The 2025 Metabolic Watershed: Moving Beyond the GLP-1 Duopoly

Date : 2026-02-26

Reading : 368

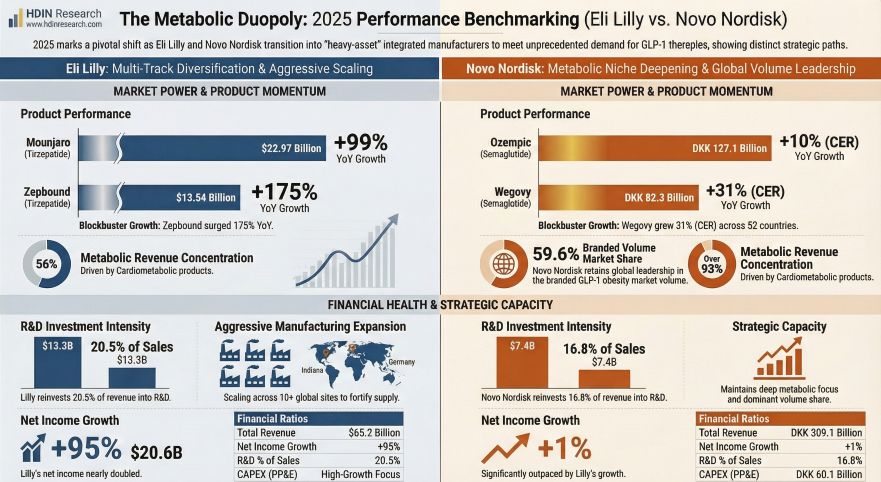

The 2025 fiscal year marks a structural turning point in the global metabolic drug arena. According to HDIN Research's deep-dive analysis, Eli Lilly has officially dethroned Novo Nordisk in flagship asset scale, with the Tirzepatide franchise generating $36.5 billion to surpass the Semaglutide portfolio’s $34.5 billion. However, this revenue milestone is merely the surface. A closer examination of their 2025 annual reports reveals a profound divergence in capital allocation efficiency, the construction of strategic moats, and preparedness for cyclical headwinds. The competition has fundamentally transitioned from a clinical product race to a full-value-chain saturation attack.

Figure The Metabolic Duopoly 2025 Performance Benchmarking (Eli Lilly vs Novo Nordisk)

Financial Health: Margin Expansion vs. Channel Taxes

Financial Health: Margin Expansion vs. Channel Taxes

While both pharmaceutical titans dominate the obesity and diabetes sectors, the underlying quality of their revenue growth dictates their long-term sector positioning. Eli Lilly posted a staggering 45% top-line surge, driven heavily by Zepbound’s 175% growth in the obesity segment. More importantly, Lilly maintained a remarkable $1.3 million revenue output per employee and expanded its gross margin to 83.0%.

Conversely, Novo Nordisk has entered a strategic consolidation phase, recording a more muted 6.4% revenue growth. The company is facing severe "channel taxes" in the U.S. market, with Gross-to-Net (GTN) concessions reaching 57.6%. To maintain its patient base against compounding pharmacies and aggressive Pharmacy Benefit Manager (PBM) negotiations, Novo is trading price for volume. This defensive posture, combined with heavy restructuring costs, compressed its gross margin down to 81.0%. The strategic implication is clear: Lilly is currently capturing high-margin incremental volume, while Novo Nordisk is paying a premium for market access and legacy preservation.

Capital Allocation Efficiency: Supply Chain Resiliency

The defining operational bottleneck of the GLP-1 era is manufacturing capacity. Both companies deployed unprecedented capital expenditures in 2025 to shatter their production ceilings, but their strategic deployment models sharply contrast.

Novo Nordisk executed a massive vertical integration strategy, allocating an $8.6 billion CAPEX budget and spending $11.7 billion to acquire Catalent’s fill-finish sites. While this internalizes critical supply chain nodes, it introduces profound integration risks and compliance hurdles, exposing the company to immediate margin dilution.

