2025 Global Ophthalmic Medical Devices: Navigating Strategic Moats and Capital Allocation Efficiency

Date : 2026-02-27

Reading : 369

The global ophthalmic medical device industry in 2025 has reached a critical strategic inflection point. Driven by an aging global population and a myopia epidemic, the sector's underlying growth remains robust. However, beneath the surface of top-line expansion, HDIN Research observes a severe bifurcation in corporate performance. The era of pure hardware-driven growth has concluded; the new battleground is defined by digital ecosystem stickiness, cross-sector synergies, and rigorous capital discipline. For global leaders—Alcon, Johnson & Johnson (J&J) Vision, Carl Zeiss Meditec (CZM), and Bausch + Lomb (B+L)—success is no longer just about market share, but about translating scale into sustainable, high-quality profitability.

Figure 2025 Global Ophthalmology Big Four: Strategic Comparison & Market Framework

Financial Health: The Divergence in Capital Allocation Efficiency

Financial Health: The Divergence in Capital Allocation Efficiency

A deep dive into 2025 financial disclosures reveals that profitability quality varies drastically across the sector, heavily influenced by corporate structure and capital allocation efficiency.

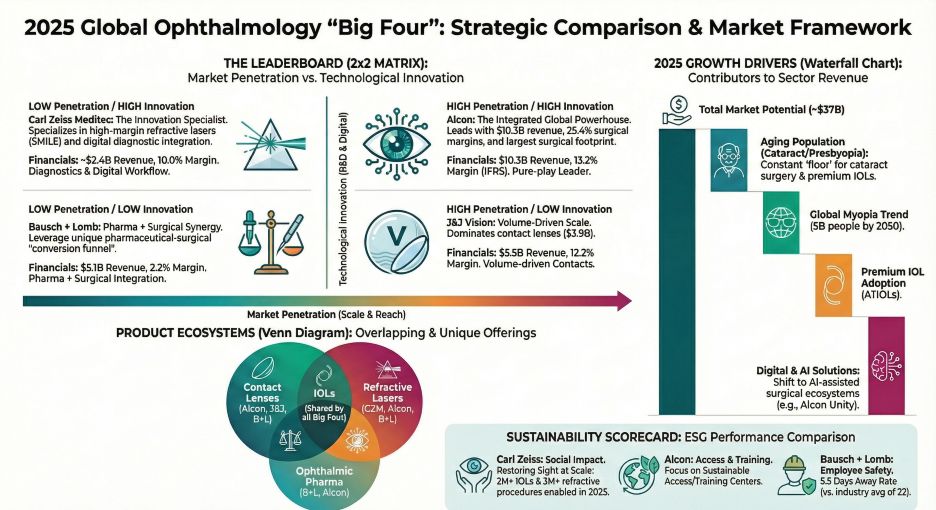

Alcon stands out as the industry’s undisputed "cash cow." By operating as an independent, pure-play ophthalmic entity, Alcon leverages a highly efficient "one-stop shop" model. This operational focus drove $10.3 billion in net sales and generated $1.7 billion in free cash flow (FCF), boasting a highly conservative accounting approach that expenses R&D immediately. This immense cash generation provides Alcon with a formidable reinvestment moat, funding $750 million in share buybacks and aggressive M&A activities without compromising its balance sheet.

Conversely, structural burdens severely dilute the profitability of other major players. While J&J Vision commands massive scale ($5.5 billion in sales), its parent company's broader MedTech restructuring and legacy legal liabilities systematically drag down its ultimate margin realization. Bausch + Lomb faces an even more precarious financial reality. Despite generating $5.1 billion in revenue, the company recorded a net loss of $360 million, constrained by an oppressive interest burden and the fallout from the enVista intraocular lens (IOL) recall. B+L's capital allocation remains defensively tethered to debt servicing rather than proactive market expansion.

Strategic Moats: Digital Ecosystems and Cross-Sector Synergies

To combat commoditization, industry leaders are aggressively constructing strategic moats through adjacent ecosystems, raising switching costs for healthcare providers.

Carl Zeiss Meditec (CZM) has masterfully executed a "Diagnostics + Surgical" synergy. By positioning its diagnostic equipment (like OCT) as the mandatory gateway for surgical workflow, CZM locks hospitals into its digital ecosystem. With over 68,000 software licenses issued, CZM ensures that diagnostic data seamlessly feeds into its VISUMAX 800 surgical systems. This digital stickiness secures the continuous pull-through of high-margin consumables, such as those used in SMILE procedures.

