Note Inc.: Transforming from a C2C Media Platform to an AI-Driven Content Hub

Date : 2026-03-01

Reading : 135

Note Inc. has officially crossed a critical profitability threshold in FY2025, recording a 25.0% year-over-year revenue surge to $27.69 million, alongside a 384.7% explosive growth in operating profit ($1.71 million). However, this inflection point was not merely a byproduct of organic user acquisition. Driven by internal operational leverage and sophisticated capital allocation, Note Inc. is structurally pivoting from a traditional content hosting platform into an "AI-driven content circulation hub."

HDIN Research has conducted a deep-dive analysis of Note Inc.’s FY2025 financial disclosures, unpacking the strategic implications behind its evolving business matrix, accounting practices, and sector positioning.

Figure Note lnc. 2025: The Al-Driven inflection Point

Strategic Moats and Ecosystem Evolution

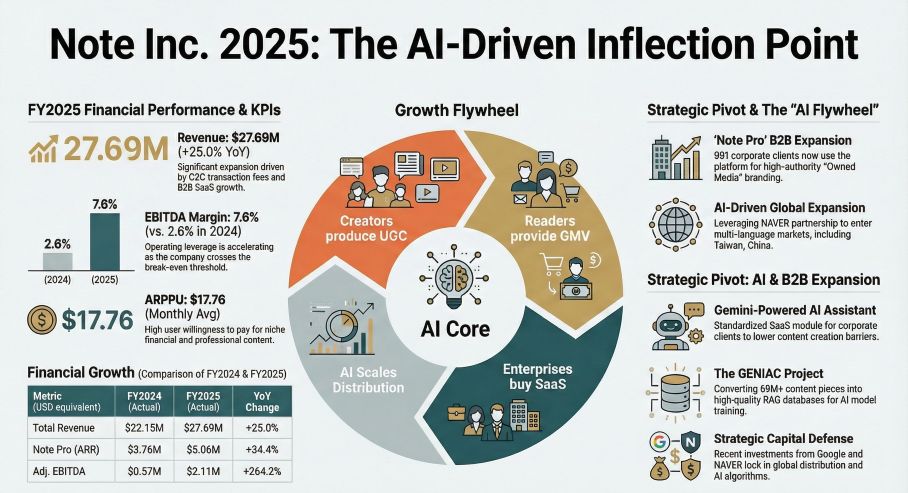

Note Inc. has successfully cultivated a highly defensible strategic moat by adhering to a "no ads, no ranking" philosophy. By avoiding algorithm-driven pageview races, the platform has insulated itself from content homogenization and low-quality viral bait, establishing a premium ecosystem. This distinct community positioning directly translates into high user willingness to pay, sustaining a robust Average Revenue Per Paying User (ARPPU) of $17.76.

The company’s revenue architecture has evolved into a resilient multi-dimensional matrix:

* C2C Transaction Commissions: Serving as the core engine, platform GMV expanded by 24.9% to $142.5 million in FY2025, proving Note Inc.'s dominance in the direct-to-consumer content monetization space.

* B2B SaaS Penetration: The "note pro" service, facilitating corporate digital transformation (DX) and owned media, witnessed a 34.4% year-over-year growth in Annual Recurring Revenue (ARR), reaching $5.06 million across 991 enterprise clients. This SaaS subscription model provides a highly predictable cash flow, mitigating the cyclical headwinds associated with retail transaction volatility.

Financial Health & Capital Allocation Efficiency

While Note Inc. reported a staggering 93.6% gross margin, HDIN Research's audit perspective reveals a more nuanced reality of its capital allocation efficiency. The company categorizes substantial variable costs—specifically $6.64 million in payment processing fees and $4.13 million in cloud computing expenses—under SG&A rather than COGS. Adjusting for these structural expenses, the authentic platform contribution margin rests at approximately 54.7%, indicating that escalating AI computing costs may pressure actual margins in the future.

Furthermore, the reported FY2025 net profit of $2.95 million was significantly inflated by a non-recurring accounting optimization—a $1.21 million deferred income tax asset adjustment. Nevertheless, Note Inc. exhibits exceptional working capital management. By holding $13.95 million in unwithdrawn creator funds, the platform leverages a massive, interest-free capital pool, fundamentally functioning as a "creator financial leverage platform" to fund its light-asset expansion without debt burdens.

AI-Driven Operational Leverage & Strategic Alliances

Internally, the deployment of advanced AI coding and editing tools (such as Cursor and Claude MAX) has generated massive operational leverage. Note Inc. increased its revenue per employee by approximately 62% compared to FY2023, reaching $178,000.

Externally, Note Inc. is aggressively utilizing capital alliances to secure top-tier technology and global distribution channels. In 2025, the company secured strategic investments from Google ($3.34 million) and NAVER ($13.37 million). These alliances are not just capital injections; they are defensive maneuvers. Integrating Google’s Gemini technology enhances the platform's AI content generation capabilities, while NAVER's global IP distribution network provides the necessary infrastructure for Note Inc.’s FY2026 international expansion—targeting Greater China (including Taiwan, China and Hong Kong SAR) and Southeast Asia through AI-powered translation frameworks.

Additionally, Note Inc.’s participation in the Japanese government-backed "GENIAC" project positions it to monetize its repository of over 69 million high-quality articles as premium RAG (Retrieval-Augmented Generation) databases for AI developers, unlocking a highly scalable, low-marginal-cost IP revenue stream.