Eli Lilly, on the other hand, engineered a highly resilient "hybrid shield" model. Utilizing $7.8 billion in internal CAPEX to build proprietary API sites, Lilly simultaneously secured a $10 billion long-term "take-or-pay" CDMO lock-in. This agile capital allocation ensures strict internal quality control while retaining elastic external capacity to absorb demand shocks, granting Lilly superior supply chain resiliency without the drag of heavy-asset integration friction.

Strategic Pivots and Pipeline Moats

As the U.S. Inflation Reduction Act (IRA) looms, shortening the runway for premium pricing, both companies are rapidly fortifying their R&D pipelines to combat impending patent cliffs.

Lilly’s pipeline strategy revolves around generational leaps and cross-cycle risk hedging. Within metabolics, the company is advancing the triple-agonist Retatrutide and the oral small-molecule Orforglipron—a critical asset that circumvents the complex peptide cold-chain entirely, promising low marginal costs for global primary care penetration. Furthermore, Lilly leverages robust cash flows from its oncology and immunology portfolios, and its approved Alzheimer’s drug (Kisunla), creating a diversified moat insulated from metabolic pricing constraints.

Novo Nordisk’s strategy is rooted in deep vertical expansion into metabolic complications, securing approvals for cardiovascular (CVD) and MASH indications to maximize Semaglutide’s lifetime value. However, this creates intense concentration risk. The recent termination of its Alzheimer’s program and the underwhelming performance of its next-generation CagriSema—which failed to meet non-inferiority against Tirzepatide in head-to-head weight-loss trials (23% vs 25.5%)—leaves Novo highly dependent on a single-molecule foundation.

Cyclical Headwinds and Earnings Quality

Policy ceilings are transitioning from theoretical risks to tangible financial erosion. As IRA price negotiations bite, HDIN Research notes significant divergences in how both entities manage their balance sheets.

Novo Nordisk exhibits signs of earnings management through a reported $4.2 billion 340B pricing provision. The anticipated reversal of this provision in Q1 2026 acts as an accounting buffer, potentially smoothing over projected core business contractions (-5% to -13%). Meanwhile, Lilly's explosive growth warrants distinct audit scrutiny; a 61% surge in accounts receivable and a massive spike in inventory outpaced revenue growth, signaling potential channel-stuffing risks that could pressure 2026 cash conversion cycles if market penetration slows.

HDIN Viewpoint

HDIN Research views Eli Lilly as a "comprehensive outperformer." By leveraging its diversified innovation matrix, Lilly generates high-barrier cash flows to fund aggressive, multi-target GLP-1 dominance. Its agile supply chain and intergenerational pipeline leaps afford it superior downside protection against cyclical regulatory pricing shocks.

In contrast, Novo Nordisk acts as a "vertical integration specialist." While its deep entrenchment in cardiovascular and renal adjacencies provides a solid defensive base, the company's heavy reliance on costly manufacturing acquisitions, accounting buffers, and a single-molecule architecture suggests a protracted and capital-intensive transitional phase. For institutional investors, the 2025 data indicates that Lilly is engineered for premium market capture, whereas Novo is currently priced for cyclical defense.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure The Metabolic Duopoly 2025 Performance Benchmarking (Eli Lilly vs Novo Nordisk)

Financial Health: Margin Expansion vs. Channel TaxesWhile both pharmaceutical titans dominate the obesity and diabetes sectors, the underlying quality of their revenue growth dictates their long-term sector positioning. Eli Lilly posted a staggering 45% top-line surge, driven heavily by Zepbound’s 175% growth in the obesity segment. More importantly, Lilly maintained a remarkable $1.3 million revenue output per employee and expanded its gross margin to 83.0%.

Conversely, Novo Nordisk has entered a strategic consolidation phase, recording a more muted 6.4% revenue growth. The company is facing severe "channel taxes" in the U.S. market, with Gross-to-Net (GTN) concessions reaching 57.6%. To maintain its patient base against compounding pharmacies and aggressive Pharmacy Benefit Manager (PBM) negotiations, Novo is trading price for volume. This defensive posture, combined with heavy restructuring costs, compressed its gross margin down to 81.0%. The strategic implication is clear: Lilly is currently capturing high-margin incremental volume, while Novo Nordisk is paying a premium for market access and legacy preservation.