Similarly, Bausch + Lomb utilizes a "Pharmaceuticals + Surgical" funnel. By leveraging heavyweight dry eye therapeutics (XIIDRA and MIEBO), B+L captures the patient at the consumer level and channels them into professional surgical pipelines, effectively driving adoption of its Stellaris platforms and IOLs through integrated pre- and post-operative care protocols.

Sector Positioning Against Cyclical Headwinds

The macroeconomic turbulence of 2025—characterized by inflation, tariff pressures, and cautious consumer spending—tested the resilience of the ophthalmic sector. Companies with balanced portfolios successfully utilized consumer-driven segments to hedge against the cyclicality of elective procedures.

Elective surgeries, particularly those utilizing self-pay Advanced Technology IOLs (ATIOLs), proved highly vulnerable to cyclical headwinds. Both Alcon and CZM noted that tightened consumer sentiment delayed discretionary surgical investments. However, vision care divisions acted as a vital counter-cyclical anchor. Because contact lenses function as a daily necessity with high repeat-purchase rates, Alcon and J&J Vision utilized their robust vision care portfolios (like DAILIES TOTAL1 and ACUVUE) to generate steady, defensive cash flows, successfully offsetting the prolonged 7-to-10-year capital equipment procurement cycles.

Regional Strategy: Navigating China’s VBP and Localization

In emerging markets, particularly China (including the Taiwan region), sector positioning requires a radical strategic pivot. The expansion of Volume-Based Procurement (VBP) policies has systematically eroded the Average Selling Prices (ASP) of foundational surgical consumables.

To defend their margins, foreign giants are executing a two-pronged strategy: shifting sales mixes toward premium, out-of-pocket ATIOLs (such as Alcon’s PanOptix Pro), and aggressively localizing production. CZM is rapidly expanding its manufacturing footprint in Suzhou and Guangzhou to secure "domestic" status, bypassing entry barriers and leveraging economies of scale to dilute manufacturing costs. The strategic implication is clear: the days of relying solely on an "imported premium" are over. Future growth in the region hinges entirely on localization execution and maintaining a generational technological gap over domestic competitors.

Strategic Pivots: Biologics and Robotic Automation

Looking toward the next decade, capital is flowing into disruptive pipelines. While CZM is deepening its integration of robotic-assisted microsurgery to push beyond human physiological limits, Alcon is making bold bets on biological alternatives. Alcon's $520 million acquisition of Aurion Biotech—targeting a revolutionary corneal endothelial cell therapy—signals a paradigm shift where pure device companies are evolving into hybrid "device + biologic" powerhouses to cure conditions previously unaddressable by hardware alone.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses that the global ophthalmic sector is transitioning from an era of volume expansion to one of structural profitability and digital integration. Investors and corporate strategists must remain vigilant regarding the escalating goodwill risks on balance sheets driven by aggressive M&A, as well as the cash flow vulnerabilities of highly leveraged firms facing sustained macroeconomic tightening.

In this landscape, operational discipline is paramount. Alcon's unmatched capital allocation efficiency, rapid inventory turnover, and robust digital integration make it the sector's optimal risk-reward standard in the current valuation environment. Meanwhile, competitors must urgently resolve their structural inefficiencies or risk being permanently relegated to lower-margin tiers as global procurement policies tighten.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 Global Ophthalmology Big Four: Strategic Comparison & Market Framework

Financial Health: The Divergence in Capital Allocation EfficiencyA deep dive into 2025 financial disclosures reveals that profitability quality varies drastically across the sector, heavily influenced by corporate structure and capital allocation efficiency.

Alcon stands out as the industry’s undisputed "cash cow." By operating as an independent, pure-play ophthalmic entity, Alcon leverages a highly efficient "one-stop shop" model. This operational focus drove $10.3 billion in net sales and generated $1.7 billion in free cash flow (FCF), boasting a highly conservative accounting approach that expenses R&D immediately. This immense cash generation provides Alcon with a formidable reinvestment moat, funding $750 million in share buybacks and aggressive M&A activities without compromising its balance sheet.

