Zebra Technologies vs. Diebold Nixdorf: Navigating AI Transitions and Geopolitical Headwinds

Date : 2026-02-26

Reading : 113

As the automation and frontline technology sectors shift from legacy hardware provision to AI-driven, end-to-end solution architectures, Zebra Technologies (ZBRA) and Diebold Nixdorf (DBD) present a stark contrast in risk and reward. Based on our comprehensive FY2025 audit, Zebra’s aggressive M&A strategy has fueled robust technological expansion but birthed a "gray rhino" of goodwill risk. Conversely, Diebold Nixdorf’s post-restructuring financial health appears stabilized on paper, yet its reliance on "Fresh Start Accounting" obscures a critical lack of endogenous growth. For institutional investors, the 2025 landscape dictates a rigorous evaluation of how these firms balance capital allocation efficiency against intensifying cyclical headwinds.

Figure 2025 Strategic Outlook: Zebra vs Diebold Nixdorf

Sector Positioning & Strategic Moats

Sector Positioning & Strategic Moats

Both legacy hardware giants are executing a synchronized strategic pivot: "hardware softening, computing forward." By utilizing high-switching-cost physical hardware as an anchoring point, both firms are aggressively expanding their software and service ecosystems to generate sticky, recurring revenue.

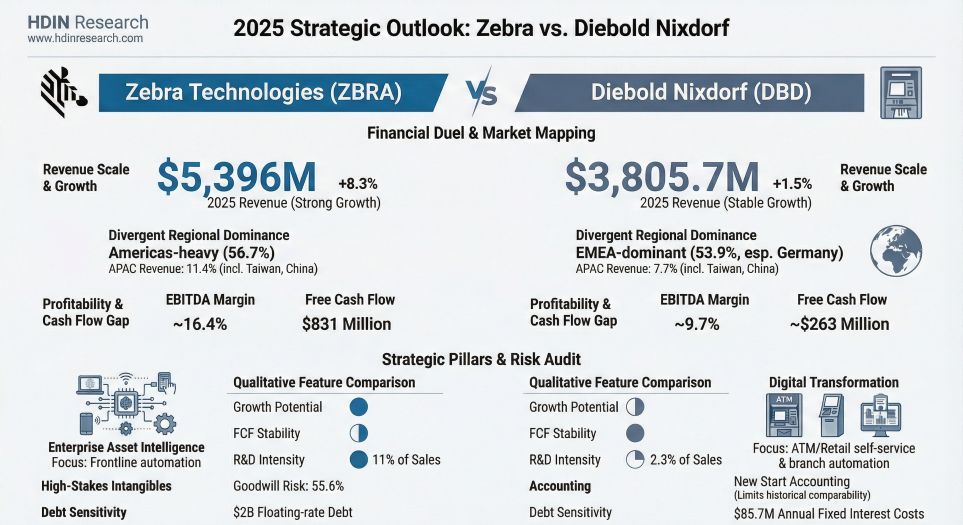

* Zebra’s Expansive TAM: Zebra is riding a pro-cyclical wave of digital transformation across logistics, retail, and manufacturing. Its strategic moat is fortified by its Connected Frontline (CF) division and heavy investments in 3D machine vision (via the Photoneo integration). By processing complex visual data at the edge, Zebra is successfully monetizing AI capabilities. However, its overarching reliance on tangible product sales (81.9% of revenue) leaves its cash flows highly sensitive to macroeconomic consumption cycles.

* Diebold Nixdorf’s Defensive Bastion: Operating in a counter-cyclical environment driven by labor cost reduction, Diebold Nixdorf retains a formidable defensive moat in the banking sector. Locking in nearly two-thirds of the world's top 100 financial institutions, the company generates 57% of its revenue from high-margin, long-term service contracts. Its strategic pivot centers on the Vynamic software suite and AI vision technology to mitigate retail shrink, effectively hedging against the secular decline of physical cash usage.

Capital Allocation Efficiency & Financial Health

Beneath the surface of top-line revenue, stark divergences in capital allocation efficiency reveal distinct vulnerability profiles.

* Zebra’s Earnings Management & Goodwill Exposure: While Zebra boasts superior gross margins (48.1%) and formidable free cash flow, its capital allocation raises red flags. In FY2025, the company executed a massive $587 million stock buyback, eclipsing its net income of $419 million. Executing maximum buybacks amidst a 20.6% year-over-year net income decline suggests a distinct earnings management strategy designed to artificially inflate diluted EPS. Furthermore, its $1.3 billion acquisition of Elo has bloated goodwill to $4.7 billion—a staggering 55.6% of total assets. Any integration friction could trigger catastrophic impairment charges.

* Diebold’s Accounting Illusion & Innovation Deficit: Diebold Nixdorf’s post-bankruptcy balance sheet looks cleaner, and its superior inventory turnover (5.42x vs. Zebra’s 3.94x) demonstrates excellent supply chain elasticity. However, the application of "Fresh Start Accounting" resets asset values and depresses depreciation, legally artificially inflating profitability and destroying historical comparability. Fundamentally, Diebold is starving its future: R&D spend sits at a meager 2.3% of revenue ($86.7M), relying on pricing strategies rather than product innovation to drive its sluggish 1.5% YoY revenue growth. Furthermore, a heavy $85.7 million annual interest burden continues to siphon critical reinvestment capital.

Cyclical Headwinds & Supply Chain Vulnerabilities

Global geopolitical fragmentation serves as the ultimate macro ceiling for both enterprises, exposing profound supply chain vulnerabilities rooted in the Asia-Pacific region.