Capital Allocation Efficiency: Supply Chain Resiliency

The defining operational bottleneck of the GLP-1 era is manufacturing capacity. Both companies deployed unprecedented capital expenditures in 2025 to shatter their production ceilings, but their strategic deployment models sharply contrast.

Novo Nordisk executed a massive vertical integration strategy, allocating an $8.6 billion CAPEX budget and spending $11.7 billion to acquire Catalent’s fill-finish sites. While this internalizes critical supply chain nodes, it introduces profound integration risks and compliance hurdles, exposing the company to immediate margin dilution.

Eli Lilly, on the other hand, engineered a highly resilient "hybrid shield" model. Utilizing $7.8 billion in internal CAPEX to build proprietary API sites, Lilly simultaneously secured a $10 billion long-term "take-or-pay" CDMO lock-in. This agile capital allocation ensures strict internal quality control while retaining elastic external capacity to absorb demand shocks, granting Lilly superior supply chain resiliency without the drag of heavy-asset integration friction.

Strategic Pivots and Pipeline Moats

As the U.S. Inflation Reduction Act (IRA) looms, shortening the runway for premium pricing, both companies are rapidly fortifying their R&D pipelines to combat impending patent cliffs.

Lilly’s pipeline strategy revolves around generational leaps and cross-cycle risk hedging. Within metabolics, the company is advancing the triple-agonist Retatrutide and the oral small-molecule Orforglipron—a critical asset that circumvents the complex peptide cold-chain entirely, promising low marginal costs for global primary care penetration. Furthermore, Lilly leverages robust cash flows from its oncology and immunology portfolios, and its approved Alzheimer’s drug (Kisunla), creating a diversified moat insulated from metabolic pricing constraints.

Novo Nordisk’s strategy is rooted in deep vertical expansion into metabolic complications, securing approvals for cardiovascular (CVD) and MASH indications to maximize Semaglutide’s lifetime value. However, this creates intense concentration risk. The recent termination of its Alzheimer’s program and the underwhelming performance of its next-generation CagriSema—which failed to meet non-inferiority against Tirzepatide in head-to-head weight-loss trials (23% vs 25.5%)—leaves Novo highly dependent on a single-molecule foundation.

Cyclical Headwinds and Earnings Quality

Policy ceilings are transitioning from theoretical risks to tangible financial erosion. As IRA price negotiations bite, HDIN Research notes significant divergences in how both entities manage their balance sheets.

Novo Nordisk exhibits signs of earnings management through a reported $4.2 billion 340B pricing provision. The anticipated reversal of this provision in Q1 2026 acts as an accounting buffer, potentially smoothing over projected core business contractions (-5% to -13%). Meanwhile, Lilly's explosive growth warrants distinct audit scrutiny; a 61% surge in accounts receivable and a massive spike in inventory outpaced revenue growth, signaling potential channel-stuffing risks that could pressure 2026 cash conversion cycles if market penetration slows.

HDIN Viewpoint

HDIN Research views Eli Lilly as a "comprehensive outperformer." By leveraging its diversified innovation matrix, Lilly generates high-barrier cash flows to fund aggressive, multi-target GLP-1 dominance. Its agile supply chain and intergenerational pipeline leaps afford it superior downside protection against cyclical regulatory pricing shocks.

In contrast, Novo Nordisk acts as a "vertical integration specialist." While its deep entrenchment in cardiovascular and renal adjacencies provides a solid defensive base, the company's heavy reliance on costly manufacturing acquisitions, accounting buffers, and a single-molecule architecture suggests a protracted and capital-intensive transitional phase. For institutional investors, the 2025 data indicates that Lilly is engineered for premium market capture, whereas Novo is currently priced for cyclical defense.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com