2025 Beverage Giants: The Great Bifurcation of Growth and Digital Moats

Date : 2026-02-24

Reading : 530

The global beverage sector in 2025 has reached a critical inflection point. Facing a complex macroeconomic environment characterized by cyclical headwinds, persistent commodity inflation, and shifting consumer demographics, legacy market leaders and emerging functional challengers are executing radically different survival and expansion playbooks.

A deep dive into the 2025 financial disclosures of five major players—Coca-Cola, PepsiCo, Nestlé, BellRing Brands, and Vita Coco—reveals a definitive bifurcation in the industry. Traditional giants are leaning heavily into brand equity to enforce aggressive pricing initiatives, while agile, small-cap functional brands are successfully capturing genuine volume penetration. For institutional investors and industry strategists, understanding these shifting tectonic plates is paramount.

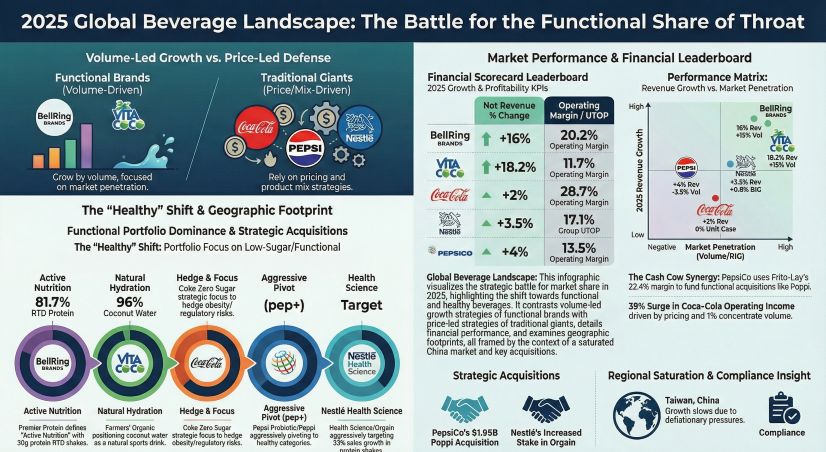

Figure 2025 Clobal Beverage Landscape: The Battle for the Functional Share of Throat

Strategic Moats: Brand Premium vs. Volume Penetration

Strategic Moats: Brand Premium vs. Volume Penetration

In 2025, revenue growth metrics unmask divergent underlying strategies. Traditional conglomerates have largely abandoned sheer volume expansion in favor of protecting gross margins through value-based pricing. PepsiCo’s North America Beverage (PBNA) division, for instance, engineered a 5% increase in effective net pricing to offset a 3.5% organic volume contraction. Similarly, Nestlé leveraged the inelasticity of its "billionaire brands" (such as Nescafé and Nespresso) to pass on soaring cocoa and coffee costs, registering a 6.6% pricing contribution against a marginal 0.7% real internal growth (RIG).

Conversely, functional innovators are redefining market share acquisition. BellRing Brands circumvented traditional marketing warfare by aligning strictly with the "active lifestyle" mega-trend. Driven by its Premier Protein portfolio, the company achieved a staggering 15% volume surge. Remarkably, BellRing accomplished this on a minimal 3.25% marketing intensity, demonstrating that in the current consumer landscape, formulation and nutritional moats can yield significantly higher organic growth than legacy advertising spend.

Capital Allocation Efficiency: Subsidizing the Functional Pivot

The true operational genius of the 2025 beverage giants lies in their cross-category capital allocation. Mature portfolios are strategically utilizing highly profitable "cash cows" to fund high-risk, high-reward acquisitions in the functional space.

* The "Salty Funds Sweet" Synergy: PepsiCo’s Frito-Lay North America remains the ultimate profit engine, boasting a 22.4% operating margin. This immense cash generation provides the financial buffer necessary for PepsiCo to aggressively reshape its beverage portfolio, exemplified by its $1.95 billion acquisition of probiotic soda brand poppi, directly addressing the consumer pivot toward gut health.

* Asset-Light Leverage: Coca-Cola’s focus on its high-margin concentrate operations (which drove 59% of net revenue while supporting 85% of global volume) sustained its robust 61.6% gross margin. This capital efficiency enabled the company to execute its $6.1 billion final milestone payment for the fairlife dairy acquisition, securing a dominant position in the value-added protein sector.

* Working Capital Supremacy: Operational efficiency remains a definitive moat. PepsiCo demonstrated extraordinary supply chain leverage in 2025, maintaining a negative cash conversion cycle (-48.9 days). By stretching its days payable outstanding (DPO) to nearly 100 days while rapidly turning over inventory, PepsiCo is effectively funding its global expansion using supplier capital.

