ExxonMobil vs. Phillips 66: Decoding 2025 Strategic Moats and Capital Allocation Efficiency

Date : 2026-02-25

Reading : 339

The FY2025 financial landscape for global energy majors reveals a definitive divergence in value-creation models. Based on a deep-dive analysis by HDIN Research, the contrasting financial architecture of ExxonMobil (NYSE: XOM) and Phillips 66 (NYSE: PSX) underscores two distinct paradigms of sector positioning: the resource-driven behemoth versus the efficiency-driven downstream expert.

Rather than merely generating windfall revenues in a volatile commodity environment, both titans have deployed radically different strategic moats to navigate cyclical headwinds, optimize capital allocation efficiency, and future-proof against an accelerating energy transition.

Figure Energy Giants 2025 integrated Resilience vs Refining Excellence

Sector Positioning: Resource Scale vs. Downstream Integration

Sector Positioning: Resource Scale vs. Downstream Integration

The core competitive divergence between XOM and PSX lies in their asset gravity.

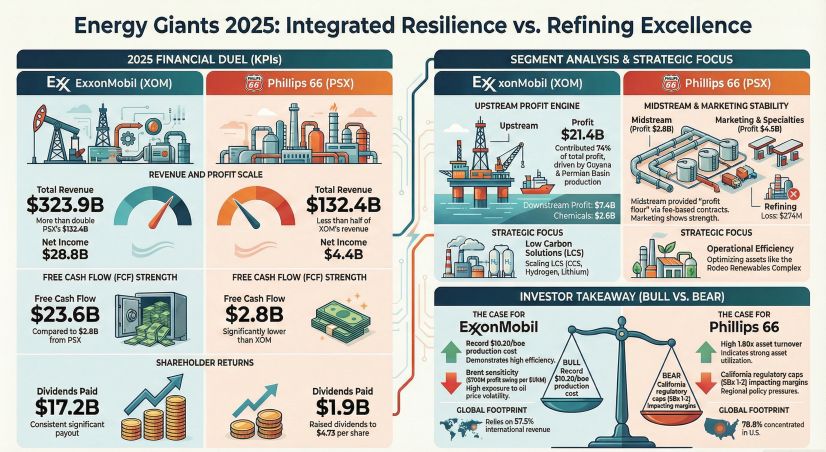

ExxonMobil’s ultimate strategic moat is its unparalleled upstream scale and asset quality. By the end of 2025, XOM’s proven reserves hit 19.3 billion oil-equivalent barrels (GOEB). The strategic implications are profound: driven by record outputs in Guyana (715,000 barrels/day) and the Permian Basin (1.6 million boe/day) following the Pioneer integration, XOM has driven its upstream unit production cost down to a remarkable $10.20/boe. This hyper-efficient cost structure acts as a structural defense mechanism, ensuring robust margin capture even during severe cyclical downturns.

Conversely, Phillips 66 operates without an upstream anchor, relying instead on its profound downstream and midstream agility. PSX’s logistics moat—anchored by 70,000 miles of pipeline—enables high-frequency trading and distribution. While XOM operates on a massive capital base with an asset turnover of 0.72x, PSX leverages a much leaner asset footprint to achieve an exceptional asset turnover of 1.80x. Despite raw material cost squeezes, PSX's meticulous crack spread management and high utilization rates (94%) allowed it to capture a global realized refining margin of $10.88/bbl in 2025.

Capital Allocation Efficiency & Financial Agility

When evaluating financial health and cash-generation profiles, the distinction between a "Beta" player and an "Alpha" player becomes evident.

ExxonMobil (The Beta Powerhouse): Highly sensitive to crude price fluctuations ($700 million profit impact per $1/bbl Brent change), XOM utilizes its immense scale as a natural hedge. Generating a staggering $52 billion in operating cash flow (CFO) in 2025, XOM demonstrates absolute dominance in capital allocation. Maintaining an ultra-low net debt ratio of 11.0% and an interest coverage ratio exceeding 68x, XOM comfortably executed $20.3 billion in share buybacks and $17.2 billion in dividends. We estimate its free cash flow (FCF) breakeven point sits securely around $40-$45/bbl, providing an almost impregnable safety net.

