2025 Global Diabetes Management Giants: Sector Positioning and Strategic Moats

Date : 2026-02-26

Reading : 584

The global diabetes management sector reached a critical inflection point in 2025. Moving beyond traditional hardware-centric sales, the industry's vanguard is aggressively transitioning toward high-margin, algorithm-driven subscription models. An in-depth financial analysis of the top five industry leaders—Abbott, Dexcom, Insulet, Tandem, and Embecta—reveals a stark bifurcation in sector positioning. While the rise of GLP-1 therapies acts as a structural headwind for traditional injection segments, it has simultaneously catalyzed a massive Total Addressable Market (TAM) expansion for continuous glucose monitoring (CGM) players, redefining the competitive moats of the next decade.

Figure 2025 Global Diabetes Management: The High-Tech Duel and Financial Frontier

Financial Health & Capital Allocation Efficiency

Financial Health & Capital Allocation Efficiency

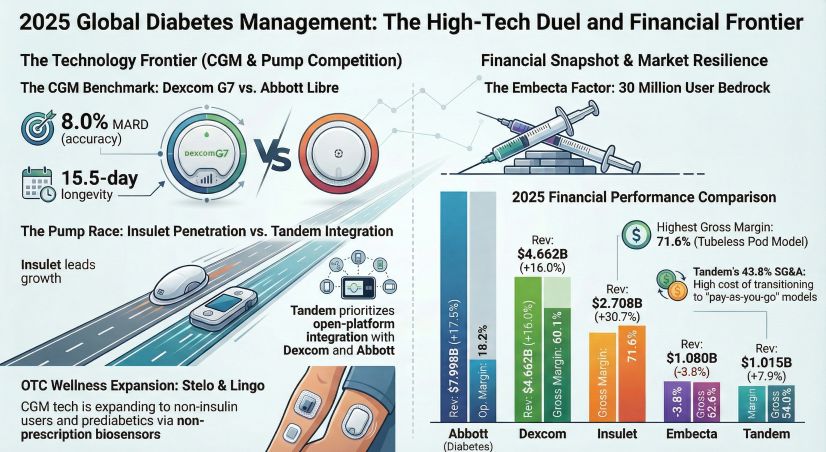

A granular look at the 2025 financial disclosures illustrates how scale and capital allocation dictate operational resilience.

* Scale and Ecosystem Monetization: Abbott and Dexcom demonstrate mature capital efficiency by leveraging immense economies of scale. Abbott’s diabetes care unit achieved a commanding $7.99 billion in revenue (a 17.5% YoY surge), driven heavily by its FreeStyle Libre franchise. Dexcom, posting $4.66 billion in revenue with an exceptional 60.1% gross margin, exhibited profound operational stability. Dexcom’s aggressive $500 million share buyback program signals strong management confidence in organic cash flow generation, further fortified by the launch of its over-the-counter (OTC) Stelo sensor.

* High-Growth Alpha vs. Transition Pains: In the Automated Insulin Delivery (AID) space, capital allocation strategies diverged sharply. Insulet delivered a striking 30.7% revenue growth and an industry-leading 71.6% gross margin. Instead of optimizing for short-term net income, Insulet utilized its margin premium to fuel a 43.0% SG&A rate, aggressively acquiring international market share and pushing into the Type 2 Diabetes (T2D) segment. Conversely, Tandem faced cyclical headwinds, posting a modest 7.9% growth. Tandem’s current profitability is temporarily suppressed as it absorbs the financial shock of transitioning from upfront hardware revenue to a deferred, consumable-driven model.

* Structural Retreat: Embecta, burdened by a 3.8% revenue contraction, represents the defensive posture of legacy hardware. Facing declining daily injection frequencies, the company wisely optimized its capital allocation by terminating its patch pump R&D, absorbing a $34.5 million restructuring charge to fiercely protect its core free cash flow.

Strategic Pivots: The Pharmacy Channel & Subscription Economics

The most profound structural shift in 2025 is the aggressive migration from the traditional Durable Medical Equipment (DME) distribution framework to the Pharmacy Channel.

This is not merely a logistical shift; it is a fundamental redesign of the unit economic model. By eliminating exorbitant upfront pump costs, companies like Insulet and Tandem are radically lowering the barrier to entry for new patients. While this "pay-as-you-go" strategy creates short-term margin friction (notably for Tandem), the long-term strategic implication is a highly resilient subscription moat. By monetizing proprietary software (like Tandem's Control-IQ+ and Insulet's SmartAdjust) through high-frequency consumable purchases, these firms are significantly expanding the Lifetime Value (LTV) of their user base.

Sector Positioning: Navigating the GLP-1 Ecosystem & Geopolitical Headwinds

The proliferation of GLP-1 therapies has forced management teams to re-evaluate their long-term sector positioning.

* The GLP-1 Catalyst: Rather than a threat, CGM leaders view GLP-1s as a powerful market multiplier. Dexcom and Abbott have strategically positioned their sensors (Stelo and Lingo, respectively) as essential "companion products" to monitor metabolic health, effectively expanding their TAM from strictly insulin-dependent patients to a broader demographic of 25 million non-insulin T2D and pre-diabetic individuals.

* The GLP-1 Headwind: Pump manufacturers Insulet and Tandem acknowledge that GLP-1s may delay patient progression to intensive insulin therapy, prompting them to accelerate their push into the T2D AID market to offset delayed onboarding. For Embecta, GLP-1s present a severe, structural threat to its core Multiple Daily Injection (MDI) base.