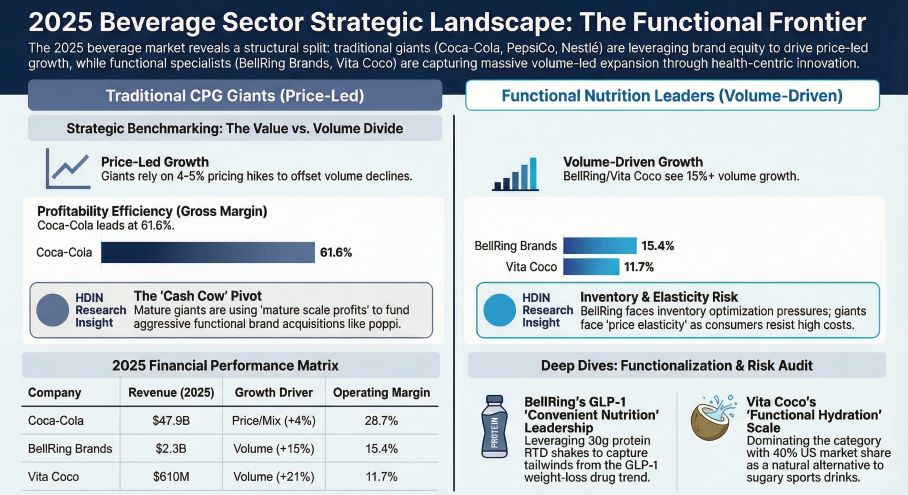

Figure 2025 Beverage Sector Strategic Landscape: The Functional Frontier

Digital Transformation: AI as the New Barrier to Entry

Digital Transformation: AI as the New Barrier to Entry

With global physical volume growth approaching a ceiling, top-tier FMCG companies have pivoted their capital expenditures from traditional scale expansion to operational digitization. Artificial Intelligence is no longer a buzzword; it is a structural barrier to entry.

Nestlé leads the pack in generative AI adoption, utilizing "digital twins" to rapidly and cost-effectively deploy e-commerce visual assets, driving its digital channel sales to over 20% of total revenue. Simultaneously, PepsiCo has deployed AI-powered virtual sales assistants, automating 40% of routine sales tasks to drastically improve its return on promotional spend. This industry-wide technological arms race signals a critical evolution: future market leadership will belong to companies that can predict consumer shifts and execute hyper-localized pricing adjustments in real time.

Sector Positioning & Cyclical Headwinds

Despite these advancements, the industry faces severe structural vulnerabilities that demand rigorous risk auditing.

* Impairment Risks: Aggressive historical M&A activity is showing cracks. Coca-Cola recognized an additional $960 million impairment on the BodyArmor trademark, while PepsiCo recorded a staggering $1.9 billion writedown on its Rockstar brand. These massive non-cash charges underscore the volatility of consumer loyalty in non-core functional segments.

* Geopolitical and Deflationary Pressures: The Greater China market presents a persistent deflationary environment, prompting sharp strategic recalibrations. Nestlé reported a 4.6% local currency sales decline in the region, driven by weak consumer sentiment and channel inventory corrections.

* Regulatory Squeeze: Rising ESG compliance costs—ranging from Extended Producer Responsibility (EPR) packaging laws to global sugar taxes—are structurally elevating the floor for cost of goods sold (COGS), disproportionately threatening single-product players like Vita Coco, whose supply chains are highly concentrated.

HDIN Viewpoint

Based on our proprietary analysis, HDIN Research concludes that the era of relying on simple demographic expansion and ubiquitous distribution is over. The 2025 financial landscape confirms that the most resilient entities are those transitioning from traditional beverage manufacturers into "Digital FMCG Platforms" and "Health Science Innovators."

Investors and stakeholders must look beyond top-line revenue. The true markers of long-term viability in this sector are the ability to utilize mature cash flows to subsidize functional M&A, the agility to offset commodity inflation through AI-driven supply chain efficiencies, and the discipline to maintain robust capital allocation amidst shifting geopolitical sands.

Presentation Download

To dive deeper into the financial metrics, forensic accounting audits, and strategic forecasts of these five industry leaders, please click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

A deep dive into the 2025 financial disclosures of five major players—Coca-Cola, PepsiCo, Nestlé, BellRing Brands, and Vita Coco—reveals a definitive bifurcation in the industry. Traditional giants are leaning heavily into brand equity to enforce aggressive pricing initiatives, while agile, small-cap functional brands are successfully capturing genuine volume penetration. For institutional investors and industry strategists, understanding these shifting tectonic plates is paramount.

