Straumann vs. Envista: Decoding the 2025 Strategic Moats and Ecosystem Wars in the Dental Industry

Date : 2026-03-01

Reading : 106

As the global dental industry navigates an era of macroeconomic volatility and structural transformation, the divergence between top-tier players has never been more pronounced. An in-depth 2025 financial and strategic analysis by HDIN Research reveals a stark contrast: while Straumann (STMN) leverages a zero-leverage balance sheet and an aggressive AI-driven software ecosystem to compound its premium market share, Envista (NVST) continues to carry the weight of historical M&A premiums, relying on operational cost-cutting to defend its margins. Ultimately, the battle has shifted from selling standalone implants to monopolizing the digital workflow of Dental Service Organizations (DSOs).

Figure 2025 DENTAL GIANTS DUEL: ENVISTA VS STRAUMANN

Sector Positioning: The Shift to AI-Driven Digital Ecosystems

Sector Positioning: The Shift to AI-Driven Digital Ecosystems

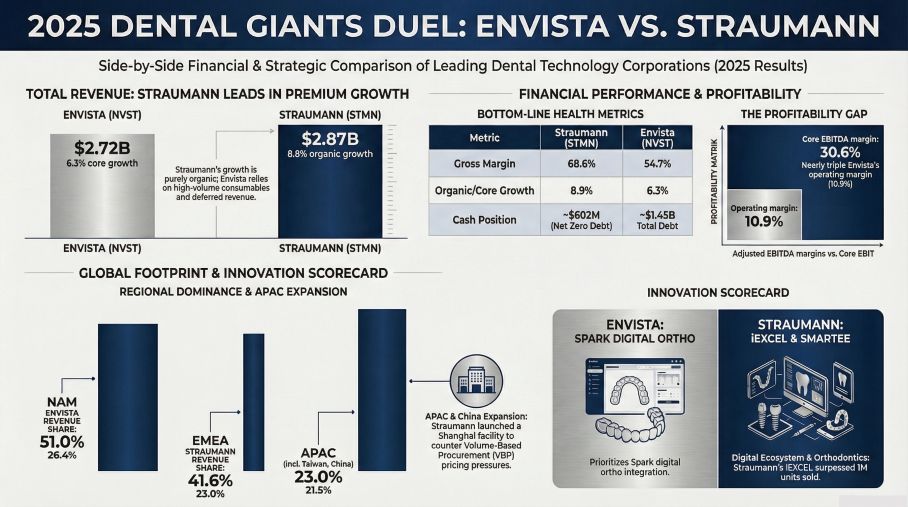

The fundamental paradigm of the dental sector has pivoted from physical product superiority to comprehensive digital workflow integration. Both companies recognize that Intraoral Scanners (IOS) are no longer just hardware, but the critical "traffic entry tickets" into the clinic’s ecosystem.

However, their Sector Positioning diverges in execution. Straumann is aggressively transitioning into an ecosystem builder. By integrating the SIRIOS X3 scanner with its open-architecture AXS cloud platform and acquiring AI-specialist Promaton, Straumann has successfully created a digital twin workflow that reduces clinical planning time by over 60%. This end-to-end connectivity—from AI-assisted diagnostics to localized 3D printing (MIDAS)—creates a high switching cost for DSOs.

Conversely, Envista employs a closed-loop synergy between its imaging equipment (like the DEXIS Imprevo) and consumables. While highly effective at utilizing diagnostic hardware as a gateway to drive its DTX Studio software and consumable sales, Envista’s hardware-heavy portfolio makes it inherently more vulnerable to the capital expenditure (CAPEX) cycles of dental practices.

Financial Health & Capital Allocation Efficiency

Beneath the surface of top-line revenue growth, the disparity in Capital Allocation Efficiency between the two giants is striking.

Straumann demonstrates near-impenetrable financial resilience. Operating essentially debt-free with a staggering interest coverage ratio of approximately 41.5x, the company is entirely insulated from the current high-interest-rate environment. This robust capitalization enables Straumann to sustain an elite gross margin of 68.6% and aggressively fund its R&D initiatives (5.2% of revenue) without compromising liquidity.

Envista, meanwhile, is navigating a high-leverage reality. With roughly $1.45 billion in total debt and an interest coverage ratio of just 5.8x, the company’s balance sheet is heavily weighted. Notably, following a massive $1.15 billion impairment in 2024, goodwill still accounts for 41.5% of Envista’s total assets in 2025. While Envista reported an 8.3% nominal revenue growth, a deep dive reveals that 5.2% of this was driven by volume recovery and deferred revenue recognition, with pricing power contributing a mere 1.1%. This reliance on accounting-driven revenue highlights a structural vulnerability compared to Straumann's robust 8.9% pure organic growth.

Navigating Cyclical Headwinds and the VBP Era

Both companies face profound Cyclical Headwinds, including inflation-suppressed consumer discretionary spending and the aggressive pricing pressures of Volume-Based Procurement (VBP) policies, particularly in China.

To defend its profitability against VBP, Straumann executed a highly effective localized defense strategy. The full operation of its Shanghai manufacturing campus in 2025 localized the supply chain, stripping out tariff and logistics costs. Coupled with a multi-brand strategy (leveraging "value brands" like Medentika and Neodent), Straumann successfully captured volume in the mass market without diluting its premium flagship offerings.

