Ekso Bionics 2025: Navigating Financial Headwinds, Policy Moats, and the ChronoScale Pivot

Date : 2026-03-01

Reading : 106

Ekso Bionics is currently navigating a critical and turbulent inflection point, transitioning from a capital-intensive hardware manufacturer to an asset-light, policy-driven medical service provider. According to the latest analysis by HDIN Research, the company’s 2025 fiscal year results underscore a severe juxtaposition: while a landmark $91,000 Medicare reimbursement policy has established a robust strategic moat for its Personal Health division, sweeping cyclical headwinds and a 29% year-over-year revenue decline have forced the company into a defensive posture, culminating in a drastic strategic merger to ensure financial survival.

Here is our deep-dive analysis into the strategic implications behind the 2025 data.

Figure Ekso Bionics 2025: Fiscal Audit and the ChronoScale Strategic Pivot

Financial Health & Capital Allocation Efficiency

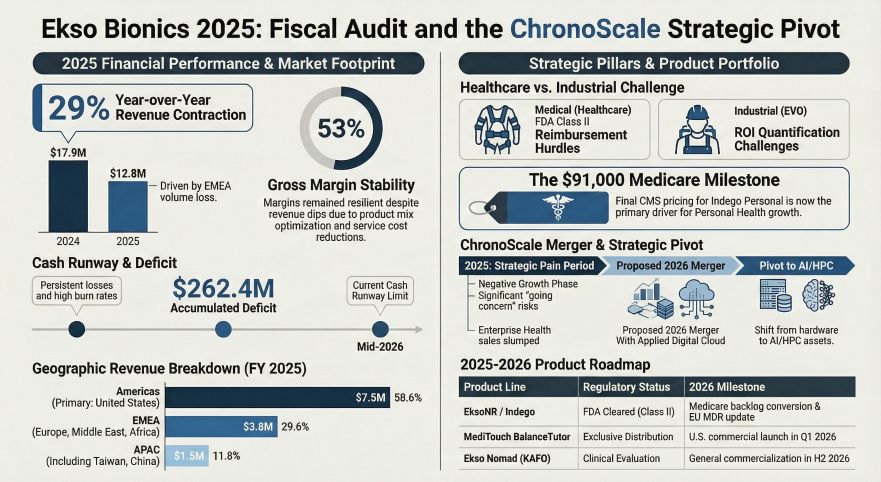

The 2025 financial disclosures reveal extreme vulnerability in Ekso Bionics' capital allocation efficiency. Total revenue contracted by 29% to $12.8 million, heavily dragged down by a 36% revenue shrinkage in the EMEA region and elongating 8-to-12-month capital expenditure approval cycles in the Enterprise Health sector.

While the company maintained a high gross margin of 53%, this stability was not the result of scale economics—which have severely deteriorated alongside volume drops—but rather a byproduct of optimizing product mix and shifting focus toward higher-margin individual medical devices.

More critically, the company's cash flow pipeline is heavily constrained. With a net loss of $11.7 million, an accumulated deficit of $262.4 million, and a year-end cash reserve of merely $1.2 million against a monthly burn rate of approximately $1 million, Ekso faces substantial "Going Concern" risks. The operational reality is stark: absent highly dilutive secondary financing or structural business combinations, the company's cash runway extends only to the end of the second quarter of 2026.

Strategic Pivots: RaaS Transition and the ChronoScale Merger

To mitigate these financial pressures, Ekso Bionics has initiated two major strategic pivots.

First, the company is attempting to break away from one-off capital sales by accelerating its Robot-as-a-Service (RaaS) and subscription models. However, HDIN Research notes that this remains a defensive mechanism rather than a primary growth engine. In 2025, traditional device sales still generated $9.24 million, dwarfing the $358,000 generated from subscriptions. The deferred revenue shrinkage from $3.88 million in 2024 to $3.14 million in 2025 indicates that the RaaS model has yet to achieve scale and generate the upfront cash inflows required to repair the balance sheet.

Second, and most transformative, is the proposed business combination with Applied Digital Cloud, announced in early 2026. This transaction will see the company rebrand as ChronoScale Corporation, signaling a radical shift from a pure MedTech robotics firm to a hybrid entity integrating High-Performance Computing (HPC) with medical technology. For Ekso, this is a calculated survival maneuver; the merger's core prerequisite is securing at least $15 million in post-closing liquidity, which will serve as the essential lifeline for its continued operations, albeit at the cost of diluting existing shareholder equity to approximately 3%.

Sector Positioning & Policy-Driven Moats

Despite balance sheet distress, Ekso Bionics has successfully entrenched a profound policy-driven moat. The U.S. Centers for Medicare & Medicaid Services (CMS) approval of an approximately $91,000 reimbursement rate for the Ekso Indego Personal device—targeting patients with Spinal Cord Injuries (SCI) from T3 to L5—is a watershed moment.

This policy tailwind has structurally differentiated Ekso from its peers. While the Enterprise segment faces intense competition from traditional physical therapy and rival robotic systems, the Personal Health market is seeing tangible momentum. The company has accumulated a backlog of over 50 qualified patients awaiting CMS claims processing. Furthermore, Ekso is aggressively targeting Total Addressable Market (TAM) expansion by seeking FDA indications for larger patient populations, including Stroke and Multiple Sclerosis (MS), while developing new form factors like the Ekso Nomad power knee-ankle-foot orthosis (KAFO).

