Nachi-Fujikoshi FY2025

Date : 2026-02-27

Reading : 291

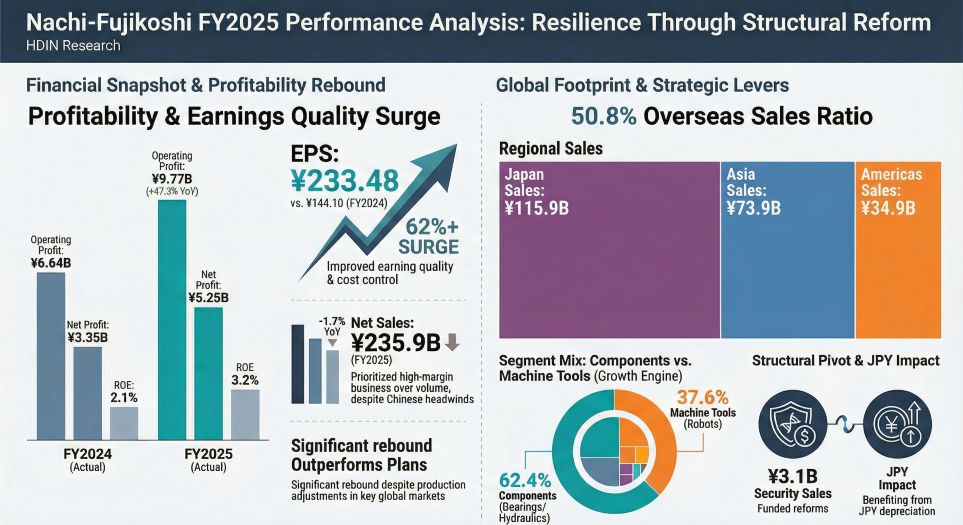

Nachi-Fujikoshi’s (Nachi) FY2025 report reveals a company in the midst of a critical "structural transition." While consolidated revenue dipped slightly by 1.7% to $1.577 billion, operating profit surged by a remarkable 47.3%. At HDIN Research, we interpret this divergence not merely as a fluctuation, but as the result of an "aggressive defense" strategy: prioritizing profit repair over scale expansion while accelerating a high-stakes pivot from traditional automotive components to a Robot-Centric business model.

Financial Health: The Anatomy of Profit Repair

The headline growth in operating profit (reaching a 4.1% margin) was driven less by market demand and more by internal rigor. Nachi effectively utilized a weak yen (averaging 149.57 JPY/USD) and aggressive price pass-throughs to counter raw material inflation.

However, the "So What" behind these numbers lies in the Structural Reform. The company recorded approximately $20.85 million in special losses dedicated to personnel and equipment optimization. This "subtraction strategy" aims to lower the break-even point, ensuring free cash flow (FCF) generation even in a low-growth environment. By shedding the weight of low-margin assets, Nachi is attempting to buy time for its growth engines to ignite.

Strategic Pivot: Vertical Integration in the EV Era

Nachi’s unique value proposition—its status as a comprehensive machinery manufacturer integrating materials, tools, and robots—is facing a stress test. The automotive sector, accounting for roughly 50% of revenue, is undergoing a rapid shift to Electric Vehicles (EVs).

* From Burden to Moat: In the internal combustion engine (ICE) era, vertical integration often dragged down capital efficiency. In the EV era, it is becoming a competitive moat. Nachi is leveraging its proprietary special steel technology to produce EV-insulated bearings and flexible manufacturing systems for e-Axles.

* The Robot Offensive: To escape the cyclicality of the auto sector, Nachi is positioning robotics as its central growth pillar. The launch of the MZS05, the world’s first collision-detecting collaborative robot that does not sacrifice speed, signals a move to challenge competitors like Fanuc and Yaskawa in non-automotive sectors.

Regional Dynamics: decoupling Growth Engines

The report highlights a significant divergence in regional momentum essential for Nachi’s 2030 vision of a 60% overseas sales ratio.

* China Headwinds: The robotics division faced a 5.3% revenue decline due to delayed capital expenditures in China. This signals a need to reduce over-reliance on the Chinese industrial cycle.

* The US & India Nexus: Conversely, the strategy now hinges on the resilience of the North American tool market and the expanding industrial base in India. The company is aggressively localizing production in these regions to decouple its growth trajectory from East Asian volatility.

Capital Allocation: Efficiency vs. Engineering

A closer look at the balance sheet reveals a complex picture of capital efficiency. With an ROE of just 3.2% and an asset turnover of 0.71, Nachi remains a heavy-asset operation.

