Applied Materials (AMAT) FY2025 Teardown: How AI Tailwinds and Subscription Moats Offset Geopolitical Friction

Date : 2026-02-25

Reading : 419

Applied Materials (AMAT) navigated a highly complex FY2025, balancing the structural supercycle of artificial intelligence (AI) and High-Bandwidth Memory (HBM) against mounting regulatory friction. According to HDIN Research's deep-dive analysis of AMAT’s Form 10-K, the company is undergoing a fundamental business model transition. While top-line resilience remains intact, shifting global trade policies, asymmetric regulatory burdens, and aggressive R&D infrastructure investments are fundamentally reshaping its margin profile and regional dependencies.

Figure Applied Materials (AMAT) FY2025 Performance: Navigating Geopolitical Shifts through Al innovation

Capital Allocation Efficiency Amid Cyclical Headwinds

Capital Allocation Efficiency Amid Cyclical Headwinds

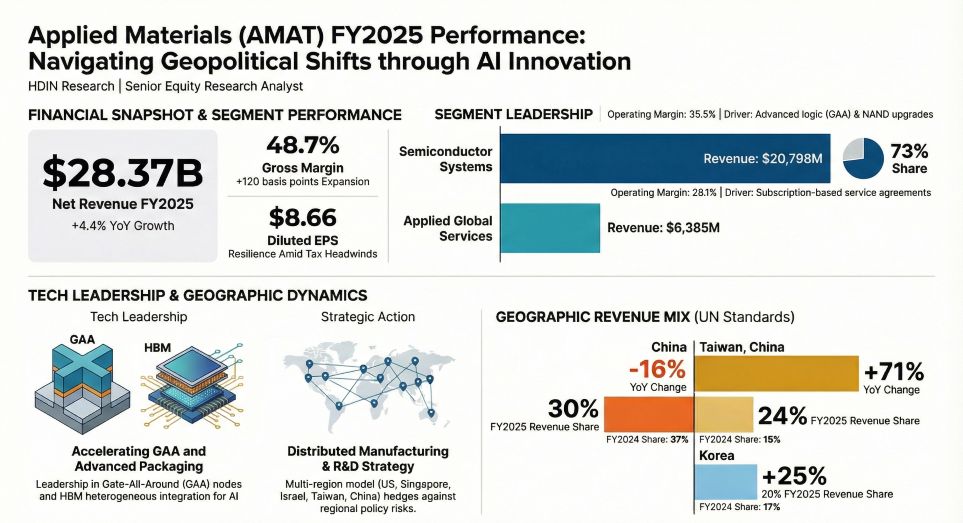

On the surface, AMAT demonstrated steady operational execution with FY2025 net revenue reaching $28.37 billion (+4.4% YoY). Gross margins expanded by 1.2 percentage points to 48.7%, driven by a favorable product mix and optimized production costs.

However, the strategic implications lie beneath the top-line data. Free cash flow (FCF) contracted by 23.9% to $5.7 billion. This compression is not a sign of operational weakness, but rather a deliberate exercise in capital allocation efficiency. AMAT nearly doubled its CapEx to $2.26 billion—heavily funding infrastructure like the new EPIC Center—to secure its position as the "Tool-of-Record" for next-generation nodes. Furthermore, profitability faced cyclical headwinds from a spiked effective tax rate of 24.5% (up from 12.0%), primarily due to the revaluation of Singapore tax incentives and CAMT valuation allowances. AMAT is consciously absorbing short-term margin pressures to cement its long-term R&D supremacy.

Strategic Moats: The AGS Subscription Pivot

To insulate the business from the inherent cyclicality of the Wafer Fab Equipment (WFE) market, AMAT is aggressively leveraging its Applied Global Services (AGS) division. Generating $6.39 billion in revenue with a robust 28.1% operating margin, AGS is the company's definitive stabilization engine.

The strategic pivot here is the transition toward a subscription-based model. By locking clients into long-term service agreements for maintenance, parts, and factory automation software, AMAT has built a formidable backlog of $7.14 billion within AGS alone (accounting for 48% of the company's total backlog). This high-visibility, predictable cash flow stream is effectively transforming AMAT from a cyclical hardware vendor into a highly sticky, integrated "equipment-as-a-service" platform.

Sector Positioning & Geopolitical Headwinds

Regional revenue shifts in FY2025 highlight a dramatic realignment in the global semiconductor supply chain. Sector positioning in advanced packaging and Gate-All-Around (GAA) 3D architectures drove a 71% revenue surge in Taiwan (now 24% of total revenue) and a 25% increase in Korea. Leading foundries and memory manufacturers are heavily deploying capital into 7nm/below nodes and HBM capacities, directly benefiting AMAT's specialized materials engineering portfolio.