Sector Positioning & Cyclical Headwinds

Despite the strong growth narrative supporting management's aggressive target of $66.86 million in revenue by FY2030, systemic risks remain. At a P/E ratio of 61.9x, the market has heavily priced in the success of Note Inc.'s AI transition.

The platform faces critical headwinds: an over-reliance on high-monetization niches (such as investing and horse racing) makes it vulnerable to regulatory shifts. Moreover, as generative AI proliferates, the influx of automated, low-quality content threatens to erode the very trust and authenticity that form Note Inc.'s primary competitive moat.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Note Inc. as a prime example of a digital platform successfully crossing the chasm from user-growth cash burn to scale-driven profitability. Its strategic foresight in transitioning into an "AI training data supplier" while maintaining SaaS growth is commendable. However, the true test of its lofty 2030 valuation will rely on two factors: the commercial viability of its AI data-sharing profit models (GENIAC) and its ability to strictly control Customer Acquisition Costs (CAC) as it navigates cross-cultural barriers during its impending multi-language global rollout.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com

HDIN Research has conducted a deep-dive analysis of Note Inc.’s FY2025 financial disclosures, unpacking the strategic implications behind its evolving business matrix, accounting practices, and sector positioning.

Figure Note lnc. 2025: The Al-Driven inflection Point

Strategic Moats and Ecosystem Evolution

Note Inc. has successfully cultivated a highly defensible strategic moat by adhering to a "no ads, no ranking" philosophy. By avoiding algorithm-driven pageview races, the platform has insulated itself from content homogenization and low-quality viral bait, establishing a premium ecosystem. This distinct community positioning directly translates into high user willingness to pay, sustaining a robust Average Revenue Per Paying User (ARPPU) of $17.76.

The company’s revenue architecture has evolved into a resilient multi-dimensional matrix:

* C2C Transaction Commissions: Serving as the core engine, platform GMV expanded by 24.9% to $142.5 million in FY2025, proving Note Inc.'s dominance in the direct-to-consumer content monetization space.

* B2B SaaS Penetration: The "note pro" service, facilitating corporate digital transformation (DX) and owned media, witnessed a 34.4% year-over-year growth in Annual Recurring Revenue (ARR), reaching $5.06 million across 991 enterprise clients. This SaaS subscription model provides a highly predictable cash flow, mitigating the cyclical headwinds associated with retail transaction volatility.

Financial Health & Capital Allocation Efficiency

While Note Inc. reported a staggering 93.6% gross margin, HDIN Research's audit perspective reveals a more nuanced reality of its capital allocation efficiency. The company categorizes substantial variable costs—specifically $6.64 million in payment processing fees and $4.13 million in cloud computing expenses—under SG&A rather than COGS. Adjusting for these structural expenses, the authentic platform contribution margin rests at approximately 54.7%, indicating that escalating AI computing costs may pressure actual margins in the future.

Furthermore, the reported FY2025 net profit of $2.95 million was significantly inflated by a non-recurring accounting optimization—a $1.21 million deferred income tax asset adjustment. Nevertheless, Note Inc. exhibits exceptional working capital management. By holding $13.95 million in unwithdrawn creator funds, the platform leverages a massive, interest-free capital pool, fundamentally functioning as a "creator financial leverage platform" to fund its light-asset expansion without debt burdens.

AI-Driven Operational Leverage & Strategic Alliances

Internally, the deployment of advanced AI coding and editing tools (such as Cursor and Claude MAX) has generated massive operational leverage. Note Inc. increased its revenue per employee by approximately 62% compared to FY2023, reaching $178,000.

Externally, Note Inc. is aggressively utilizing capital alliances to secure top-tier technology and global distribution channels. In 2025, the company secured strategic investments from Google ($3.34 million) and NAVER ($13.37 million). These alliances are not just capital injections; they are defensive maneuvers. Integrating Google’s Gemini technology enhances the platform's AI content generation capabilities, while NAVER's global IP distribution network provides the necessary infrastructure for Note Inc.’s FY2026 international expansion—targeting Greater China (including Taiwan, China and Hong Kong SAR) and Southeast Asia through AI-powered translation frameworks.

Additionally, Note Inc.’s participation in the Japanese government-backed "GENIAC" project positions it to monetize its repository of over 69 million high-quality articles as premium RAG (Retrieval-Augmented Generation) databases for AI developers, unlocking a highly scalable, low-marginal-cost IP revenue stream.

Sector Positioning & Cyclical Headwinds

Despite the strong growth narrative supporting management's aggressive target of $66.86 million in revenue by FY2030, systemic risks remain. At a P/E ratio of 61.9x, the market has heavily priced in the success of Note Inc.'s AI transition.

The platform faces critical headwinds: an over-reliance on high-monetization niches (such as investing and horse racing) makes it vulnerable to regulatory shifts. Moreover, as generative AI proliferates, the influx of automated, low-quality content threatens to erode the very trust and authenticity that form Note Inc.'s primary competitive moat.

HDIN Viewpoint

From an institutional perspective, HDIN Research views Note Inc. as a prime example of a digital platform successfully crossing the chasm from user-growth cash burn to scale-driven profitability. Its strategic foresight in transitioning into an "AI training data supplier" while maintaining SaaS growth is commendable. However, the true test of its lofty 2030 valuation will rely on two factors: the commercial viability of its AI data-sharing profit models (GENIAC) and its ability to strictly control Customer Acquisition Costs (CAC) as it navigates cross-cultural barriers during its impending multi-language global rollout.

Presentation Download

Click the PDF download link under “Related Topics” to access the presentation of this report.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

E-mail: sales@hdinresearch.com