Figure 2025 Clobal Beverage Landscape: The Battle for the Functional Share of Throat

Strategic Moats: Brand Premium vs. Volume PenetrationIn 2025, revenue growth metrics unmask divergent underlying strategies. Traditional conglomerates have largely abandoned sheer volume expansion in favor of protecting gross margins through value-based pricing. PepsiCo’s North America Beverage (PBNA) division, for instance, engineered a 5% increase in effective net pricing to offset a 3.5% organic volume contraction. Similarly, Nestlé leveraged the inelasticity of its "billionaire brands" (such as Nescafé and Nespresso) to pass on soaring cocoa and coffee costs, registering a 6.6% pricing contribution against a marginal 0.7% real internal growth (RIG).

Conversely, functional innovators are redefining market share acquisition. BellRing Brands circumvented traditional marketing warfare by aligning strictly with the "active lifestyle" mega-trend. Driven by its Premier Protein portfolio, the company achieved a staggering 15% volume surge. Remarkably, BellRing accomplished this on a minimal 3.25% marketing intensity, demonstrating that in the current consumer landscape, formulation and nutritional moats can yield significantly higher organic growth than legacy advertising spend.

Capital Allocation Efficiency: Subsidizing the Functional Pivot

The true operational genius of the 2025 beverage giants lies in their cross-category capital allocation. Mature portfolios are strategically utilizing highly profitable "cash cows" to fund high-risk, high-reward acquisitions in the functional space.

* The "Salty Funds Sweet" Synergy: PepsiCo’s Frito-Lay North America remains the ultimate profit engine, boasting a 22.4% operating margin. This immense cash generation provides the financial buffer necessary for PepsiCo to aggressively reshape its beverage portfolio, exemplified by its $1.95 billion acquisition of probiotic soda brand poppi, directly addressing the consumer pivot toward gut health.

* Asset-Light Leverage: Coca-Cola’s focus on its high-margin concentrate operations (which drove 59% of net revenue while supporting 85% of global volume) sustained its robust 61.6% gross margin. This capital efficiency enabled the company to execute its $6.1 billion final milestone payment for the fairlife dairy acquisition, securing a dominant position in the value-added protein sector.

* Working Capital Supremacy: Operational efficiency remains a definitive moat. PepsiCo demonstrated extraordinary supply chain leverage in 2025, maintaining a negative cash conversion cycle (-48.9 days). By stretching its days payable outstanding (DPO) to nearly 100 days while rapidly turning over inventory, PepsiCo is effectively funding its global expansion using supplier capital.

Figure 2025 Beverage Sector Strategic Landscape: The Functional Frontier

Digital Transformation: AI as the New Barrier to EntryWith global physical volume growth approaching a ceiling, top-tier FMCG companies have pivoted their capital expenditures from traditional scale expansion to operational digitization. Artificial Intelligence is no longer a buzzword; it is a structural barrier to entry.

Nestlé leads the pack in generative AI adoption, utilizing "digital twins" to rapidly and cost-effectively deploy e-commerce visual assets, driving its digital channel sales to over 20% of total revenue. Simultaneously, PepsiCo has deployed AI-powered virtual sales assistants, automating 40% of routine sales tasks to drastically improve its return on promotional spend. This industry-wide technological arms race signals a critical evolution: future market leadership will belong to companies that can predict consumer shifts and execute hyper-localized pricing adjustments in real time.

Sector Positioning & Cyclical Headwinds

Despite these advancements, the industry faces severe structural vulnerabilities that demand rigorous risk auditing.

* Impairment Risks: Aggressive historical M&A activity is showing cracks. Coca-Cola recognized an additional $960 million impairment on the BodyArmor trademark, while PepsiCo recorded a staggering $1.9 billion writedown on its Rockstar brand. These massive non-cash charges underscore the volatility of consumer loyalty in non-core functional segments.

* Geopolitical and Deflationary Pressures: The Greater China market presents a persistent deflationary environment, prompting sharp strategic recalibrations. Nestlé reported a 4.6% local currency sales decline in the region, driven by weak consumer sentiment and channel inventory corrections.

* Regulatory Squeeze: Rising ESG compliance costs—ranging from Extended Producer Responsibility (EPR) packaging laws to global sugar taxes—are structurally elevating the floor for cost of goods sold (COGS), disproportionately threatening single-product players like Vita Coco, whose supply chains are highly concentrated.

HDIN Viewpoint

Based on our proprietary analysis, HDIN Research concludes that the era of relying on simple demographic expansion and ubiquitous distribution is over. The 2025 financial landscape confirms that the most resilient entities are those transitioning from traditional beverage manufacturers into "Digital FMCG Platforms" and "Health Science Innovators."

Investors and stakeholders must look beyond top-line revenue. The true markers of long-term viability in this sector are the ability to utilize mature cash flows to subsidize functional M&A, the agility to offset commodity inflation through AI-driven supply chain efficiencies, and the discipline to maintain robust capital allocation amidst shifting geopolitical sands.

Presentation Download

To dive deeper into the financial metrics, forensic accounting audits, and strategic forecasts of these five industry leaders, please click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com