Phillips 66 (The Alpha Tactician): PSX’s profitability relies less on macro oil prices and more on market arbitrage and fee-based midstream contracts. Delivering $5 billion in CFO, PSX compensates for its higher leverage (39% total debt-to-capital ratio) through disciplined capital distribution, explicitly committing to return over 50% of its CFO to shareholders. Through strategic asset rationalization—such as divesting European retail assets for $3.5 billion—PSX actively optimizes its balance sheet while capturing seasonal market volatility through agile derivative hedging.

Strategic Pivots: Industrial Decarbonization vs. Molecular Conversion

Both energy giants are aggressively addressing the energy transition, but their pathways are tailored to their existing operational DNA.

XOM is championing industrial-scale decarbonization. Through its Low Carbon Solutions (LCS) unit, XOM is leveraging its massive subterranean engineering capabilities to commercialize Carbon Capture and Storage (CCS), hydrogen, and lithium extraction. Strategically, XOM factors in a proxy carbon price of $150/mt by 2050 into its investment models. Furthermore, XOM continues to optimize its global footprint, notably operating its wholly-owned high-performance petrochemical complex in Huizhou, China, focusing on material innovation to reduce resource consumption.

PSX, meanwhile, focuses on molecular conversion and terminal market transition. The transformation of its San Francisco refinery into the Rodeo Renewable Energy Complex—capable of processing 50,000 barrels/day of renewable feedstocks into Sustainable Aviation Fuel (SAF) and renewable diesel—is a testament to this strategy. PSX is directly addressing Scope 3 emissions by pivoting its distribution networks toward the EV infrastructure and battery materials (e.g., NOVONIX).

Regulatory Headwinds and Industry Outlook

Both entities face escalating climate litigation risks and stringent ESG disclosure scrutiny, including potential "greenwashing" torts. However, regulatory geography plays a crucial role. PSX's heavy exposure to California's aggressive regulatory environment (such as the SBx 1-2 margin cap legislation) has directly forced the idling and planned redevelopment of its Los Angeles refinery. XOM’s risks are more globally dispersed, centering around carbon pricing compliance (e.g., EU ETS) and the broader policy viability of its net-zero 2050 ambitions.

HDIN Viewpoint

From the analytical lens of HDIN Research, ExxonMobil and Phillips 66 offer mutually exclusive value propositions. XOM is the ultimate "resource-driven behemoth." Its deep integration, low-cost barrels in Guyana, and robust petrochemical operations globally (including its strategic presence in the Greater China market) make it the premier choice for investors seeking absolute balance sheet safety and a definitive inflation hedge.

Phillips 66, the "efficiency-driven expert," operates with surgical precision. For stakeholders prioritizing stringent capital allocation discipline, high asset turnover, and agile downstream arbitrage in the face of cyclical headwinds, PSX presents a highly compelling, yield-focused architecture.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Rather than merely generating windfall revenues in a volatile commodity environment, both titans have deployed radically different strategic moats to navigate cyclical headwinds, optimize capital allocation efficiency, and future-proof against an accelerating energy transition.

Figure Energy Giants 2025 integrated Resilience vs Refining Excellence

Sector Positioning: Resource Scale vs. Downstream IntegrationThe core competitive divergence between XOM and PSX lies in their asset gravity.

ExxonMobil’s ultimate strategic moat is its unparalleled upstream scale and asset quality. By the end of 2025, XOM’s proven reserves hit 19.3 billion oil-equivalent barrels (GOEB). The strategic implications are profound: driven by record outputs in Guyana (715,000 barrels/day) and the Permian Basin (1.6 million boe/day) following the Pioneer integration, XOM has driven its upstream unit production cost down to a remarkable $10.20/boe. This hyper-efficient cost structure acts as a structural defense mechanism, ensuring robust margin capture even during severe cyclical downturns.