Crucially, HDIN Research analysts note that the company offset its structural reform losses by selling approximately $20.91 million in policy-held investment securities. While this "profit smoothing" stabilizes the bottom line and maintains dividends (100 yen/share), it masks the underlying fragility of core operational profitability. True capital efficiency will only be achieved when the robotics division moves from the investment phase to the scale-profitability phase.

HDIN Viewpoint: The Race Against Time

The core narrative of Nachi-Fujikoshi’s FY2025 is one of race and replacement. The company is racing to replace the cash flow from declining legacy automotive parts with high-margin robotics and EV solutions.

While the "profit repair" via cost-cutting and asset sales has been successful in the short term, these are finite levers. The long-term valuation of Nachi depends entirely on two factors:

1. Technological Adoption: Can the AI-integrated MZS05 robot capture significant market share outside the auto industry?

2. EV Supply Chain Penetration: Can their proprietary materials science lock them into the next generation of EV drive systems?

Investors should look beyond the 47.3% profit jump and monitor the quarterly growth of the robotics division in the US and India. That is where the company’s future valuation resides.

Figure Nachi-Fujikoshi FY2025 Performance Analysis: Resilience Through Structural Reform

Presentation Download

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Financial Health: The Anatomy of Profit Repair

The headline growth in operating profit (reaching a 4.1% margin) was driven less by market demand and more by internal rigor. Nachi effectively utilized a weak yen (averaging 149.57 JPY/USD) and aggressive price pass-throughs to counter raw material inflation.

However, the "So What" behind these numbers lies in the Structural Reform. The company recorded approximately $20.85 million in special losses dedicated to personnel and equipment optimization. This "subtraction strategy" aims to lower the break-even point, ensuring free cash flow (FCF) generation even in a low-growth environment. By shedding the weight of low-margin assets, Nachi is attempting to buy time for its growth engines to ignite.

Strategic Pivot: Vertical Integration in the EV Era

Nachi’s unique value proposition—its status as a comprehensive machinery manufacturer integrating materials, tools, and robots—is facing a stress test. The automotive sector, accounting for roughly 50% of revenue, is undergoing a rapid shift to Electric Vehicles (EVs).

* From Burden to Moat: In the internal combustion engine (ICE) era, vertical integration often dragged down capital efficiency. In the EV era, it is becoming a competitive moat. Nachi is leveraging its proprietary special steel technology to produce EV-insulated bearings and flexible manufacturing systems for e-Axles.

* The Robot Offensive: To escape the cyclicality of the auto sector, Nachi is positioning robotics as its central growth pillar. The launch of the MZS05, the world’s first collision-detecting collaborative robot that does not sacrifice speed, signals a move to challenge competitors like Fanuc and Yaskawa in non-automotive sectors.

Regional Dynamics: decoupling Growth Engines

The report highlights a significant divergence in regional momentum essential for Nachi’s 2030 vision of a 60% overseas sales ratio.

* China Headwinds: The robotics division faced a 5.3% revenue decline due to delayed capital expenditures in China. This signals a need to reduce over-reliance on the Chinese industrial cycle.

* The US & India Nexus: Conversely, the strategy now hinges on the resilience of the North American tool market and the expanding industrial base in India. The company is aggressively localizing production in these regions to decouple its growth trajectory from East Asian volatility.

Capital Allocation: Efficiency vs. Engineering

A closer look at the balance sheet reveals a complex picture of capital efficiency. With an ROE of just 3.2% and an asset turnover of 0.71, Nachi remains a heavy-asset operation.

Crucially, HDIN Research analysts note that the company offset its structural reform losses by selling approximately $20.91 million in policy-held investment securities. While this "profit smoothing" stabilizes the bottom line and maintains dividends (100 yen/share), it masks the underlying fragility of core operational profitability. True capital efficiency will only be achieved when the robotics division moves from the investment phase to the scale-profitability phase.

HDIN Viewpoint: The Race Against Time

The core narrative of Nachi-Fujikoshi’s FY2025 is one of race and replacement. The company is racing to replace the cash flow from declining legacy automotive parts with high-margin robotics and EV solutions.

While the "profit repair" via cost-cutting and asset sales has been successful in the short term, these are finite levers. The long-term valuation of Nachi depends entirely on two factors:

1. Technological Adoption: Can the AI-integrated MZS05 robot capture significant market share outside the auto industry?

2. EV Supply Chain Penetration: Can their proprietary materials science lock them into the next generation of EV drive systems?

Investors should look beyond the 47.3% profit jump and monitor the quarterly growth of the robotics division in the US and India. That is where the company’s future valuation resides.

Figure Nachi-Fujikoshi FY2025 Performance Analysis: Resilience Through Structural Reform

Presentation DownloadClick the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com