CRH vs. Amrize: Decoding the Divergent Strategic Moats in the 2025 Building Materials Sector

Date : 2026-02-26

Reading : 108

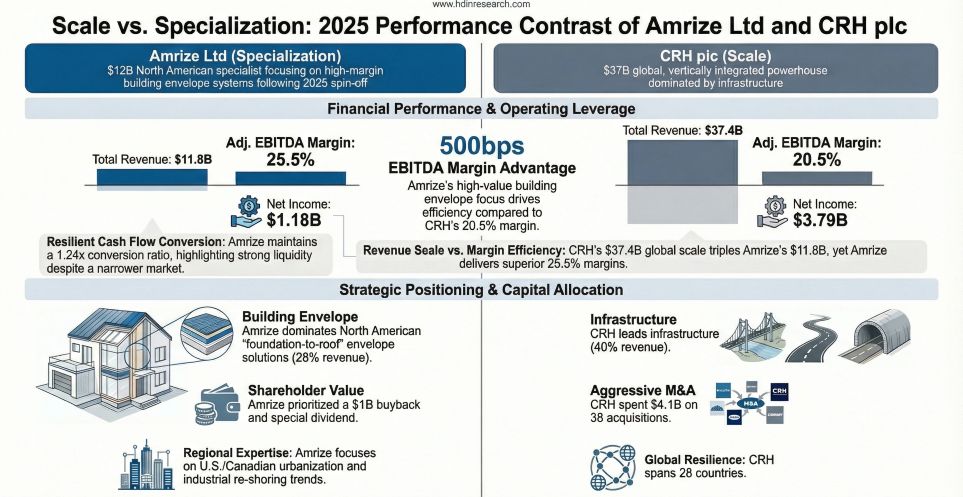

In the fiscal year 2025, the global building materials landscape witnessed a profound strategic bifurcation. While CRH plc consolidated its dominance as a $37.45 billion vertically integrated global juggernaut driven by macro-infrastructure tailwinds, Amrize Ltd—recently spun off from Holcim—emerged as an $11.82 billion highly specialized North American pure-play. HDIN Research’s in-depth fundamental analysis reveals that the competition is no longer simply about capacity expansion; it is a complex battle between global scale advantages and high-margin, niche technological applications.

Figure Scale vs Specialization 2025 Performance Contrast of Amrize Ltd and CRH plc

Sector Positioning: The Global Integrator vs. The North American Specialist

Sector Positioning: The Global Integrator vs. The North American Specialist

The structural divergence between the two firms is primarily rooted in their geographic and end-market reliance. CRH’s sector positioning operates on a "Connected Portfolio" model, where 40% of its revenue is deeply anchored to infrastructure projects. Benefiting significantly from the U.S. Infrastructure Investment and Jobs Act (IIJA), CRH utilizes its footprint across 28 countries to mitigate regional macroeconomic shocks. This infrastructure exposure acts as a robust counter-cyclical buffer during private residential downturns.

Conversely, Amrize maintains a hyper-concentrated geographic footprint, deriving over 99% of its revenue from the United States and Canada. Rather than competing head-on in sheer aggregate volume, Amrize has built robust strategic moats around its Building Envelope segment, which accounts for 28% of its top line. By focusing on advanced roofing systems, insulation, and waterproofing, Amrize heavily targets the Repair and Remodel (R&R) market (43% of total revenue). This focus on "mission-critical" maintenance allows Amrize to generate resilient cash flows that are structurally less sensitive to the cyclical headwinds of new housing starts.

Capital Allocation Efficiency: Aggressive Consolidation vs. Defensive Yield

The "so what" behind the financials lies in how each company maneuvers its capital in a high-interest-rate environment.

CRH exhibits an aggressive, growth-oriented capital allocation strategy. In 2025 alone, the company executed 38 acquisitions totaling $4.1 billion—most notably the $2.1 billion acquisition of Eco Material to secure low-carbon technological leadership. While this aggressive M&A strategy expanded its top line by 5%, it also pushed total debt to $17.65 billion.

Amrize, however, prioritizes capital allocation efficiency and shareholder returns over aggressive scale. Operating with an asset-light model compared to CRH, Amrize boasts a superior Adjusted EBITDA margin of 25.5% (versus CRH’s 20.5%) and an exceptional cash conversion ratio (OCF/Net Income) of 1.87. As a newly independent entity, Amrize has deployed a defensive yield strategy, approving a $1 billion share buyback program alongside special dividends, signaling a disciplined approach to cash flow generation rather than debt-fueled expansion.

Cyclical Headwinds and Accounting Vigilance

Both industry leaders face severe cyclical headwinds, notably the escalating costs of decarbonization and energy price volatility. However, HDIN Research advises institutional investors to look beyond the income statement and scrutinize balance sheet vulnerabilities:

* CRH’s Goodwill and Estimation Risks: CRH carries a massive $13.1 billion in goodwill (22.5% of total assets) accumulated from its relentless M&A streak. Furthermore, heavy reliance on the Percentage of Completion (POC) accounting method for its $8.69 billion services revenue introduces significant estimation elasticity. Any cost overruns in raw materials could force future margin restatements or impairment charges.