Conversely, Phillips 66 operates without an upstream anchor, relying instead on its profound downstream and midstream agility. PSX’s logistics moat—anchored by 70,000 miles of pipeline—enables high-frequency trading and distribution. While XOM operates on a massive capital base with an asset turnover of 0.72x, PSX leverages a much leaner asset footprint to achieve an exceptional asset turnover of 1.80x. Despite raw material cost squeezes, PSX's meticulous crack spread management and high utilization rates (94%) allowed it to capture a global realized refining margin of $10.88/bbl in 2025.

Capital Allocation Efficiency & Financial Agility

When evaluating financial health and cash-generation profiles, the distinction between a "Beta" player and an "Alpha" player becomes evident.

ExxonMobil (The Beta Powerhouse): Highly sensitive to crude price fluctuations ($700 million profit impact per $1/bbl Brent change), XOM utilizes its immense scale as a natural hedge. Generating a staggering $52 billion in operating cash flow (CFO) in 2025, XOM demonstrates absolute dominance in capital allocation. Maintaining an ultra-low net debt ratio of 11.0% and an interest coverage ratio exceeding 68x, XOM comfortably executed $20.3 billion in share buybacks and $17.2 billion in dividends. We estimate its free cash flow (FCF) breakeven point sits securely around $40-$45/bbl, providing an almost impregnable safety net.

Phillips 66 (The Alpha Tactician): PSX’s profitability relies less on macro oil prices and more on market arbitrage and fee-based midstream contracts. Delivering $5 billion in CFO, PSX compensates for its higher leverage (39% total debt-to-capital ratio) through disciplined capital distribution, explicitly committing to return over 50% of its CFO to shareholders. Through strategic asset rationalization—such as divesting European retail assets for $3.5 billion—PSX actively optimizes its balance sheet while capturing seasonal market volatility through agile derivative hedging.

Strategic Pivots: Industrial Decarbonization vs. Molecular Conversion

Both energy giants are aggressively addressing the energy transition, but their pathways are tailored to their existing operational DNA.

XOM is championing industrial-scale decarbonization. Through its Low Carbon Solutions (LCS) unit, XOM is leveraging its massive subterranean engineering capabilities to commercialize Carbon Capture and Storage (CCS), hydrogen, and lithium extraction. Strategically, XOM factors in a proxy carbon price of $150/mt by 2050 into its investment models. Furthermore, XOM continues to optimize its global footprint, notably operating its wholly-owned high-performance petrochemical complex in Huizhou, China, focusing on material innovation to reduce resource consumption.

PSX, meanwhile, focuses on molecular conversion and terminal market transition. The transformation of its San Francisco refinery into the Rodeo Renewable Energy Complex—capable of processing 50,000 barrels/day of renewable feedstocks into Sustainable Aviation Fuel (SAF) and renewable diesel—is a testament to this strategy. PSX is directly addressing Scope 3 emissions by pivoting its distribution networks toward the EV infrastructure and battery materials (e.g., NOVONIX).

Regulatory Headwinds and Industry Outlook

Both entities face escalating climate litigation risks and stringent ESG disclosure scrutiny, including potential "greenwashing" torts. However, regulatory geography plays a crucial role. PSX's heavy exposure to California's aggressive regulatory environment (such as the SBx 1-2 margin cap legislation) has directly forced the idling and planned redevelopment of its Los Angeles refinery. XOM’s risks are more globally dispersed, centering around carbon pricing compliance (e.g., EU ETS) and the broader policy viability of its net-zero 2050 ambitions.

HDIN Viewpoint

From the analytical lens of HDIN Research, ExxonMobil and Phillips 66 offer mutually exclusive value propositions. XOM is the ultimate "resource-driven behemoth." Its deep integration, low-cost barrels in Guyana, and robust petrochemical operations globally (including its strategic presence in the Greater China market) make it the premier choice for investors seeking absolute balance sheet safety and a definitive inflation hedge.

Phillips 66, the "efficiency-driven expert," operates with surgical precision. For stakeholders prioritizing stringent capital allocation discipline, high asset turnover, and agile downstream arbitrage in the face of cyclical headwinds, PSX presents a highly compelling, yield-focused architecture.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com