Envista has countered these margin pressures by leaning heavily into the Envista Business System (EBS). By aggressively streamlining operational costs and consolidating manufacturing bases, Envista has managed to stabilize its profitability. However, its overall gross margin of 54.7% indicates that it remains significantly more exposed to supply chain friction and tariff impacts than its Swiss rival.

HDIN Viewpoint

At HDIN Research, we believe the future of the global dental industry no longer lies in merely manufacturing clinical tools, but in delivering clinical "certainty." Strategic Moats are now built on data interoperability, AI-driven automation, and deep integration with DSO procurement channels.

Straumann’s aggressive M&A in software capabilities, combined with its fortress-like balance sheet, grants it the agility to dictate industry standards. Envista, while demonstrating commendable operational discipline through its EBS framework, remains in a defensive posture—tasked with unwinding historical debt and optimizing a mature, consumable-heavy portfolio. For stakeholders and investors, scrutinizing the true quality of organic growth versus deferred revenue recognition will be paramount in identifying long-term value creators in this space.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

Figure 2025 DENTAL GIANTS DUEL: ENVISTA VS STRAUMANN

Sector Positioning: The Shift to AI-Driven Digital EcosystemsThe fundamental paradigm of the dental sector has pivoted from physical product superiority to comprehensive digital workflow integration. Both companies recognize that Intraoral Scanners (IOS) are no longer just hardware, but the critical "traffic entry tickets" into the clinic’s ecosystem.

However, their Sector Positioning diverges in execution. Straumann is aggressively transitioning into an ecosystem builder. By integrating the SIRIOS X3 scanner with its open-architecture AXS cloud platform and acquiring AI-specialist Promaton, Straumann has successfully created a digital twin workflow that reduces clinical planning time by over 60%. This end-to-end connectivity—from AI-assisted diagnostics to localized 3D printing (MIDAS)—creates a high switching cost for DSOs.

Conversely, Envista employs a closed-loop synergy between its imaging equipment (like the DEXIS Imprevo) and consumables. While highly effective at utilizing diagnostic hardware as a gateway to drive its DTX Studio software and consumable sales, Envista’s hardware-heavy portfolio makes it inherently more vulnerable to the capital expenditure (CAPEX) cycles of dental practices.

Financial Health & Capital Allocation Efficiency

Beneath the surface of top-line revenue growth, the disparity in Capital Allocation Efficiency between the two giants is striking.

Straumann demonstrates near-impenetrable financial resilience. Operating essentially debt-free with a staggering interest coverage ratio of approximately 41.5x, the company is entirely insulated from the current high-interest-rate environment. This robust capitalization enables Straumann to sustain an elite gross margin of 68.6% and aggressively fund its R&D initiatives (5.2% of revenue) without compromising liquidity.

Envista, meanwhile, is navigating a high-leverage reality. With roughly $1.45 billion in total debt and an interest coverage ratio of just 5.8x, the company’s balance sheet is heavily weighted. Notably, following a massive $1.15 billion impairment in 2024, goodwill still accounts for 41.5% of Envista’s total assets in 2025. While Envista reported an 8.3% nominal revenue growth, a deep dive reveals that 5.2% of this was driven by volume recovery and deferred revenue recognition, with pricing power contributing a mere 1.1%. This reliance on accounting-driven revenue highlights a structural vulnerability compared to Straumann's robust 8.9% pure organic growth.

Navigating Cyclical Headwinds and the VBP Era

Both companies face profound Cyclical Headwinds, including inflation-suppressed consumer discretionary spending and the aggressive pricing pressures of Volume-Based Procurement (VBP) policies, particularly in China.

To defend its profitability against VBP, Straumann executed a highly effective localized defense strategy. The full operation of its Shanghai manufacturing campus in 2025 localized the supply chain, stripping out tariff and logistics costs. Coupled with a multi-brand strategy (leveraging "value brands" like Medentika and Neodent), Straumann successfully captured volume in the mass market without diluting its premium flagship offerings.

Envista has countered these margin pressures by leaning heavily into the Envista Business System (EBS). By aggressively streamlining operational costs and consolidating manufacturing bases, Envista has managed to stabilize its profitability. However, its overall gross margin of 54.7% indicates that it remains significantly more exposed to supply chain friction and tariff impacts than its Swiss rival.

HDIN Viewpoint

At HDIN Research, we believe the future of the global dental industry no longer lies in merely manufacturing clinical tools, but in delivering clinical "certainty." Strategic Moats are now built on data interoperability, AI-driven automation, and deep integration with DSO procurement channels.

Straumann’s aggressive M&A in software capabilities, combined with its fortress-like balance sheet, grants it the agility to dictate industry standards. Envista, while demonstrating commendable operational discipline through its EBS framework, remains in a defensive posture—tasked with unwinding historical debt and optimizing a mature, consumable-heavy portfolio. For stakeholders and investors, scrutinizing the true quality of organic growth versus deferred revenue recognition will be paramount in identifying long-term value creators in this space.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com