Conversely, structural burdens severely dilute the profitability of other major players. While J&J Vision commands massive scale ($5.5 billion in sales), its parent company's broader MedTech restructuring and legacy legal liabilities systematically drag down its ultimate margin realization. Bausch + Lomb faces an even more precarious financial reality. Despite generating $5.1 billion in revenue, the company recorded a net loss of $360 million, constrained by an oppressive interest burden and the fallout from the enVista intraocular lens (IOL) recall. B+L's capital allocation remains defensively tethered to debt servicing rather than proactive market expansion.

Strategic Moats: Digital Ecosystems and Cross-Sector Synergies

To combat commoditization, industry leaders are aggressively constructing strategic moats through adjacent ecosystems, raising switching costs for healthcare providers.

Carl Zeiss Meditec (CZM) has masterfully executed a "Diagnostics + Surgical" synergy. By positioning its diagnostic equipment (like OCT) as the mandatory gateway for surgical workflow, CZM locks hospitals into its digital ecosystem. With over 68,000 software licenses issued, CZM ensures that diagnostic data seamlessly feeds into its VISUMAX 800 surgical systems. This digital stickiness secures the continuous pull-through of high-margin consumables, such as those used in SMILE procedures.

Similarly, Bausch + Lomb utilizes a "Pharmaceuticals + Surgical" funnel. By leveraging heavyweight dry eye therapeutics (XIIDRA and MIEBO), B+L captures the patient at the consumer level and channels them into professional surgical pipelines, effectively driving adoption of its Stellaris platforms and IOLs through integrated pre- and post-operative care protocols.

Sector Positioning Against Cyclical Headwinds

The macroeconomic turbulence of 2025—characterized by inflation, tariff pressures, and cautious consumer spending—tested the resilience of the ophthalmic sector. Companies with balanced portfolios successfully utilized consumer-driven segments to hedge against the cyclicality of elective procedures.

Elective surgeries, particularly those utilizing self-pay Advanced Technology IOLs (ATIOLs), proved highly vulnerable to cyclical headwinds. Both Alcon and CZM noted that tightened consumer sentiment delayed discretionary surgical investments. However, vision care divisions acted as a vital counter-cyclical anchor. Because contact lenses function as a daily necessity with high repeat-purchase rates, Alcon and J&J Vision utilized their robust vision care portfolios (like DAILIES TOTAL1 and ACUVUE) to generate steady, defensive cash flows, successfully offsetting the prolonged 7-to-10-year capital equipment procurement cycles.

Regional Strategy: Navigating China’s VBP and Localization

In emerging markets, particularly China (including the Taiwan region), sector positioning requires a radical strategic pivot. The expansion of Volume-Based Procurement (VBP) policies has systematically eroded the Average Selling Prices (ASP) of foundational surgical consumables.

To defend their margins, foreign giants are executing a two-pronged strategy: shifting sales mixes toward premium, out-of-pocket ATIOLs (such as Alcon’s PanOptix Pro), and aggressively localizing production. CZM is rapidly expanding its manufacturing footprint in Suzhou and Guangzhou to secure "domestic" status, bypassing entry barriers and leveraging economies of scale to dilute manufacturing costs. The strategic implication is clear: the days of relying solely on an "imported premium" are over. Future growth in the region hinges entirely on localization execution and maintaining a generational technological gap over domestic competitors.

Strategic Pivots: Biologics and Robotic Automation

Looking toward the next decade, capital is flowing into disruptive pipelines. While CZM is deepening its integration of robotic-assisted microsurgery to push beyond human physiological limits, Alcon is making bold bets on biological alternatives. Alcon's $520 million acquisition of Aurion Biotech—targeting a revolutionary corneal endothelial cell therapy—signals a paradigm shift where pure device companies are evolving into hybrid "device + biologic" powerhouses to cure conditions previously unaddressable by hardware alone.

HDIN Viewpoint

From an institutional perspective, HDIN Research assesses that the global ophthalmic sector is transitioning from an era of volume expansion to one of structural profitability and digital integration. Investors and corporate strategists must remain vigilant regarding the escalating goodwill risks on balance sheets driven by aggressive M&A, as well as the cash flow vulnerabilities of highly leveraged firms facing sustained macroeconomic tightening.

In this landscape, operational discipline is paramount. Alcon's unmatched capital allocation efficiency, rapid inventory turnover, and robust digital integration make it the sector's optimal risk-reward standard in the current valuation environment. Meanwhile, competitors must urgently resolve their structural inefficiencies or risk being permanently relegated to lower-margin tiers as global procurement policies tighten.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com