* Manufacturing Concentration: Both firms are critically dependent on APAC—specifically China, Taiwan, Malaysia, and Vietnam—for hardware assembly. Zebra has explicitly warned that regional tensions or disruptions in Taiwan could lead to severe operational paralysis due to a lack of alternative capacity.

* Tariffs vs. Sanctions: Zebra’s profit margins are directly squeezed by US-China tariff walls, forcing costly supply chain realignments that elevated FY2025 operational expenses. Diebold Nixdorf, however, faces existential compliance risks. Its heavy reliance on Chinese joint ventures (e.g., Inspur and Aisino) places it directly in the crosshairs of US Export Administration Regulations (EAR). If its joint venture partners are added to the US Entity List, Diebold faces the immediate severing of its software and technology supply lines in the region.

HDIN Viewpoint

From an institutional advisory perspective, HDIN Research views Zebra Technologies as a high-ceiling growth play burdened by immense balance sheet fragility. Its technological leadership in AI edge computing is undeniable, but investors must heavily discount its valuation to account for extreme channel concentration (top three distributors control 59% of revenue) and the looming threat of goodwill impairment.

Diebold Nixdorf, conversely, operates as a mature cash-cow proxy. Its restructuring has flushed out immediate insolvency risks, and its European banking stronghold provides robust cash flow visibility. Yet, without a structural acceleration in R&D, Diebold risks long-term obsolescence as the global economy accelerates toward cashless infrastructures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Strategic Outlook: Zebra vs Diebold Nixdorf

Sector Positioning & Strategic MoatsBoth legacy hardware giants are executing a synchronized strategic pivot: "hardware softening, computing forward." By utilizing high-switching-cost physical hardware as an anchoring point, both firms are aggressively expanding their software and service ecosystems to generate sticky, recurring revenue.

* Zebra’s Expansive TAM: Zebra is riding a pro-cyclical wave of digital transformation across logistics, retail, and manufacturing. Its strategic moat is fortified by its Connected Frontline (CF) division and heavy investments in 3D machine vision (via the Photoneo integration). By processing complex visual data at the edge, Zebra is successfully monetizing AI capabilities. However, its overarching reliance on tangible product sales (81.9% of revenue) leaves its cash flows highly sensitive to macroeconomic consumption cycles.

* Diebold Nixdorf’s Defensive Bastion: Operating in a counter-cyclical environment driven by labor cost reduction, Diebold Nixdorf retains a formidable defensive moat in the banking sector. Locking in nearly two-thirds of the world's top 100 financial institutions, the company generates 57% of its revenue from high-margin, long-term service contracts. Its strategic pivot centers on the Vynamic software suite and AI vision technology to mitigate retail shrink, effectively hedging against the secular decline of physical cash usage.

Capital Allocation Efficiency & Financial Health

Beneath the surface of top-line revenue, stark divergences in capital allocation efficiency reveal distinct vulnerability profiles.

* Zebra’s Earnings Management & Goodwill Exposure: While Zebra boasts superior gross margins (48.1%) and formidable free cash flow, its capital allocation raises red flags. In FY2025, the company executed a massive $587 million stock buyback, eclipsing its net income of $419 million. Executing maximum buybacks amidst a 20.6% year-over-year net income decline suggests a distinct earnings management strategy designed to artificially inflate diluted EPS. Furthermore, its $1.3 billion acquisition of Elo has bloated goodwill to $4.7 billion—a staggering 55.6% of total assets. Any integration friction could trigger catastrophic impairment charges.

* Diebold’s Accounting Illusion & Innovation Deficit: Diebold Nixdorf’s post-bankruptcy balance sheet looks cleaner, and its superior inventory turnover (5.42x vs. Zebra’s 3.94x) demonstrates excellent supply chain elasticity. However, the application of "Fresh Start Accounting" resets asset values and depresses depreciation, legally artificially inflating profitability and destroying historical comparability. Fundamentally, Diebold is starving its future: R&D spend sits at a meager 2.3% of revenue ($86.7M), relying on pricing strategies rather than product innovation to drive its sluggish 1.5% YoY revenue growth. Furthermore, a heavy $85.7 million annual interest burden continues to siphon critical reinvestment capital.

Cyclical Headwinds & Supply Chain Vulnerabilities

Global geopolitical fragmentation serves as the ultimate macro ceiling for both enterprises, exposing profound supply chain vulnerabilities rooted in the Asia-Pacific region.

* Manufacturing Concentration: Both firms are critically dependent on APAC—specifically China, Taiwan, Malaysia, and Vietnam—for hardware assembly. Zebra has explicitly warned that regional tensions or disruptions in Taiwan could lead to severe operational paralysis due to a lack of alternative capacity.

* Tariffs vs. Sanctions: Zebra’s profit margins are directly squeezed by US-China tariff walls, forcing costly supply chain realignments that elevated FY2025 operational expenses. Diebold Nixdorf, however, faces existential compliance risks. Its heavy reliance on Chinese joint ventures (e.g., Inspur and Aisino) places it directly in the crosshairs of US Export Administration Regulations (EAR). If its joint venture partners are added to the US Entity List, Diebold faces the immediate severing of its software and technology supply lines in the region.

HDIN Viewpoint

From an institutional advisory perspective, HDIN Research views Zebra Technologies as a high-ceiling growth play burdened by immense balance sheet fragility. Its technological leadership in AI edge computing is undeniable, but investors must heavily discount its valuation to account for extreme channel concentration (top three distributors control 59% of revenue) and the looming threat of goodwill impairment.

Diebold Nixdorf, conversely, operates as a mature cash-cow proxy. Its restructuring has flushed out immediate insolvency risks, and its European banking stronghold provides robust cash flow visibility. Yet, without a structural acceleration in R&D, Diebold risks long-term obsolescence as the global economy accelerates toward cashless infrastructures.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com