Beyond the Pump: How Global Fluid Giants are Engineering Margin Expansion in 2025

Date : 2026-02-25

Reading : 265

The industrial fluid management sector has officially crossed the Rubicon, transitioning from a volume-driven hardware market into a high-margin ecosystem of predictive maintenance, digital lifecycles, and niche precision engineering. Based on a deep-dive analysis of the 2025 financial disclosures of five industry behemoths—IDEX, Dover, Ingersoll Rand, ITT Inc., and Flowserve—HDIN Research has identified a stark bifurcation in profitability.

The underlying narrative is clear: operational efficiency and strategic exposure to secular tailwinds (such as AI data centers, biopharma, and energy transition) are heavily outweighing traditional scale. Here is how the top players are fortifying their strategic moats against cyclical headwinds.

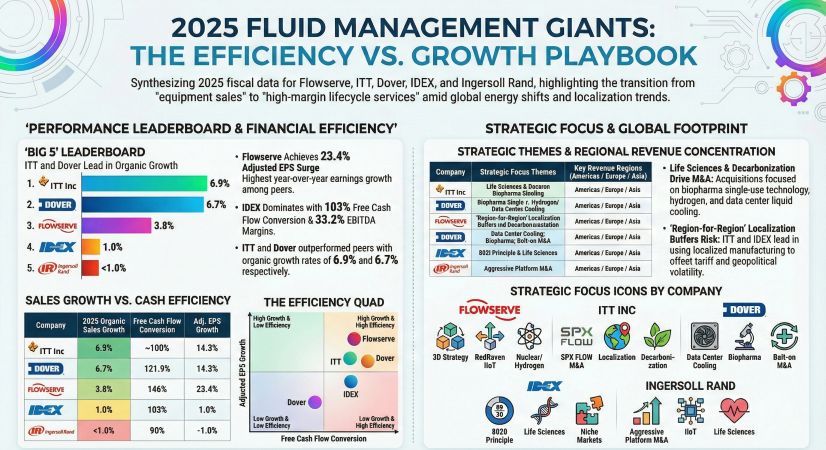

Figure 2025 FLUID MANAGEMENT CIANTS: THE EFFICIENCY VS. GROWTH PLAYBOOK

Financial Health: The Divergence in Capital Allocation Efficiency

Financial Health: The Divergence in Capital Allocation Efficiency

Stripping away acquisition-related noise and intangible amortization reveals a tiered reality in core profitability. IDEX (Fluid & Metering Technologies) and Dover (Pumps & Process Solutions) have firmly established themselves in the elite Tier-1 bracket, boasting Adjusted EBITDA margins of 33.2% and 30.3%, respectively.

What is driving this profitability surge? It is not merely cost-cutting, but aggressive capital allocation efficiency. IDEX operates on a rigorous "80/20 principle," commanding immense pricing power in highly fragmented, non-commoditized niche markets. This efficiency translates directly into a best-in-class working capital profile, with IDEX achieving a Days Sales Outstanding (DSO) of just 55 days and an operating cash flow (OCF) conversion rate of 141% relative to net income. IDEX has proven to be an unparalleled cash-generating machine.

Conversely, heavy-duty industrial pump manufacturers like Flowserve (18.6% operating margin) navigate a longer DSO (76 days) due to large-scale, capital-intensive engineering projects. However, Flowserve is actively executing an "improved selective bidding" strategy, shedding low-margin hardware contracts to prioritize high-yield aftermarket engagements.

Strategic Pivots: Aftermarket Dynamics and the Digital Moat

The most resilient defense against macroeconomic cyclicality is recurring revenue. Across the five giants, aftermarket and service revenues now constitute a structural baseline of 36% to 53% of total earnings.

Flowserve leads this metric, with aftermarket revenues comprising 53% of its mix. The strategic implication is profound: by leveraging its RedRaven IIoT platform, Flowserve is monetizing data. This shift transforms one-off equipment sales into "Value-in-Use" contracts featuring remote diagnostics and fluid dynamics optimization.

Similarly, Dover is actively insulating itself from traditional industrial volatility. While traditional automotive-exposed segments face headwinds, Dover’s PPS division generated 6.7% organic growth by pivoting toward data center liquid cooling thermal connectors and biopharma single-use technologies. The switching costs for these highly sensitive, mission-critical components are astronomical, granting Dover an enduring pricing moat.

Sector Positioning: Geopolitical Hedging and M&A Risks

In 2025, robust supply chain localization transitioned from a buzzword to a quantifiable financial asset. ITT Inc. set the benchmark with its aggressive "region-for-region" and local-for-local manufacturing strategy. By shifting production capabilities directly into key markets—expanding its footprint across China, Europe, and the Middle East—ITT successfully neutralized tariff volatility and realized pricing actions that more than offset cost inflation.

However, the pursuit of growth through mergers and acquisitions (M&A) carries distinct risks in a high-interest-rate environment. Dover and IDEX have favored "bolt-on" acquisitions to quietly capture niche capabilities without bloating their balance sheets. In contrast, Ingersoll Rand has pursued an aggressive platform-consolidation strategy. While this rapidly expands their footprint in life sciences and clean energy, it has resulted in goodwill comprising nearly 55% of its Precision & Science Technologies (P&ST) segment assets. The recent $230 million non-cash goodwill impairment reported by Ingersoll Rand underscores the latent risks inherent in high-premium roll-ups if synergy execution falters.

