margin.

Conversely, ESAB embraced a "Growth Elastic" model. Its 3.7% topline expansion to $2.84 billion was entirely inorganic, driven by a 4.2% M&A contribution that effectively offset cyclical headwinds and a 1.1% organic contraction. ESAB’s capital strategy is defined by expanding its total addressable market (TAM). The landmark $1.45 billion acquisition of Eddyfi Technologies signals a critical shift from traditional welding hardware to high-margin, software-defined digital inspection protocols, integrated via its EBXai business system.

Sector Positioning and Geographic Moats

Both entities leverage an "in the market, for the market" manufacturing doctrine to mitigate geopolitical friction, yet their geographic exposures present contrasting risk-reward paradigms. ITW maintains a fortified dual-core supply chain anchored heavily in the U.S. (46.1% of revenue) and China. Notably, ITW capitalized on secular tailwinds in China’s electric vehicle (EV) and semiconductor sectors, delivering an impressive 8.7% organic growth surge in the region.

ESAB, generating roughly 80% of its revenue outside the U.S., commands a dominant presence in high-growth emerging markets spanning South America, Eastern Europe, India, and the Middle East. Furthermore, ESAB’s robust "razor and blade" business model—where recurring consumables constitute 66% of total revenue—provides a structural hedge against capital expenditure volatility, softening the blow of cyclical headwinds in mature industrial sectors.

Financial Health & Earnings Quality

Delving into the balance sheet, HDIN Research identifies distinct profiles in financial health and risk management. ITW stands as a paragon of defensive value, boasting an exceptional 14.4x interest coverage ratio. Its highly localized manufacturing footprint and disciplined bad-debt provisioning effectively insulated its bottom line against the 2025 global tariff escalations.

ESAB countered inflationary pressures and tariff impacts through proactive pricing strategies ($29.4 million realized) and operational optimizations. However, a deeper DuPont analysis reveals that ESAB’s earnings quality warrants institutional scrutiny. In 2025, ESAB's inventory spiked by 19.3%, drastically outpacing its 3.7% revenue growth. Coupled with a reduction in credit loss allowances amidst geopolitical uncertainties, these metrics suggest potential working capital and earnings management risks that investors must monitor closely.

HDIN Viewpoint: The Institutional Perspective

From HDIN Research’s analytical vantage point, the 2025 landscape highlights a classic dichotomy in industrial sector positioning. ITW represents the ultimate "Value Defensive" asset. By strictly adhering to its 80/20 discipline, ITW actively manages cyclical headwinds, ensuring top-tier free cash flow conversion (~88%) and robust shareholder returns without over-leveraging its balance sheet.

ESAB, on the other hand, is an aggressive "Growth Elastic" play. Its success heavily depends on the EBXai system's ability to seamlessly integrate complex, high-tech acquisitions without breaking its tighter 4.9x interest coverage threshold. For stakeholders, the choice between ITW's impenetrable margin resilience and ESAB's aggressive TAM-expanding acquisitions will ultimately dictate portfolio beta in the impending industrial cycle.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Industrial Giants 2025 Strategic & Financial Comparison - ESAB VS ITW

Capital Allocation Efficiency & Growth EnginesIn 2025, the growth engines of both organizations highlighted entirely different capital allocation philosophies. ITW deployed its proprietary "80/20 Front-to-Back" framework to systematically prune underperforming product lines. While this product line simplification (PLS) suppressed organic top-line momentum, it fortified capital allocation efficiency, securing a formidable 26.3% operating margin. ITW essentially sacrificed low-yield volume for structural profitability, allowing its internal cash cow—the Welding division—to generate a staggering 32.9% operating margin.

Conversely, ESAB embraced a "Growth Elastic" model. Its 3.7% topline expansion to $2.84 billion was entirely inorganic, driven by a 4.2% M&A contribution that effectively offset cyclical headwinds and a 1.1% organic contraction. ESAB’s capital strategy is defined by expanding its total addressable market (TAM). The landmark $1.45 billion acquisition of Eddyfi Technologies signals a critical shift from traditional welding hardware to high-margin, software-defined digital inspection protocols, integrated via its EBXai business system.

Sector Positioning and Geographic Moats

Both entities leverage an "in the market, for the market" manufacturing doctrine to mitigate geopolitical friction, yet their geographic exposures present contrasting risk-reward paradigms. ITW maintains a fortified dual-core supply chain anchored heavily in the U.S. (46.1% of revenue) and China. Notably, ITW capitalized on secular tailwinds in China’s electric vehicle (EV) and semiconductor sectors, delivering an impressive 8.7% organic growth surge in the region.

ESAB, generating roughly 80% of its revenue outside the U.S., commands a dominant presence in high-growth emerging markets spanning South America, Eastern Europe, India, and the Middle East. Furthermore, ESAB’s robust "razor and blade" business model—where recurring consumables constitute 66% of total revenue—provides a structural hedge against capital expenditure volatility, softening the blow of cyclical headwinds in mature industrial sectors.

Financial Health & Earnings Quality

Delving into the balance sheet, HDIN Research identifies distinct profiles in financial health and risk management. ITW stands as a paragon of defensive value, boasting an exceptional 14.4x interest coverage ratio. Its highly localized manufacturing footprint and disciplined bad-debt provisioning effectively insulated its bottom line against the 2025 global tariff escalations.

ESAB countered inflationary pressures and tariff impacts through proactive pricing strategies ($29.4 million realized) and operational optimizations. However, a deeper DuPont analysis reveals that ESAB’s earnings quality warrants institutional scrutiny. In 2025, ESAB's inventory spiked by 19.3%, drastically outpacing its 3.7% revenue growth. Coupled with a reduction in credit loss allowances amidst geopolitical uncertainties, these metrics suggest potential working capital and earnings management risks that investors must monitor closely.

HDIN Viewpoint: The Institutional Perspective

From HDIN Research’s analytical vantage point, the 2025 landscape highlights a classic dichotomy in industrial sector positioning. ITW represents the ultimate "Value Defensive" asset. By strictly adhering to its 80/20 discipline, ITW actively manages cyclical headwinds, ensuring top-tier free cash flow conversion (~88%) and robust shareholder returns without over-leveraging its balance sheet.

ESAB, on the other hand, is an aggressive "Growth Elastic" play. Its success heavily depends on the EBXai system's ability to seamlessly integrate complex, high-tech acquisitions without breaking its tighter 4.9x interest coverage threshold. For stakeholders, the choice between ITW's impenetrable margin resilience and ESAB's aggressive TAM-expanding acquisitions will ultimately dictate portfolio beta in the impending industrial cycle.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com