* Geopolitical and Policy Constraints: The regulatory landscape continues to exert margin pressure. Both Abbott and Embecta cited severe price erosion resulting from Volume-Based Procurement (VBP) policies in China, validating that localized manufacturing alone cannot fully insulate against centralized pricing power.

HDIN Viewpoint

At HDIN Research, we assess the 2025 Diabetes Management sector's vitality index at a robust 8.5/10, yet we advise cautious optimism regarding profit structure reorganization. The ultimate strategic moat has evolved: clinical accuracy is now merely table stakes, replaced by "interoperability and algorithm monetization" as the true drivers of enterprise value.

Investors and stakeholders must remain hyper-vigilant regarding two impending inflection points. First, the scheduled 2028 Medicare DMEPOS competitive bidding process will likely establish a rigid structural price ceiling for hardware. Second, the success of the current pharmacy channel transition hinges entirely on whether the high-margin consumable ecosystem can successfully offset the evaporation of upfront capital sales. Companies that fail to lock users into a closed-loop algorithmic ecosystem will inevitably face commoditization.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Diabetes Management: The High-Tech Duel and Financial Frontier

Financial Health & Capital Allocation EfficiencyA granular look at the 2025 financial disclosures illustrates how scale and capital allocation dictate operational resilience.

* Scale and Ecosystem Monetization: Abbott and Dexcom demonstrate mature capital efficiency by leveraging immense economies of scale. Abbott’s diabetes care unit achieved a commanding $7.99 billion in revenue (a 17.5% YoY surge), driven heavily by its FreeStyle Libre franchise. Dexcom, posting $4.66 billion in revenue with an exceptional 60.1% gross margin, exhibited profound operational stability. Dexcom’s aggressive $500 million share buyback program signals strong management confidence in organic cash flow generation, further fortified by the launch of its over-the-counter (OTC) Stelo sensor.

* High-Growth Alpha vs. Transition Pains: In the Automated Insulin Delivery (AID) space, capital allocation strategies diverged sharply. Insulet delivered a striking 30.7% revenue growth and an industry-leading 71.6% gross margin. Instead of optimizing for short-term net income, Insulet utilized its margin premium to fuel a 43.0% SG&A rate, aggressively acquiring international market share and pushing into the Type 2 Diabetes (T2D) segment. Conversely, Tandem faced cyclical headwinds, posting a modest 7.9% growth. Tandem’s current profitability is temporarily suppressed as it absorbs the financial shock of transitioning from upfront hardware revenue to a deferred, consumable-driven model.

* Structural Retreat: Embecta, burdened by a 3.8% revenue contraction, represents the defensive posture of legacy hardware. Facing declining daily injection frequencies, the company wisely optimized its capital allocation by terminating its patch pump R&D, absorbing a $34.5 million restructuring charge to fiercely protect its core free cash flow.

Strategic Pivots: The Pharmacy Channel & Subscription Economics

The most profound structural shift in 2025 is the aggressive migration from the traditional Durable Medical Equipment (DME) distribution framework to the Pharmacy Channel.

This is not merely a logistical shift; it is a fundamental redesign of the unit economic model. By eliminating exorbitant upfront pump costs, companies like Insulet and Tandem are radically lowering the barrier to entry for new patients. While this "pay-as-you-go" strategy creates short-term margin friction (notably for Tandem), the long-term strategic implication is a highly resilient subscription moat. By monetizing proprietary software (like Tandem's Control-IQ+ and Insulet's SmartAdjust) through high-frequency consumable purchases, these firms are significantly expanding the Lifetime Value (LTV) of their user base.

Sector Positioning: Navigating the GLP-1 Ecosystem & Geopolitical Headwinds

The proliferation of GLP-1 therapies has forced management teams to re-evaluate their long-term sector positioning.

* The GLP-1 Catalyst: Rather than a threat, CGM leaders view GLP-1s as a powerful market multiplier. Dexcom and Abbott have strategically positioned their sensors (Stelo and Lingo, respectively) as essential "companion products" to monitor metabolic health, effectively expanding their TAM from strictly insulin-dependent patients to a broader demographic of 25 million non-insulin T2D and pre-diabetic individuals.

* The GLP-1 Headwind: Pump manufacturers Insulet and Tandem acknowledge that GLP-1s may delay patient progression to intensive insulin therapy, prompting them to accelerate their push into the T2D AID market to offset delayed onboarding. For Embecta, GLP-1s present a severe, structural threat to its core Multiple Daily Injection (MDI) base.

* Geopolitical and Policy Constraints: The regulatory landscape continues to exert margin pressure. Both Abbott and Embecta cited severe price erosion resulting from Volume-Based Procurement (VBP) policies in China, validating that localized manufacturing alone cannot fully insulate against centralized pricing power.

HDIN Viewpoint

At HDIN Research, we assess the 2025 Diabetes Management sector's vitality index at a robust 8.5/10, yet we advise cautious optimism regarding profit structure reorganization. The ultimate strategic moat has evolved: clinical accuracy is now merely table stakes, replaced by "interoperability and algorithm monetization" as the true drivers of enterprise value.

Investors and stakeholders must remain hyper-vigilant regarding two impending inflection points. First, the scheduled 2028 Medicare DMEPOS competitive bidding process will likely establish a rigid structural price ceiling for hardware. Second, the success of the current pharmacy channel transition hinges entirely on whether the high-margin consumable ecosystem can successfully offset the evaporation of upfront capital sales. Companies that fail to lock users into a closed-loop algorithmic ecosystem will inevitably face commoditization.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

About HDIN Research Profile: HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com