HDIN Viewpoint

From an institutional perspective, the 2026 outlook hinges on order visibility and technological premium. HDIN Research assesses that Flowserve and ITT possess the highest near-term revenue certainty. Flowserve’s Book-to-Bill ratio of 1.012, combined with a backlog where 76% is executable in 2026, offers a highly visible runway, particularly as its higher-margin digital service segments scale.

Meanwhile, companies like Dover and IDEX command the highest "quality of earnings." Their pivot toward cryogenic clean energy, AI liquid cooling, and semiconductor precision represents the future blueprint for the industry. Investors and operators alike must recognize that the fluid giant of tomorrow is no longer a manufacturer of pumps, but a critical architect of high-tech thermal and fluid ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

The underlying narrative is clear: operational efficiency and strategic exposure to secular tailwinds (such as AI data centers, biopharma, and energy transition) are heavily outweighing traditional scale. Here is how the top players are fortifying their strategic moats against cyclical headwinds.

Figure 2025 FLUID MANAGEMENT CIANTS: THE EFFICIENCY VS. GROWTH PLAYBOOK

Financial Health: The Divergence in Capital Allocation EfficiencyStripping away acquisition-related noise and intangible amortization reveals a tiered reality in core profitability. IDEX (Fluid & Metering Technologies) and Dover (Pumps & Process Solutions) have firmly established themselves in the elite Tier-1 bracket, boasting Adjusted EBITDA margins of 33.2% and 30.3%, respectively.

What is driving this profitability surge? It is not merely cost-cutting, but aggressive capital allocation efficiency. IDEX operates on a rigorous "80/20 principle," commanding immense pricing power in highly fragmented, non-commoditized niche markets. This efficiency translates directly into a best-in-class working capital profile, with IDEX achieving a Days Sales Outstanding (DSO) of just 55 days and an operating cash flow (OCF) conversion rate of 141% relative to net income. IDEX has proven to be an unparalleled cash-generating machine.

Conversely, heavy-duty industrial pump manufacturers like Flowserve (18.6% operating margin) navigate a longer DSO (76 days) due to large-scale, capital-intensive engineering projects. However, Flowserve is actively executing an "improved selective bidding" strategy, shedding low-margin hardware contracts to prioritize high-yield aftermarket engagements.

Strategic Pivots: Aftermarket Dynamics and the Digital Moat

The most resilient defense against macroeconomic cyclicality is recurring revenue. Across the five giants, aftermarket and service revenues now constitute a structural baseline of 36% to 53% of total earnings.

Flowserve leads this metric, with aftermarket revenues comprising 53% of its mix. The strategic implication is profound: by leveraging its RedRaven IIoT platform, Flowserve is monetizing data. This shift transforms one-off equipment sales into "Value-in-Use" contracts featuring remote diagnostics and fluid dynamics optimization.

Similarly, Dover is actively insulating itself from traditional industrial volatility. While traditional automotive-exposed segments face headwinds, Dover’s PPS division generated 6.7% organic growth by pivoting toward data center liquid cooling thermal connectors and biopharma single-use technologies. The switching costs for these highly sensitive, mission-critical components are astronomical, granting Dover an enduring pricing moat.

Sector Positioning: Geopolitical Hedging and M&A Risks

In 2025, robust supply chain localization transitioned from a buzzword to a quantifiable financial asset. ITT Inc. set the benchmark with its aggressive "region-for-region" and local-for-local manufacturing strategy. By shifting production capabilities directly into key markets—expanding its footprint across China, Europe, and the Middle East—ITT successfully neutralized tariff volatility and realized pricing actions that more than offset cost inflation.

However, the pursuit of growth through mergers and acquisitions (M&A) carries distinct risks in a high-interest-rate environment. Dover and IDEX have favored "bolt-on" acquisitions to quietly capture niche capabilities without bloating their balance sheets. In contrast, Ingersoll Rand has pursued an aggressive platform-consolidation strategy. While this rapidly expands their footprint in life sciences and clean energy, it has resulted in goodwill comprising nearly 55% of its Precision & Science Technologies (P&ST) segment assets. The recent $230 million non-cash goodwill impairment reported by Ingersoll Rand underscores the latent risks inherent in high-premium roll-ups if synergy execution falters.

HDIN Viewpoint

From an institutional perspective, the 2026 outlook hinges on order visibility and technological premium. HDIN Research assesses that Flowserve and ITT possess the highest near-term revenue certainty. Flowserve’s Book-to-Bill ratio of 1.012, combined with a backlog where 76% is executable in 2026, offers a highly visible runway, particularly as its higher-margin digital service segments scale.

Meanwhile, companies like Dover and IDEX command the highest "quality of earnings." Their pivot toward cryogenic clean energy, AI liquid cooling, and semiconductor precision represents the future blueprint for the industry. Investors and operators alike must recognize that the fluid giant of tomorrow is no longer a manufacturer of pumps, but a critical architect of high-tech thermal and fluid ecosystems.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com