Conversely, China revenues contracted by 16%, dropping to 30% of total revenue. US export controls on critical semiconductor technology have introduced severe market access restrictions and compliance costs. This geopolitical headwind has created an asymmetric competitive environment, inadvertently incentivizing Chinese domestic equipment substitution while empowering international rivals unburdened by US restrictions. To optimize organizational efficiency and defend margins against these geopolitical disruptions, AMAT initiated a targeted global restructuring plan, reducing its workforce by 4% to ensure lean agility.

HDIN Viewpoint: Navigating the AI Dividend

From an institutional perspective, HDIN Research views AMAT’s FY2025 as a definitive "positioning year." The management team's decision to tie executive compensation directly to Economic Profit and Total Shareholder Return (TSR) signals a rigorous focus on sustainable value creation. Their heavy capital deployment into R&D and the defensive pivot toward AGS subscription services are textbook strategic moats designed to capture the AI materials engineering dividend.

However, moving forward, the primary risk vector is not technological, but regulatory. Investors and supply-chain strategists must closely monitor the ongoing DOJ, BIS, and SEC scrutiny regarding export compliance, as well as potential supply chain chokepoints involving rare earth mineral export controls from China. AMAT's ultimate success in the coming cycle relies heavily on sustaining its architectural lead in heterogenous integration while ruthlessly mitigating geographic concentration risks.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Applied Materials (AMAT) FY2025 Performance: Navigating Geopolitical Shifts through Al innovation

Capital Allocation Efficiency Amid Cyclical HeadwindsOn the surface, AMAT demonstrated steady operational execution with FY2025 net revenue reaching $28.37 billion (+4.4% YoY). Gross margins expanded by 1.2 percentage points to 48.7%, driven by a favorable product mix and optimized production costs.

However, the strategic implications lie beneath the top-line data. Free cash flow (FCF) contracted by 23.9% to $5.7 billion. This compression is not a sign of operational weakness, but rather a deliberate exercise in capital allocation efficiency. AMAT nearly doubled its CapEx to $2.26 billion—heavily funding infrastructure like the new EPIC Center—to secure its position as the "Tool-of-Record" for next-generation nodes. Furthermore, profitability faced cyclical headwinds from a spiked effective tax rate of 24.5% (up from 12.0%), primarily due to the revaluation of Singapore tax incentives and CAMT valuation allowances. AMAT is consciously absorbing short-term margin pressures to cement its long-term R&D supremacy.

Strategic Moats: The AGS Subscription Pivot

To insulate the business from the inherent cyclicality of the Wafer Fab Equipment (WFE) market, AMAT is aggressively leveraging its Applied Global Services (AGS) division. Generating $6.39 billion in revenue with a robust 28.1% operating margin, AGS is the company's definitive stabilization engine.

The strategic pivot here is the transition toward a subscription-based model. By locking clients into long-term service agreements for maintenance, parts, and factory automation software, AMAT has built a formidable backlog of $7.14 billion within AGS alone (accounting for 48% of the company's total backlog). This high-visibility, predictable cash flow stream is effectively transforming AMAT from a cyclical hardware vendor into a highly sticky, integrated "equipment-as-a-service" platform.

Sector Positioning & Geopolitical Headwinds

Regional revenue shifts in FY2025 highlight a dramatic realignment in the global semiconductor supply chain. Sector positioning in advanced packaging and Gate-All-Around (GAA) 3D architectures drove a 71% revenue surge in Taiwan (now 24% of total revenue) and a 25% increase in Korea. Leading foundries and memory manufacturers are heavily deploying capital into 7nm/below nodes and HBM capacities, directly benefiting AMAT's specialized materials engineering portfolio.

Conversely, China revenues contracted by 16%, dropping to 30% of total revenue. US export controls on critical semiconductor technology have introduced severe market access restrictions and compliance costs. This geopolitical headwind has created an asymmetric competitive environment, inadvertently incentivizing Chinese domestic equipment substitution while empowering international rivals unburdened by US restrictions. To optimize organizational efficiency and defend margins against these geopolitical disruptions, AMAT initiated a targeted global restructuring plan, reducing its workforce by 4% to ensure lean agility.

HDIN Viewpoint: Navigating the AI Dividend

From an institutional perspective, HDIN Research views AMAT’s FY2025 as a definitive "positioning year." The management team's decision to tie executive compensation directly to Economic Profit and Total Shareholder Return (TSR) signals a rigorous focus on sustainable value creation. Their heavy capital deployment into R&D and the defensive pivot toward AGS subscription services are textbook strategic moats designed to capture the AI materials engineering dividend.

However, moving forward, the primary risk vector is not technological, but regulatory. Investors and supply-chain strategists must closely monitor the ongoing DOJ, BIS, and SEC scrutiny regarding export compliance, as well as potential supply chain chokepoints involving rare earth mineral export controls from China. AMAT's ultimate success in the coming cycle relies heavily on sustaining its architectural lead in heterogenous integration while ruthlessly mitigating geographic concentration risks.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com