HDIN Viewpoint

From an institutional perspective, HDIN Research views Ekso Bionics as a pioneer caught in the "valley of death" between technological validation and commercial scale. The company’s core valuation anchor is undergoing a fundamental paradigm shift. Historically valued on its proprietary exoskeleton clinical data and FDA clearances, the company’s future valuation will increasingly depend on the successful integration of its legacy assets with Applied Digital Cloud's HPC infrastructure under the ChronoScale umbrella.

For the broader exoskeleton sector, Ekso’s 2025 friction proves that relying solely on a high-barrier, long-cycle medical hardware model is financially unsustainable for independent public entities. Market participants and investors must closely monitor the Q2 2026 financing milestones; successful execution of the $15 million liquidity injection is the absolute prerequisite for realizing the delayed exponential growth promised by Medicare reimbursement rollouts.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Here is our deep-dive analysis into the strategic implications behind the 2025 data.

Figure Ekso Bionics 2025: Fiscal Audit and the ChronoScale Strategic Pivot

Financial Health & Capital Allocation Efficiency

The 2025 financial disclosures reveal extreme vulnerability in Ekso Bionics' capital allocation efficiency. Total revenue contracted by 29% to $12.8 million, heavily dragged down by a 36% revenue shrinkage in the EMEA region and elongating 8-to-12-month capital expenditure approval cycles in the Enterprise Health sector.

While the company maintained a high gross margin of 53%, this stability was not the result of scale economics—which have severely deteriorated alongside volume drops—but rather a byproduct of optimizing product mix and shifting focus toward higher-margin individual medical devices.

More critically, the company's cash flow pipeline is heavily constrained. With a net loss of $11.7 million, an accumulated deficit of $262.4 million, and a year-end cash reserve of merely $1.2 million against a monthly burn rate of approximately $1 million, Ekso faces substantial "Going Concern" risks. The operational reality is stark: absent highly dilutive secondary financing or structural business combinations, the company's cash runway extends only to the end of the second quarter of 2026.

Strategic Pivots: RaaS Transition and the ChronoScale Merger

To mitigate these financial pressures, Ekso Bionics has initiated two major strategic pivots.

First, the company is attempting to break away from one-off capital sales by accelerating its Robot-as-a-Service (RaaS) and subscription models. However, HDIN Research notes that this remains a defensive mechanism rather than a primary growth engine. In 2025, traditional device sales still generated $9.24 million, dwarfing the $358,000 generated from subscriptions. The deferred revenue shrinkage from $3.88 million in 2024 to $3.14 million in 2025 indicates that the RaaS model has yet to achieve scale and generate the upfront cash inflows required to repair the balance sheet.

Second, and most transformative, is the proposed business combination with Applied Digital Cloud, announced in early 2026. This transaction will see the company rebrand as ChronoScale Corporation, signaling a radical shift from a pure MedTech robotics firm to a hybrid entity integrating High-Performance Computing (HPC) with medical technology. For Ekso, this is a calculated survival maneuver; the merger's core prerequisite is securing at least $15 million in post-closing liquidity, which will serve as the essential lifeline for its continued operations, albeit at the cost of diluting existing shareholder equity to approximately 3%.

Sector Positioning & Policy-Driven Moats

Despite balance sheet distress, Ekso Bionics has successfully entrenched a profound policy-driven moat. The U.S. Centers for Medicare & Medicaid Services (CMS) approval of an approximately $91,000 reimbursement rate for the Ekso Indego Personal device—targeting patients with Spinal Cord Injuries (SCI) from T3 to L5—is a watershed moment.

This policy tailwind has structurally differentiated Ekso from its peers. While the Enterprise segment faces intense competition from traditional physical therapy and rival robotic systems, the Personal Health market is seeing tangible momentum. The company has accumulated a backlog of over 50 qualified patients awaiting CMS claims processing. Furthermore, Ekso is aggressively targeting Total Addressable Market (TAM) expansion by seeking FDA indications for larger patient populations, including Stroke and Multiple Sclerosis (MS), while developing new form factors like the Ekso Nomad power knee-ankle-foot orthosis (KAFO).

HDIN Viewpoint

From an institutional perspective, HDIN Research views Ekso Bionics as a pioneer caught in the "valley of death" between technological validation and commercial scale. The company’s core valuation anchor is undergoing a fundamental paradigm shift. Historically valued on its proprietary exoskeleton clinical data and FDA clearances, the company’s future valuation will increasingly depend on the successful integration of its legacy assets with Applied Digital Cloud's HPC infrastructure under the ChronoScale umbrella.

For the broader exoskeleton sector, Ekso’s 2025 friction proves that relying solely on a high-barrier, long-cycle medical hardware model is financially unsustainable for independent public entities. Market participants and investors must closely monitor the Q2 2026 financing milestones; successful execution of the $15 million liquidity injection is the absolute prerequisite for realizing the delayed exponential growth promised by Medicare reimbursement rollouts.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research Profile:

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com