* Amrize’s Operational Transition: The primary headwind for Amrize is administrative rather than commercial. The company has acknowledged a "Material Weakness" in its internal controls over financial reporting, stemming from a lack of U.S. GAAP-experienced personnel following its separation from Holcim. Coupled with $80 million in spin-off and rebranding costs, this introduces short-term compliance and reporting friction.

HDIN Viewpoint

From the analytical desk of HDIN Research, the investment thesis for these two giants hinges on macroeconomic conviction. CRH is the definitive vehicle for investors seeking to capture global infrastructure stimulus and vertical integration synergies, albeit with rising leverage risks. Amrize, on the other hand, presents a compelling margin-expansion narrative for those who believe in the resilience of the North American re-industrialization and the high-premium Building Envelope lifecycle. The ultimate winner in the next half-decade will be the firm that best translates its decarbonization mandates into pricing power, seamlessly passing cyclical cost inflations onto the end-user.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure Scale vs Specialization 2025 Performance Contrast of Amrize Ltd and CRH plc

Sector Positioning: The Global Integrator vs. The North American SpecialistThe structural divergence between the two firms is primarily rooted in their geographic and end-market reliance. CRH’s sector positioning operates on a "Connected Portfolio" model, where 40% of its revenue is deeply anchored to infrastructure projects. Benefiting significantly from the U.S. Infrastructure Investment and Jobs Act (IIJA), CRH utilizes its footprint across 28 countries to mitigate regional macroeconomic shocks. This infrastructure exposure acts as a robust counter-cyclical buffer during private residential downturns.

Conversely, Amrize maintains a hyper-concentrated geographic footprint, deriving over 99% of its revenue from the United States and Canada. Rather than competing head-on in sheer aggregate volume, Amrize has built robust strategic moats around its Building Envelope segment, which accounts for 28% of its top line. By focusing on advanced roofing systems, insulation, and waterproofing, Amrize heavily targets the Repair and Remodel (R&R) market (43% of total revenue). This focus on "mission-critical" maintenance allows Amrize to generate resilient cash flows that are structurally less sensitive to the cyclical headwinds of new housing starts.

Capital Allocation Efficiency: Aggressive Consolidation vs. Defensive Yield

The "so what" behind the financials lies in how each company maneuvers its capital in a high-interest-rate environment.

CRH exhibits an aggressive, growth-oriented capital allocation strategy. In 2025 alone, the company executed 38 acquisitions totaling $4.1 billion—most notably the $2.1 billion acquisition of Eco Material to secure low-carbon technological leadership. While this aggressive M&A strategy expanded its top line by 5%, it also pushed total debt to $17.65 billion.

Amrize, however, prioritizes capital allocation efficiency and shareholder returns over aggressive scale. Operating with an asset-light model compared to CRH, Amrize boasts a superior Adjusted EBITDA margin of 25.5% (versus CRH’s 20.5%) and an exceptional cash conversion ratio (OCF/Net Income) of 1.87. As a newly independent entity, Amrize has deployed a defensive yield strategy, approving a $1 billion share buyback program alongside special dividends, signaling a disciplined approach to cash flow generation rather than debt-fueled expansion.

Cyclical Headwinds and Accounting Vigilance

Both industry leaders face severe cyclical headwinds, notably the escalating costs of decarbonization and energy price volatility. However, HDIN Research advises institutional investors to look beyond the income statement and scrutinize balance sheet vulnerabilities:

* CRH’s Goodwill and Estimation Risks: CRH carries a massive $13.1 billion in goodwill (22.5% of total assets) accumulated from its relentless M&A streak. Furthermore, heavy reliance on the Percentage of Completion (POC) accounting method for its $8.69 billion services revenue introduces significant estimation elasticity. Any cost overruns in raw materials could force future margin restatements or impairment charges.

* Amrize’s Operational Transition: The primary headwind for Amrize is administrative rather than commercial. The company has acknowledged a "Material Weakness" in its internal controls over financial reporting, stemming from a lack of U.S. GAAP-experienced personnel following its separation from Holcim. Coupled with $80 million in spin-off and rebranding costs, this introduces short-term compliance and reporting friction.

HDIN Viewpoint

From the analytical desk of HDIN Research, the investment thesis for these two giants hinges on macroeconomic conviction. CRH is the definitive vehicle for investors seeking to capture global infrastructure stimulus and vertical integration synergies, albeit with rising leverage risks. Amrize, on the other hand, presents a compelling margin-expansion narrative for those who believe in the resilience of the North American re-industrialization and the high-premium Building Envelope lifecycle. The ultimate winner in the next half-decade will be the firm that best translates its decarbonization mandates into pricing power, seamlessly passing cyclical cost inflations onto the end-user.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com